Table of contents

- Company profile - Manufacturer of lifestyle and performance footwear

- The latest Deckers Outdoor quarterly figures from June 2024

- Deckers Outdoor stock forecast 2024

- Important key figures of the Deckers Outdoor stock from the HGI analysis

- Valuation of the Deckers Outdoor stock

- Conclusion on the Deckers Outdoor stock

Deckers Outdoor stocks (ISIN: US2435371073) are a niche specialist in the lifestyle and performance footwear sector, characterized by a highly diversified brand portfolio. The company benefits from megatrends such as the increasing demand for health-conscious lifestyles, outdoor activities and sustainable products. Above all, however, the Americans have not missed the trend towards cushioned soles. But they are also stepping on the gas in the e-commerce sector. Expansion abroad is progressing. There is much to suggest that things are going really well here.

Investors have long understood Deckers Outdoor's equity story and are rewarding the high growth with juicy stock price increases. Until recently, the stock price had increased almost tenfold over ten years.

Source: Deckers Outdoor stock price

Despite strong price increases, Deckers Outdoor stocks do not necessarily have to be expensive. Indeed, taking into account continued double-digit EPS growth, the current price/earnings ratio of 27 could even be fair or favorable.

The numerous megatrends (outdoor, health, cushioning shoes, luxury, e-commerce) from which the company is benefiting indicate a high probability that Deckers Outdoor will also be able to achieve double-digit growth in the long term.

However, growth appears to be leveling off significantly after a strong start to the 2025 financial year. The following Deckers Outdoor stock analysis reveals how this development should be assessed and whether the stock could ultimately be a buy.

The most important facts in brief

- Deckers Outdoor is a niche specialist in the lifestyle and performance footwear sector

- Growth is high, megatrends play into the company's hands

- Double-digit annual EPS growth should also be possible in the long term

- The stock could be fairly valued with an expected P/E ratio of 26

Company profile - manufacturer of lifestyle and performance footwear

Deckers Outdoor Corporation is a global company specializing in the development, design, marketing and distribution of innovative and high-quality footwear and apparel products. The business model is based on various distribution channels, including wholesale, direct-to-consumer business and international distribution partnerships.

Source: Annual Report 2024 Deckers Outdoor

At segment level, sales in wholesale (sales via third parties) and direct-to-consumer are allocated to the individual brands. Let's take a closer look at what happens here.

Direct-to-consumer and wholesale

In the Direct-To-Consumer (DTC) segment, Deckers Outdoor sells its products directly to end customers via its own retail stores and e-commerce platforms. On the one hand, this enables the company to achieve higher margins by cutting out middlemen. On the other hand, direct customer contact enables better control over brand presentation and the shopping experience. Not forgetting the data obtained. This can be meaningfully evaluated and used for customer loyalty.

In the wholesale segment, Deckers Outdoor sells its products via third parties, including large retail chains, specialist stores and international sales partners. This channel makes it possible to quickly reach a broad customer base and increase brand awareness through presence in various retail environments.

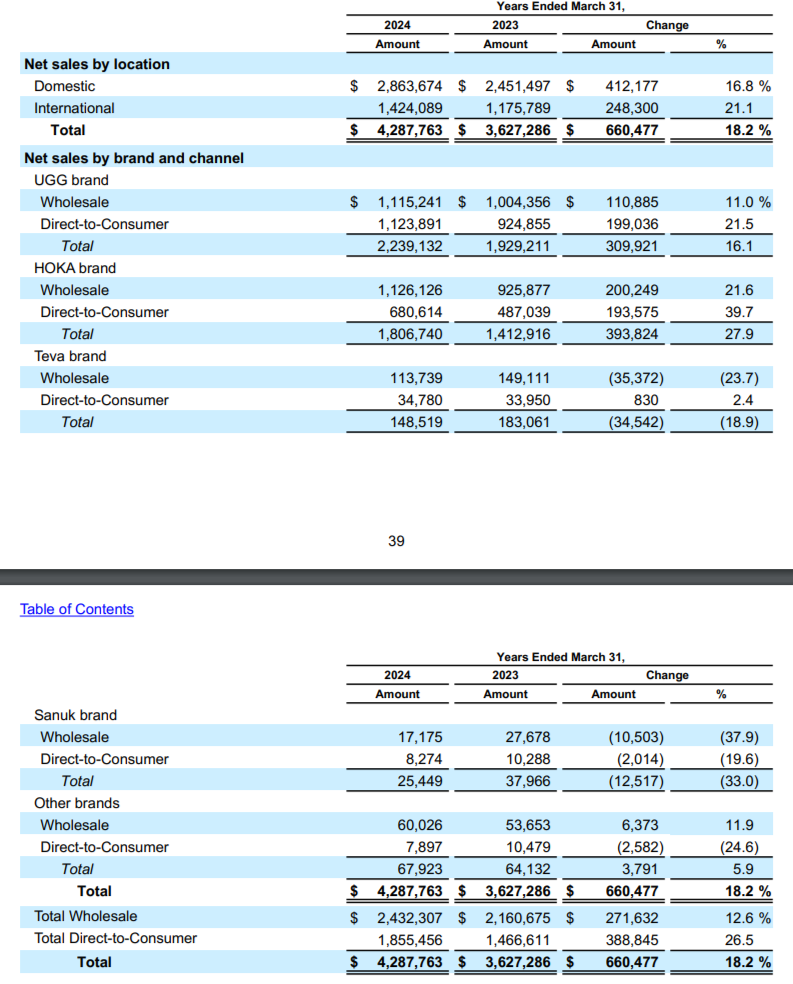

Both wholesale and direct-to-consumer have disadvantages. Looking at the distribution of the two sales areas, it is clear that the wholesale business still dominates at present. In the last financial year 2024, which ended on March 31, around 57% of sales were generated in wholesale. However, the direct-to-consumer business is growing more than twice as fast at 26.5%. It is therefore probably only a matter of time before the company defines its brand image more strongly through its own sales activities and analyzes customer data.

UGG

UGG is one of Deckers Outdoor's best-known brands. It offers luxurious and comfortable shoes, clothing and accessories. Originally known as a brand for sheepskin boots, UGG has developed into a lifestyle brand that offers a wide range of products. UGG's target group consists of fashion-conscious consumers who are looking for comfort and style. Sales are split equally between the wholesale and direct-to-consumer segments, with the direct-to-consumer segment growing significantly faster (21.5%) than the wholesale segment (11%). Overall, the brand accounts for annual sales of EUR 2.2 billion, which corresponds to a stock of Group sales of over 52%. The brand was purchased in 1995.

HOKA

The second major brand in the Group is HOKA. It is known for its performance running shoes and clothing, which stand out for their innovative midsole technology and exceptional comfort. Logically, HOKA's target group includes runners, athletes and outdoor enthusiasts who value performance and comfort. The interesting thing is that more and more professional athletes are switching to equipment from the Deckers brand, which stands for a strong sales performance. However, the focus here is still on niche areas of sport. However, these are growing better than the mainstream.

The HOKA brand recently accounted for 42% of total sales, making it the second-largest individual brand in the Group in terms of sales. However, with sales growth of almost 28% in the past financial year, it is the fastest growing brand. Sales continue to be made primarily via retailers, although the direct sales business is also growing much faster here. Again, this is not an in-house creation. The brand was purchased in 2013 for around one million US dollars - a real bargain.

Teva and Sanuk

The Teva brand focuses on outdoor sandals and shoes for adventure and leisure activities. Teva appeals to an active, outdoor-oriented target group that values functionality and durability. Through innovative designs and collaborations with other brands and designers, Deckers is trying to strengthen Teva's position in the outdoor and leisure market. Nevertheless, the brand is struggling with structural problems, which are reflected in the sales figures. In the 2024 financial year, for example, sales fell by 18.9 percent to 149 million US dollars.

Sanuk is a similar example. The brand is known for its relaxed and comfortable footwear, often made from innovative materials. The brand targets consumers who prefer a casual and unconventional style. However, not all potential customers appreciate this. The brand lost a third of its turnover in the 2024 financial year. At 25.5 million US dollars, it is already the weakest individual brand in the Group in terms of sales.

Other Brands

The Other Brands segment comprises smaller brands in Deckers' portfolio that serve specific market segments. They complement the existing product range and contribute to the company's diversification. This segment also suffered a significant drop in sales in the direct-to-consumer area in the past financial year. Overall, however, a slight increase in turnover of 5.9% to 68 million was achieved. Similar to Alphabet with its Other Bets, these are also likely to be so-called test brands. If they prove successful, they could be rolled out and later stand for brands with sales in the billions.

International expansion

A final word on international expansion is of course essential. Here it is clear that Deckers Outdoor is already well advanced in the internationalization of its products, with foreign sales of 1.4 billion euros. They account for around a third of total sales. Foreign business is currently the growth driver. Although domestic business in the USA is also growing at a visible double-digit rate of 16.8 percent, the dynamics abroad are in a different class with sales growth of 21.1 percent.

The latest Deckers Outdoor quarterly figures from June 2024

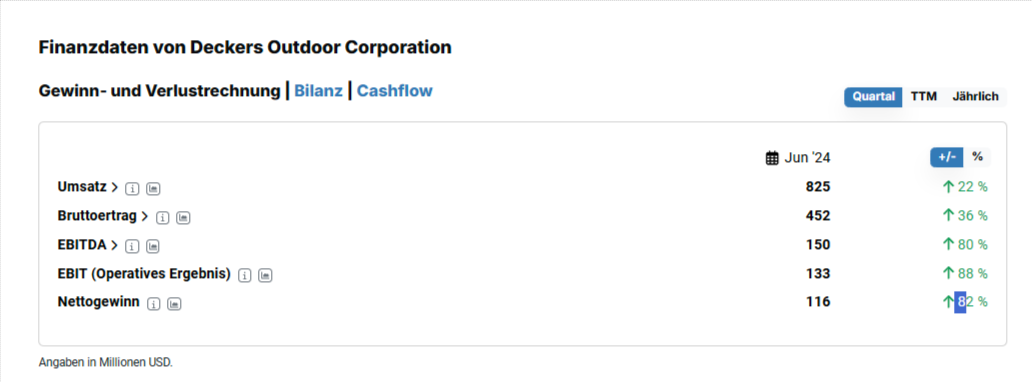

Deckers Outdoors' latest quarterly figures were convincing across the board, at least if you look at what Nike delivered.

Source: Financial data for Q1/2025 from Deckers Outdoor

In the first quarter of 2025, revenue growth of 22% to USD 825 million was reported for the quarter ending June 30, 2024. Compared to growth of 18.2% in the 2024 financial year, this represents increasing momentum. There were also big leaps in net income. The quarterly result of 116 million US dollars is 82% higher than the comparable figure for the previous year.

Both UGG and HOKA continued their strong growth of 14% and 29.7% respectively. What is striking here is that UGG's growth has slowed further, while that of the HOKA brand has gained some momentum. It is also very positive that the two smaller brands Teva and Sanuk, which failed to impress in the last financial year with a severe slump in sales, achieved a turnaround in the first quarter of 2025. With sales growth of 4.3% and 28.4% respectively for Sanuk, the brands were able to show positive growth again.

Koolaburra , a promising candidate in the other brands segment, also performed extremely well. Net sales here rose by 124 percent to 4 million US dollars. The brand stands for more affordable and fashionable sheepskin and lifestyle products. It is intended to be an affordable alternative to the UGG brand.

Deckers Outdoor stock forecast 2024

Deckers Outdoor's forecasts for the 2025 financial year envisage further growth. For the 2025 financial year, the company expects net sales to increase by around 10% to USD 4.7 billion with a gross margin of around 54%. Compared to the previous figures, however, this represents a significant slowdown in growth momentum. The operating margin is expected to be between 19.5 and 20 percent, with diluted earnings per stock between 29.75 and 30.65 US dollars.

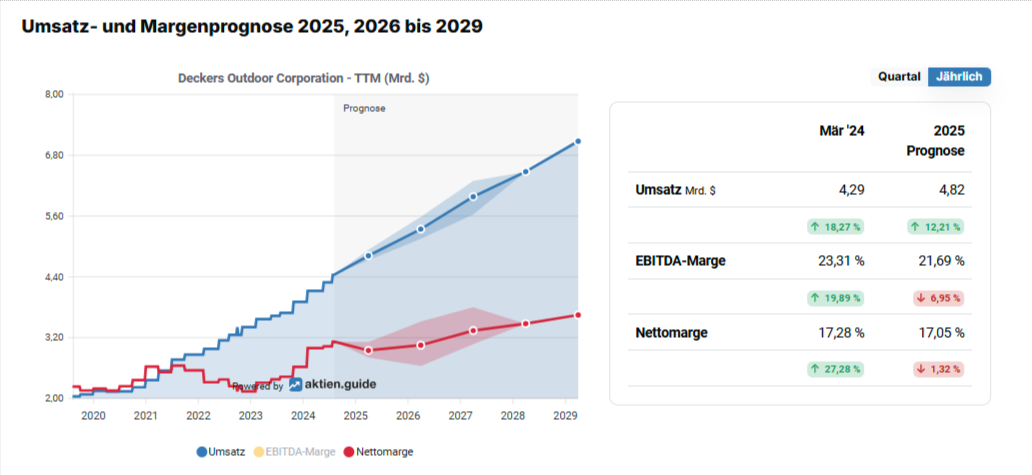

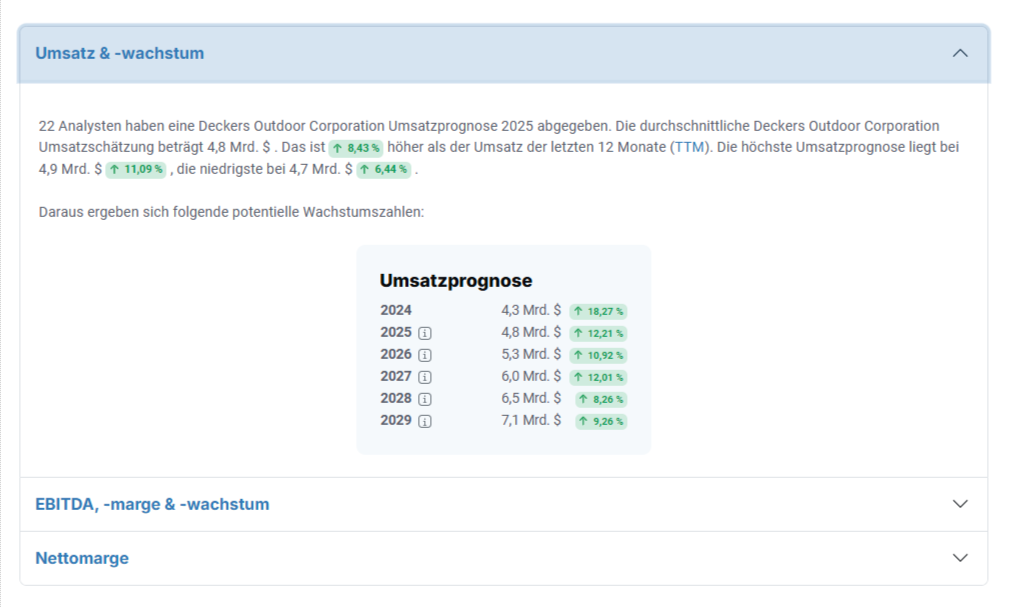

Let's take a look at the analysts' forecasts for 2025. They expect slightly higher sales of USD 4.8 billion, which corresponds to growth of 12.2% compared to the previous year.

Source: Analysts' sales and margin forecast for Deckers Outdoor stocks

Growth is also expected to remain intact in the long term. Turnover of USD 7.1 billion is expected for 2029, which corresponds to an increase of almost 50% compared to the forecast turnover for 2025. Double-digit growth is no longer likely after that, but high single-digit growth still seems very solid.

Source: Deckers Outdoor, analysts' sales growth forecast 2029

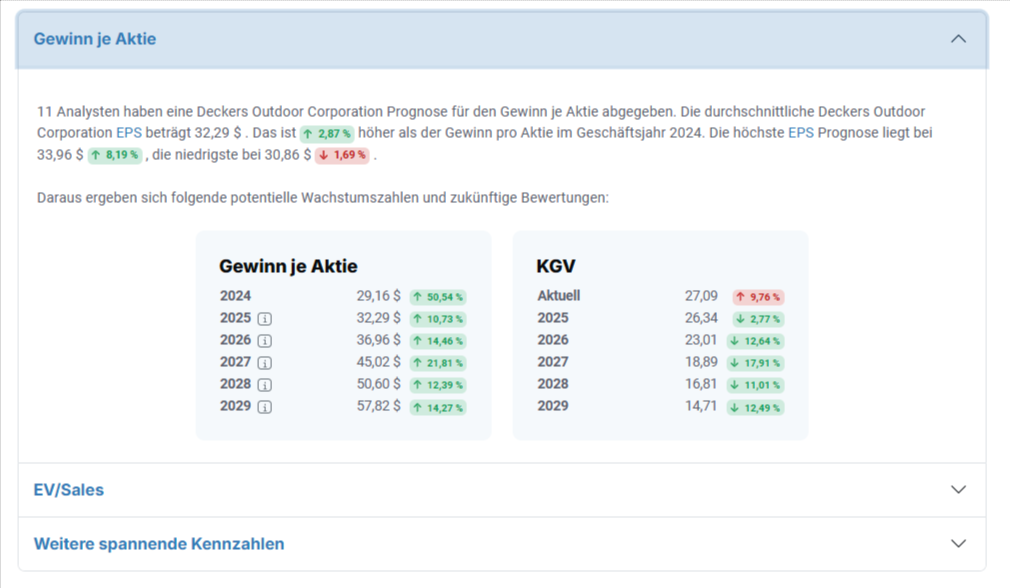

EPS is expected to develop much more dynamically. However, at USD 32.29, only a slight increase of 10.7% compared to sales growth is forecast for 2025 for the time being. In the long term, however, this is likely to change according to the analysts. Constant double-digit growth is the order of the day here. EPS of USD 57.82 could be achieved in 2029. Compared to the expected profit for 2025, this would correspond to an increase of 91%.

Source: Deckers Outdoor, analysts' profit forecast 2029

If the analysts' forecasts come true, the current ambitious P/E ratio of 27.1 could fall to a very solid 14.7 by the end of the decade. With continued double-digit EPS growth rates and a positive outlook for the future, the stock would then no longer be considered expensive by any means.

Important key figures of the Deckers Outdoor stock from the HGI analysis

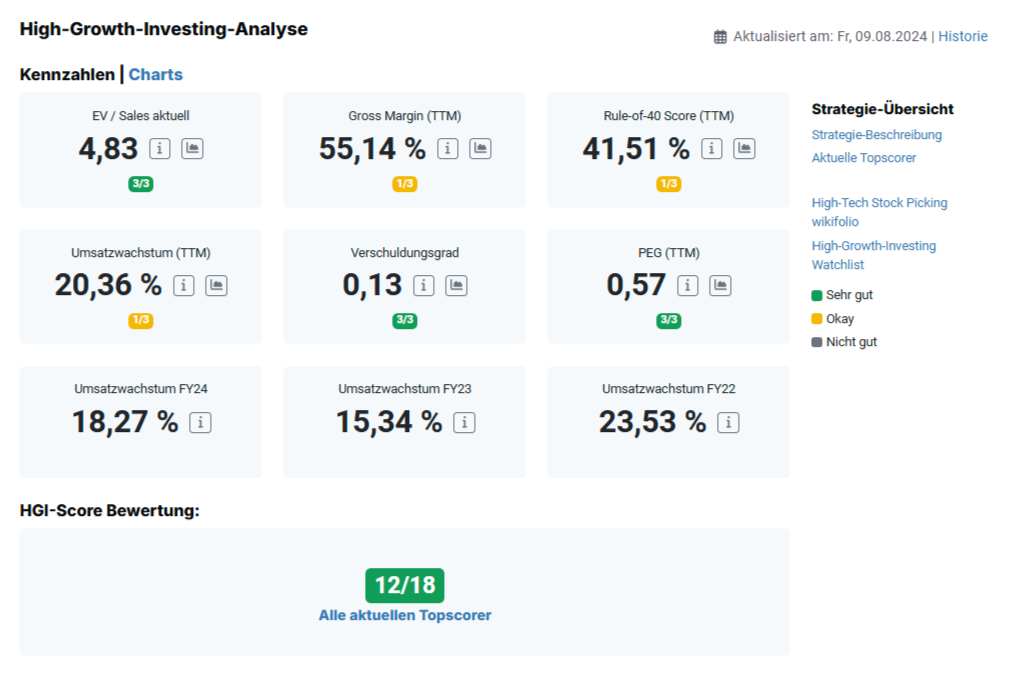

Deckers Outdoor is without doubt a growth company. This is confirmed by the high growth rates of recent years alone. The two main brands, UGG and HOKA, are the driving forces here, although the former has recently suffered somewhat from a slowdown in growth. On the other hand, HOKA has been all the more convincing, as has the cheaper alternative brand to UGG, Koolaburra.

Source: HGI Score, aktien.guide

Deckers Outdoor stocks also occupy a top position in the High Growth investment strategy. With a score of twelve points, it easily achieves top scorer status. The stock scored particularly well with a low gearing ratio (0.13), an attractive sales multiple (EV/Sales: 4.8) and a favorable PEG ratio of 0.57. One point was achieved in each of the other three categories.

Looking ahead, however, sales growth is likely to slow down further. The most recently achieved point for sales growth over the last twelve months (TTM) is then likely to be lost. If EBIT growth then also slows visibly while the valuation remains high, the PEG ratio is also likely to lose points. The same applies to the Rule-of-40 point, which was only just won.

Overall, however, Deckers Outdoor is likely to be a quality stock, although the dynamics of the fashion business should not be underestimated. As we know from the past, fashion trends can change quickly. What was trendy yesterday and in recent years may be out of fashion again in the next few years. Even an icon of the sector such as VFC Corp. has had to learn this painfully.

Valuation of Deckers Outdoor stocks

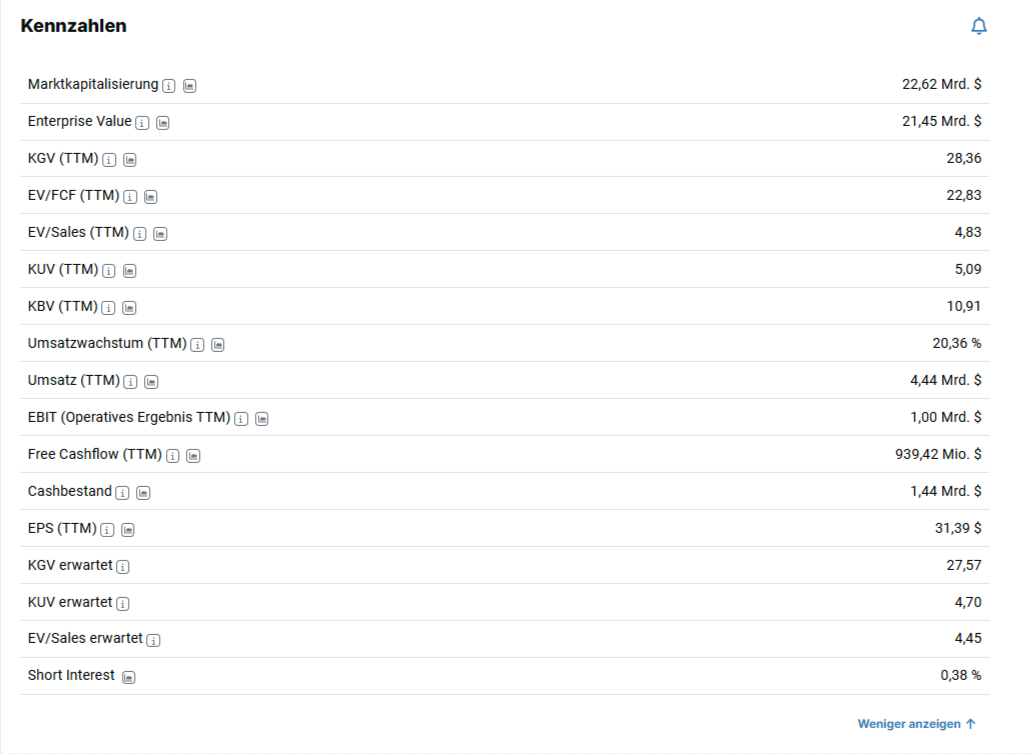

With an expected P/E ratio of 27.6, the valuation of Deckers Outdoor stocks can be classified as high. However, sales growth of 20.4 percent was also delivered in the last twelve months, which is also very high.

Source: Valuations of the Deckers Outdoor stock

However, it could be problematic that the management is only forecasting growth of 10 percent for the year as a whole. The absolute level of growth is probably less important than the direction of growth. And measured against the strong figures for the first quarter, this is a drastic slowdown in growth, the cause of which is not entirely clear. Is it due to the companies and increasing competition or is it more a general economic weakness? Analysts tend to assume the latter. They remain optimistic about Deckers Outdoor stocks and expect double-digit EPS growth rates across the board until 2029. The P/E ratio should then fall relatively quickly to a value visibly below 15. In such a scenario, Deckers stocks would of course not be expensive at all.

Conclusion on Deckers Outdoor stocks

To summarize, Deckers Outdoor is well positioned to benefit from the current megatrends in the lifestyle and performance footwear market. The company has established itself as a niche specialist that appeals to different target groups with its various brands, such as HOKA, UGG, Teva and Sanuk, and thus achieves a broad market presence.

The focus on health and wellness, outdoor activities and sustainable products addresses growing consumer needs and opens up numerous growth opportunities for Deckers. However, the potential for expansion abroad and the increased focus on e-commerce also represent further great potential. Strategic investments in digital platforms and the direct-to-consumer business strengthen customer loyalty and thus potentially improve profit margins.

The long-term prospects for Deckers are therefore promising. This is also the view of analysts, who believe that the company will achieve double-digit annual growth in earnings per stock in the future. With an expected price/earnings ratio of 28, the Deckers stock appears to be fairly valued. However, this only applies if the company consistently delivers double-digit EPS growth in the coming years. This may well be realistic, but the clearly expected slowdown in growth for the full year 2025 should be monitored. If this is a chronic weakness, for example due to increasing competition, the risk would be much greater and the valuation too high.

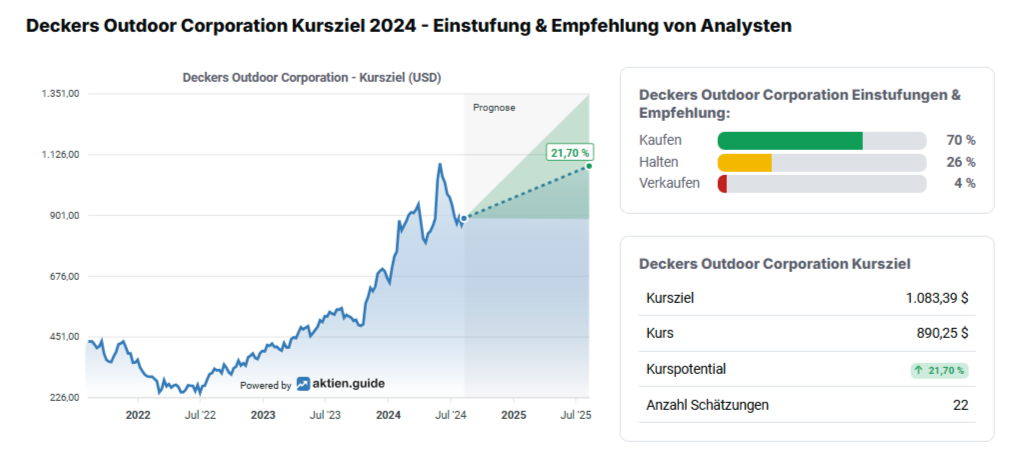

Source: Analysts' opinions on Deckers Outdoor stocks

Analysts tend to view the stock in an optimistic light. 70 percent recommend buying the stock. The average target price is USD 1,083.39, which still represents a respectable potential of over 21 percent. With this discount, the market seems to be compensating for the risk described.