Table of Contents

The stock of Meta Platforms (ISIN: US30303M1027) is the focus of much discussion as the company continues to make headlines for both its market position and its transformative strategy in the digital space.

Meta has long since become one of the largest and most influential companies in the tech industry, shaping the digital landscape not only with social networks such as Facebook and Instagram, but also with forward-looking technologies such as the Metaverse and VR and AR innovations.

Source: Development of the Meta Platforms stock price

At USD 1.8 trillion, market capitalisation has long since passed the trillion mark. It is not far off becoming the most valuable company in the world. The stock price increase of over 50 per cent last year is a testament to a particularly dynamic performance.

At times, things did not look so good, as our last stock analysis of Meta Platforms stocks showed. The main factors weighing on the stock price were a gloomy economy and the promise of betting billions on a technology that is not yet mature and established, such as the metaverse – at the expense of shareholders, of course. And most recently, the rise of the Chinese social media platform TikTok and a slowdown in the advertising industry have also caused additional worry lines.

In this update, we would like to take a closer look at how operations have progressed since then, and what the biggest issues are for Meta Platforms shares in operational terms and at present. One thing is clear: a lot has changed for the better.

Company profile – market leader in social media platforms

Meta Platforms, with a market capitalisation of $1.8 trillion, is one of the largest technology companies in the world. Founded 21 years ago in Cambridge, the company grew largely through the social network Facebook. Then, as now, it was at the forefront of developments in the digitalisation of social contacts. Over the years, the start-up has developed into a market leader in the social media sector through further innovations, but mainly through acquisitions (WhatsApp, Instagram).

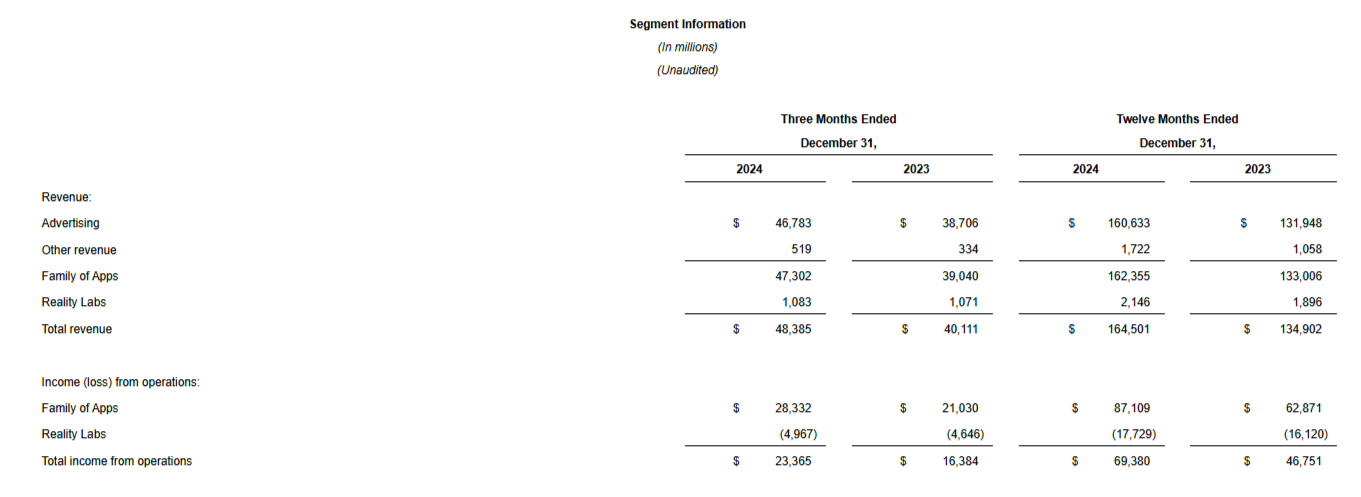

Source: Meta Platforms Q4-Earnings Release 2024

Today, Meta Platforms earns most of its money from advertising (Advertising) displayed on its platforms. In the segment reporting, this is shown under Advertising. Together with other revenues, they form the Family of Apps. The last major segment, Reality Labs, refers to a new vision of social communication on the internet – the metaverse.

Advertising

Let's move on to the first segment. Meta Platforms has grown and become successful primarily through its data-driven advertising business. The company generates a large share of its revenue from personalised advertising on platforms such as Facebook, Instagram and Messenger. Thanks to extensive user data, advertisers can run targeted campaigns that are tailored to the interests, behaviour and location of users. This targeted approach is revolutionary because it is highly efficient and avoids the high wastage rates of traditional advertising – not without criticism, but more on that later. This is how Meta Platforms was able to quickly develop into one of the leading providers in the digital advertising market behind Google, a subsidiary of Alphabet. In 2024, an incredible 161 billion US dollars were generated from advertising revenue, which corresponds to more than 97 percent of total revenue.

Other revenue

In addition to the advertising business, Meta generates additional revenue from ‘other revenue’. This includes the sale of hardware products such as the VR headset Meta Quest and services such as fees for certain digital transactions. Although this source of revenue is smaller than the advertising business, it is becoming increasingly important as the hardware business expands. At $1.7 billion in fiscal year 2024, other revenues account for just over one per cent of total group revenues.

Family of Apps

The advertising business and other revenues are combined in the ‘Family of Apps’ segment. It includes the Facebook, Instagram, Messenger and WhatsApp platforms. These services form the basis for Meta's social ecosystems and offer users a wide range of options for communication, networking and entertainment. Meta Platforms monetises this segment primarily through advertising, but plans to offer more paid subscription services in the future. There is talk of the development of Whatsapp into a super app that does everything. An operating profit of $87.1 billion represents high profitability (operating margin: 53 per cent). However, advertising revenues are also extremely cyclical and dependent on the economy. Investors would welcome a stronger focus on recurring revenues.

Reality Labs

With Reality Labs, Meta Platforms is pursuing a long-term vision of building the metaverse. This segment focuses on the development of virtual reality and augmented reality technologies. This includes the development of hardware such as the Meta Quest and software platforms for immersive experiences. Although Reality Labs is currently incurring high losses, Meta sees it as a strategic growth area for the future. But perhaps it is also the billion-dollar grave of an entrepreneurial vision of the eccentric Mark Zuckerberg. So far, this can only be guessed at.

In the past financial year 2024, a modest $2.1 billion in revenue was generated here. At 13.2 per cent, revenue growth is not showing any dynamic development either. The segment is highly deficient, with an operating loss of $17.7 billion.

Dynamic markets

Meta Platforms is active in several global markets that include various technologies and services. The social media giant is particularly active in the digital advertising market, in the field of social networks and in the emerging market of virtual and augmented reality. All of these markets are intertwined. Let's take a look at what makes them tick.

First of all, there is the digital advertising market. As we have already learned, this is Meta's core business area. Here, the company competes with tech giants such as Google, X, Reddit, Amazon, Microsoft, and now also Netflix, with each having its specialisation. However, only Google or its parent company Alphabet is really significant.

The market for online advertising is characterised by a high level of dynamism, data-based targeting and, of course, high growth potential. In contrast to traditional advertising, online advertising enables a targeted approach to users based on their interests, behaviour and geographical data. The most important channels include search engine marketing, social media, display advertising and video ads. Automated advertising technologies such as programmatic advertising play a central role. But trends such as the development towards mobile devices and the tightening of data protection regulations such as the GDPR are also continuously changing advertising strategies. The large user base on platforms such as Facebook and Instagram creates ideal access for Meta Platforms to the global online advertising market, which appeals to both large companies and small and medium-sized enterprises.

Another important market segment is the area of virtual and augmented reality. With its Reality Labs, Meta is pursuing the goal of building the so-called Metaverse, a digital world for immersive social, economic and creative interactions. The market for VR and AR technologies is still emerging, but is considered potentially revolutionary for numerous industries, including gaming, education and teleworking. In addition, Meta is entering the hardware market with products such as the VR headset Meta Quest and smart glasses. These products are primarily available in the United States and Europe, where the acceptance of innovative technologies is highest.

Competition from Meta Platforms

Competition in the market in which Meta Platforms operates is extremely intense and diverse. However, one of Meta Platforms' major competitive advantages is its user base, which benefits from a network effect. Almost everyone uses Meta Platforms because it is where the largest base of information is found and one's own social needs are best met. It is therefore a deep moat of the business model.

In the area of digital advertising, Meta Platforms primarily competes with companies such as Google/Alphabet and Amazon, which also offer data-driven and highly personalised advertising solutions. While Google plays a leading role with its dominant search engine and YouTube business, Amazon scores with advertising within its e-commerce ecosystem. But Netflix is also entering this market with its advertising-financed environment of the subscription model. In the social media sector, platforms such as TikTok/Bytedance, Snapchat/Snap and X (formerly Twitter) are in direct competition with meta platforms. In particular, TikTok has become a serious competitor for Instagram with its rapidly growing user numbers and creative short video formats. The important functions were copied by meta a long time ago, but the competitor is far from obsolete. This example shows once again that meta platforms can be subject to disruptive threats at any time.

Finally, in the emerging market of virtual and augmented reality, Meta Platforms is competing with companies such as Apple (with Vision Pro), Microsoft (HoloLens) and specialised providers such as HTC.

Other technologies in the Meta Platforms portfolio

However, the technology sector is an extremely dynamic environment. Meta Platforms is keeping pace and is increasingly delving into other areas of technology. The Metaversum is probably the area in which it is most deeply involved. I see the company, which is characterised by Mark Zuckerberg as a visionary, as the market leader here. But Oculus also plays a leading role in the hardware segment. This was most recently expanded to include the Orion data glasses.

Another important area of technology is blockchain technology. In the past, Meta has launched initiatives such as Libra (later renamed Diem) to create a digital currency and financial ecosystem. Although the project was slowed down by regulatory hurdles, blockchain technology remains a long-term interest of Meta, particularly in connection with digital assets and decentralised applications.

Meta also tended to react quickly to the release of OpenAI's ChatGPT. Here, it countered with LLaMA (Large Language Model Meta AI). LLaMA is a family of large language models trained to produce human-like text output. They have the ability to operate in a variety of contexts and tasks, from text creation to complex text comprehension tasks. With LLaMA, Meta is pursuing a strategy of developing powerful AI models that are more efficient and scalable than other well-known models. A key point here is that Meta is making the model available as open source. This means that researchers and developers worldwide can access the model and further adapt and improve it. By contrast, models like ChatGPT are not openly accessible. Meta sees LLaMA not only as a tool to improve its own platforms, but above all as a way to promote the development of AI in the broader scientific and technological community.

Finally, Meta Platforms is also innovating in the area of data infrastructure and cloud computing to further increase the capacity and scalability of its platforms and improve the user experience. Investments in modern data centres and cloud infrastructures make it possible to efficiently serve billions of users worldwide. To this end, Mark Zuckerberg's team is thinking creatively. A 40,000-kilometre undersea cable around the world is intended to bring the goal of total connectivity closer.

These broad technological investments show that Meta Platforms not only wants to position itself as a social media company, but also as a leading innovator in the digital future, with a clear focus on immersive digital worlds, AI-supported systems and blockchain technologies.

Criticism and regulatory pressure

But it is not only the threat from competitors that is significant. Meta platforms have been the focus of intense criticism and increasing regulatory pressure for years. One major point of criticism concerns user data protection and privacy. The mass collection, processing and monetisation of user data led to concerns about the protection of personal data early on. Scandals such as the Cambridge Analytica case ultimately confirmed the risks of uncontrolled data sharing. In addition, the people behind Meta Platforms have repeatedly been accused of not doing enough to stop the spread of disinformation, hate speech and extremist content. Critics complain that the platforms' algorithms promote content that aims to sensationalise and polarise in order to increase user engagement.

Another point of criticism is the company's potentially anti-competitive behaviour. Authorities in the US and Europe have launched investigations into alleged antitrust violations, including its aggressive acquisition policy (e.g. Instagram and WhatsApp) and its market power in the digital advertising business. There have been frequent calls for the social media giant to be broken up. In the US, there are always antitrust lawsuits and discussions about breaking up large tech companies. However, nothing has happened so far.

What is clear, however, is that regulatory pressure is increasing worldwide. In the EU, the GDPR has been forcing Meta Platforms and its competitors to adopt stricter data processing policies for some time, while the Digital Markets Act (DMA) regulates companies with gatekeeper status, such as Meta Platforms, more strictly. In addition, Apple's transparency in app tracking poses a major challenge, as users can now actively object to tracking, which directly affects Meta Platforms' advertising revenue. Overall, however, this has done little harm to the advertising business so far. Probably not without reason: with the help of AI, Meta Platforms can now also guess who is sitting behind the screen.

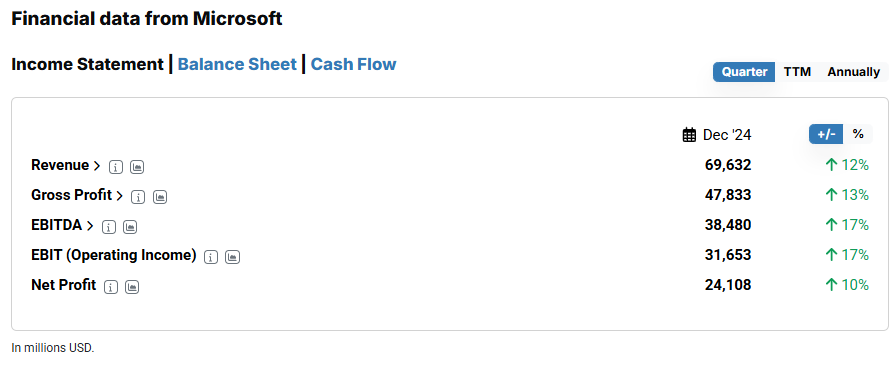

The last Meta Platforms quarterly figures from December 2024

Despite major challenges, the figures for the fourth quarter of 2024 are impressive. A 21 per cent increase in revenue to 48 billion US dollars is a testament to the company's particular momentum. From Meta Platforms' point of view, the advertising market continues to develop well. Especially in comparison to the previous quarter, when revenue growth of 19 per cent was still achieved. Explosive growth rates are being recorded on the earnings side. Quarterly operating income rose by 73 per cent to 30 billion US dollars.

Source: Financial data from Meta Platforms; StocksGuide

The growth was driven primarily by strong advertising business, which has picked up again thanks to the economic situation. However, the strong core business also provided a tailwind. The number of daily active users in the Family of Apps averaged 3.4 billion in December 2024 – an increase of 5 per cent year-on-year.

Ad impressions delivered increased by 6 per cent in the fourth quarter alone and by 11 per cent over the year as a whole. Average price per ad also developed positively, rising by 14 per cent in the fourth quarter and by 10 per cent over the year as a whole.

By contrast, costs and expenses increased at a slower rate. They totalled 25 billion US dollars in the fourth quarter and just over 95 billion US dollars for the year as a whole, which corresponds to a moderate increase of 5 per cent and 8 per cent year-on-year. Lower provisions for litigation resulted in a positive effect of 1.6 billion US dollars.

By contrast, investments in property, plant and equipment amounted to almost 15 billion US dollars in the fourth quarter and almost 40 billion US dollars for the year as a whole. They could be significantly higher in the future, but more on that in the forecast section.

By contrast, there was a sharp step on the brake with regard to share buybacks. No more treasury shares were repurchased in the fourth quarter. By contrast, the buyback volume for the full year 2024 was almost $30 billion. Meanwhile, dividends continue to flow cheerfully: shareholders enjoyed over $1.27 billion in the fourth quarter and $5.07 billion in the full year 2024. They could continue to rise given the tech company's high liquidity.

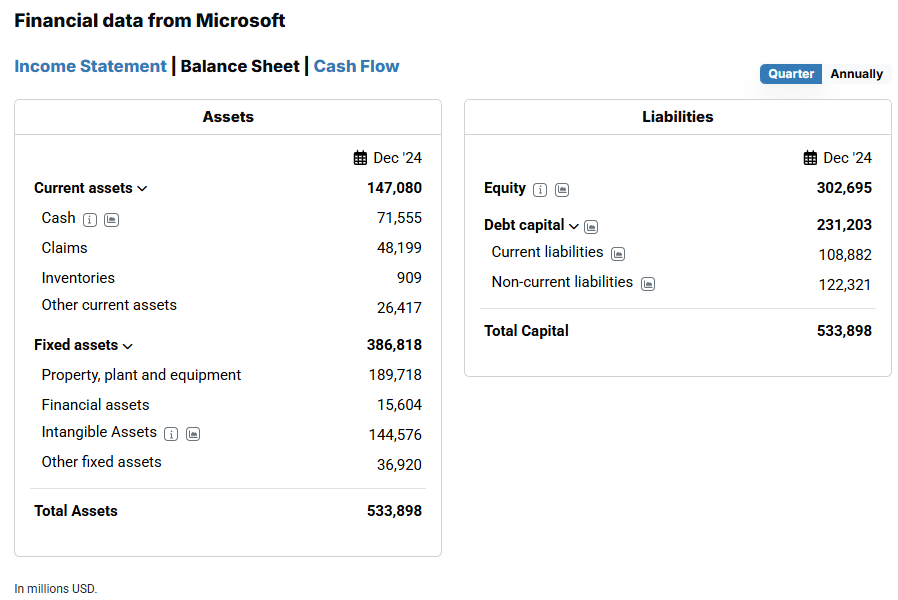

Source: Balance sheet data from Meta Platform; StocksGuide

At the end of the year, Meta had liquid funds and marketable securities totalling $78 billion. The equity ratio comes to 66 per cent. In net terms, billions more flow into the company's coffers every month.

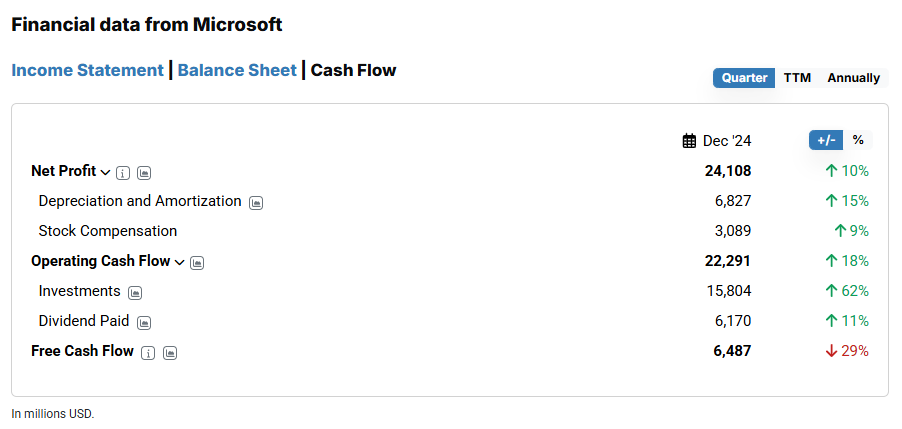

Source: Cash flow statement of Meta Platforms; StocksGuide

The free cash flow was most recently $13.6 billion in the fourth quarter and $54 billion in the full year 2024 – and rising sharply.

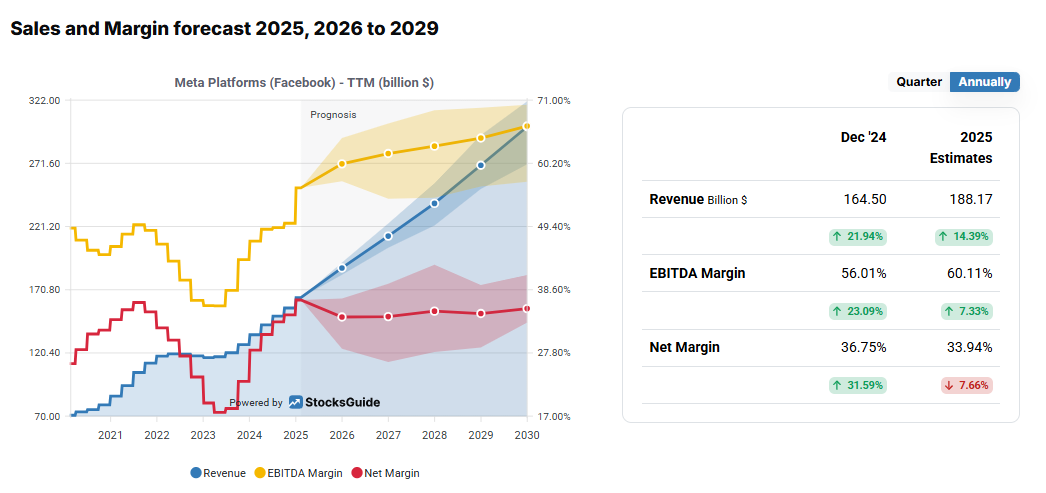

Meta Platforms Stock Forecast 2025

The future should also continue to look bright: Meta Platforms is optimistic about the first quarter and the full year 2025. For the first quarter, for example, revenue is expected to be between $39.5 billion and $41.8 billion, which represents year-over-year growth of 8 to 15 per cent. Adjusted for currency effects, growth would be as high as 11 to 18 per cent, as currency fluctuations represent a headwind of around three per cent. In addition, the absence of a leap year day in the comparison period has a negative impact on growth. However, the consistently high investments in the core business should also have a positive impact over the entire year 2025 and support strong revenue growth. Despite the favourable outlook, there is a fly in the ointment here: growth is well below the growth rates of previous quarters. One explanation, of course, lies in the cyclicality of the advertising business, from whose positive momentum Meta Platforms benefited last year. The weaker growth could indicate a return to normal, but also a saturation trend.

Meta Platforms estimates that total spending in 2025 will be between 114 and 119 billion US dollars. The biggest cost drivers are likely to be infrastructure costs (investment in AI servers) due to higher operating expenses and depreciation. However, the continued high salaries of employees will also be a significant cost factor. However, they are also extremely important for the technology group to expand its technical staff in the areas of infrastructure, monetisation, reality labs, generative AI, and regulation and compliance. Overall, Meta Platforms is growing again in terms of the number of employees – after the mass layoffs in 2023. In 2024, it rose by 10 per cent to 74,067. Investments in tangible assets are expected to be between 60 and 65 billion US dollars in the new fiscal year 2025, thus further fuelling the high level of investment. A large proportion of these funds will continue to flow into the core business, with additional funds being allocated to generative AI projects.

Analysts also view the development positively. They expect significantly higher revenues in the medium term – in the best case, over $320 billion in 2030. Annual revenue growth is expected to remain consistently in double digits. Only a slight slowdown in growth is expected.

Source: Analysts' opinions on Meta Platforms stock; StocksGuide

Due to the high scalability, margins should also continue to rise in the end. Analysts see at least the potential for the EBIT margin of 66 per cent in 2030, which represents an increase of around 10 percentage points over the previous figure.

By contrast, the net margin should remain at a high level. However, a slight decline is forecast for 2025. The main reason for this is likely to be the high level of investment, which is putting pressure on the margin.

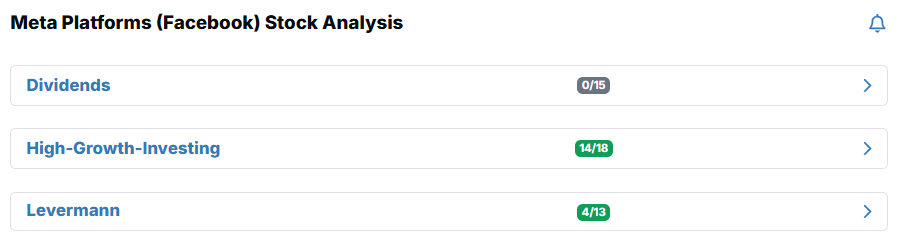

Important key metrics for Meta Platforms stock from the Levermann and HGI analyses

Currently, Meta Platforms stock is in top scorer mode in both the Levermann strategy and the Growth strategy, which could ideally be a buy candidate.

Source: Positioning of the Meta Platforms stock in the strategy analyses; StocksGuide

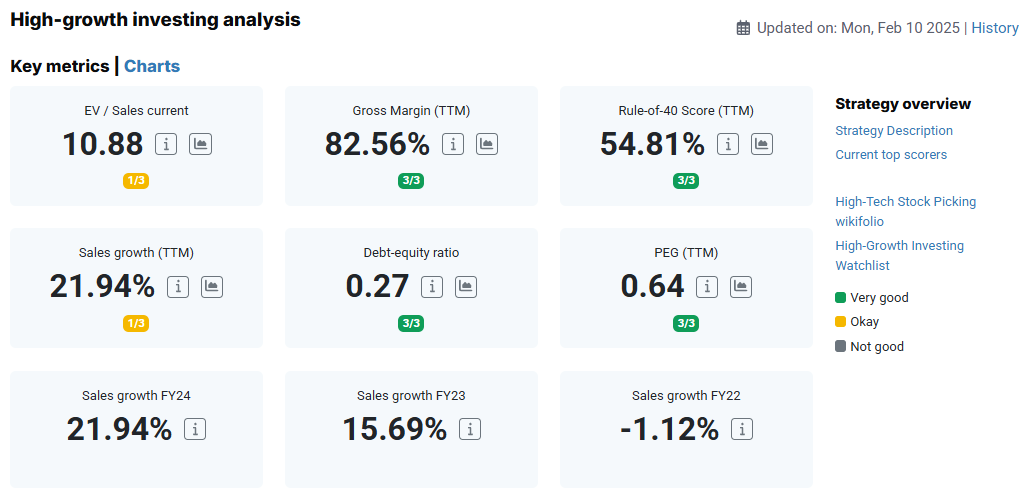

The high-growth investing analysis of the Meta Platforms stock shows a convincing overall development. The company impresses above all with its high profitability and financial stability. The gross margin is at an exceptionally high level and underlines the efficiency of the business.

Source: HGI score of Meta Platforms stock; StocksGuide

It is also positive that revenue growth has stabilised in recent years and is once again showing a clearly positive dynamic. After a slight decline in 2022, Meta already recorded moderate growth in the following year, which accelerated further in 2024. This reinvigorated revenue growth indicates that the company has been able to successfully respond to new market demands. And indeed, Meta Platforms has overcome the cyclical advertising downturn, kept its competitor TikTok at arm's length and actively cultivated its community. The low level of debt (leverage ratio: 0.3) is also a positive factor. Here, Meta shows a high degree of financial stability, giving the company room to manoeuvre for investments and innovations. In addition, the company has a very attractive growth and profitability ratio, which is reflected in an impressive Rule of 40 score (55 per cent).

Overall, the Meta Platforms stock achieves a total score of 14 points in the HGI analysis. This means that only four points are missing to achieve the maximum score of 18 points. The main reasons for this are the weak sales growth and the high valuation based on the EV/Sales multiple. All other key figures were awarded the maximum score of three points.

Source: Levermann score for Meta Platforms stock; StocksGuide

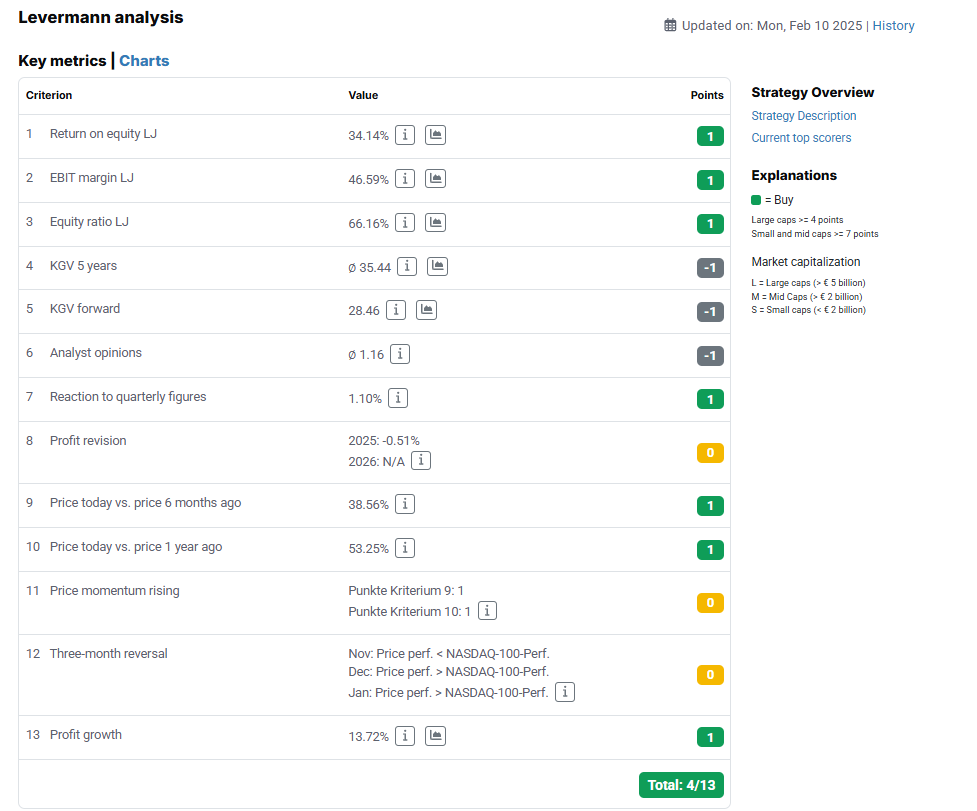

The Levermann analysis, which also takes into account technical key figures in addition to fundamental key figures, also looks good. With a total score of four points, the critical threshold for becoming a top scorer was only just exceeded, but here too the share can be described as a buy candidate.

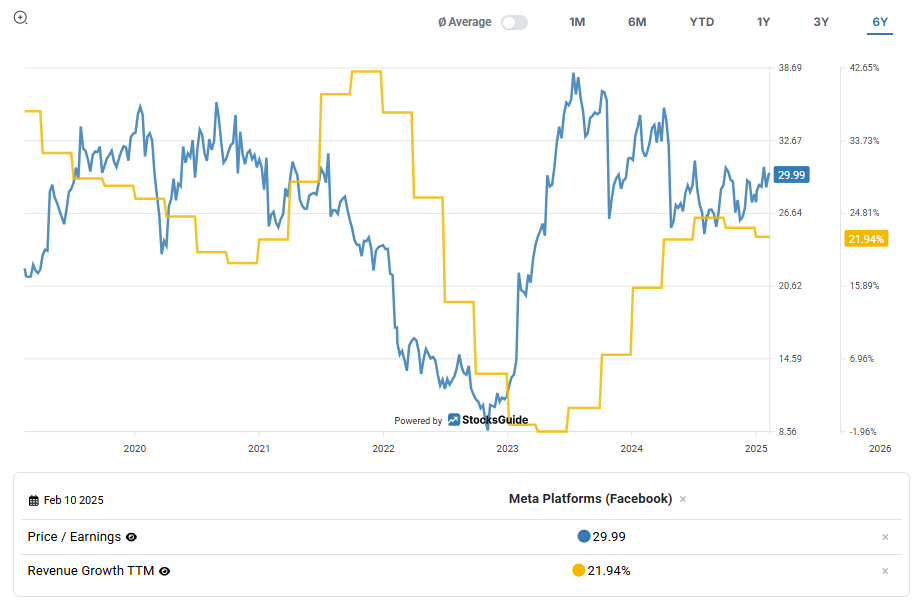

In addition to the well-known fundamental data, the stock is particularly convincing due to a positive short and medium-term price development with good reactions to the publication of the last quarterly figures. Here, too, the high valuation has a negative impact. However, the P/E ratio is used as a profit multiplier. And at just under 35, this is very high for the average of the last three years and the expected two years.

Valuation of the Meta Platforms stock

The valuation of Meta Platforms' shares initially presents a complex picture that harbours both opportunities and risks for investors. On the one hand, the company is well positioned to generate future returns based on its revenue growth and solid financial fundamentals. The high gross margin and low leverage also speak in favour of Meta's shares.

Despite these positive aspects, however, the stock is currently not cheap at an EV/Sales ratio of almost 11 and a stock price close to new all-time highs. A similar picture is shown by the P/E ratio based on the last twelve months (TTM). At 29, it is even slightly above the historical average of 26.5.

However, it should be noted that growth has improved significantly of late. Moreover, many regulatory and competitive negative scenarios have not materialised. Furthermore, the initially expensive expansion into the metaverse has been harmonised and advertising revenues recovered well in 2024. The result: reinvigorated growth of over 20 per cent.

Source: Historical valuation and growth rates of Meta Platforms' stock

It is therefore not surprising that the tech stock has a relatively low PEG of 0.6. Such low values indicate that the valuation could still be reasonably justified in relation to the company's growth. Only under this assumption could the Meta stock still be considered cheap – provided that growth does not disappoint in the future either.

Ultimately, the valuation depends heavily on future growth expectations and, of course, capital expenditure. If Meta Platforms succeeds in maintaining its own revenue and earnings growth at a high level and continues to achieve high margins, the stock could still have potential even at its current valuation. If it does not succeed, the valuation could pose a risk.

Conclusion on the Meta Platforms stock

In summary, I believe that Meta Platforms' stock has many positive arguments despite its high valuation. It impresses with high profitability, a solid financial base and stable sales growth, which has picked up momentum again in recent years.

In particular, the high free cash flows ensure that the incredible sums of money needed to develop new technologies can be raised. However, they are initially at the expense of shareholders. And many here still lack the imagination to see whether the metaverse can be a long-term success. After all, Mark Zuckerberg is investing more than 17 billion US dollars a year in this venture, which is significant. In the long term, further investment would probably be needed to get the market moving. The results of investments in AI technology are likely to be more concrete. Here, the main focus is on investments in AI infrastructure such as data centres, software assistants or the expansion of development teams.

Meanwhile, there is little sign of anything new on the competition front. On the contrary: Tiktok was briefly taken offline because the US business had not yet been sold to a US company. It is currently only running thanks to a three-month extension granted by the US president. It is also striking that Alphabet, the market leader in the advertising business, grew significantly more slowly than Meta Platforms in both the fourth quarter and the full year 2024. In my opinion, this points to an outperformance by Meta. However, new variants of social networks, such as Reddit and Discord, are emerging and are proving very successful. It is important for the meta platforms to remain vigilant here in order to avoid a new threat, such as that posed by the rise of TikTok.

The momentum in the advertising business is also likely to continue in the following quarter. However, Facebook itself expects lower growth rates for the full year 2025 than were recently achieved in the full year 2024. In the medium term, however, these could still be in double digits.

When evaluating, it should be noted that the stock is currently trading at a premium due to its market position and future strategy. This could be seen as a risk if the company is unable to achieve the expected growth rates or encounters unforeseen challenges. But then again, we are still in a growth market for online advertising. And this should continue to offer further potential in the future. Assuming that Meta Platforms' earnings develop similarly to its dynamic revenue growth, the current valuation of Meta Platforms shares could well be justified – and even offer further potential. For investors with a long-term view who believe in the company's potential and its technological vision, they could ultimately be an interesting option. However, it remains important to monitor the company's further development closely in order to identify risks at an early stage.

Source: Analysts' opinions on Meta Platforms stock; StocksGuide

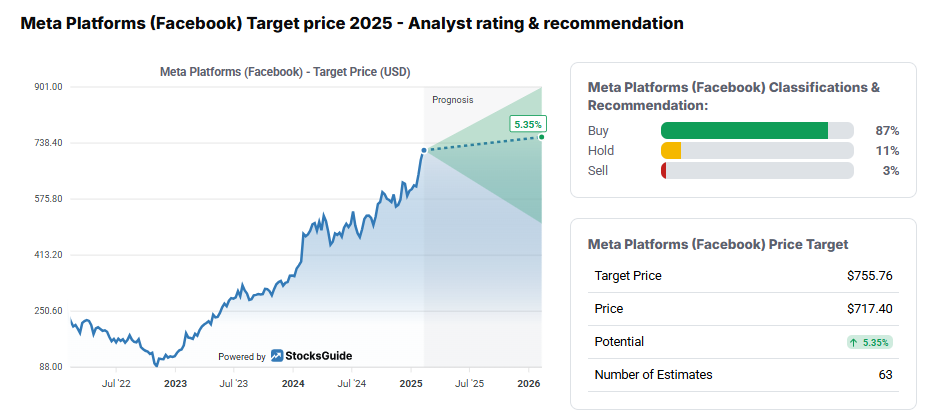

Analysts also see more opportunities than risks. 87 per cent of them consider the share to be a buy. Only 11 per cent advise holding and very few advise selling. The average price target of $755 is just under six per cent away from the current price, so a lot could already be exhausted.