Table of Contents

-

CRH and the competition: the market leader has visible strengths

-

Important key figures for CRH stocks from the dividend analysis

CRH plc (Symbol: CRH) is the largest listed building materials manufacturer in the western world and occupies an important position in the global construction industry. The company generates the majority of its sales in the USA and Europe, two of the most important and dynamic markets in the world. Particularly in view of the ailing infrastructure and the relocation of important industries, an exciting dynamic could develop here in the future.

CRH benefits from clear competitive advantages such as strong geographical diversification, a broad product portfolio and efficient cost management, which secure its market leadership. However, a key growth driver for CRH is strategic acquisitions, with which the company is continuously expanding its reach and range. As a result, sales and earnings have increased significantly in recent years. The stock price has also rewarded this development with an increase of 556% over the last ten years. Source: CRH stock price

Source: CRH stock price

Despite its strong market position, the valuation of CRH stocks remains attractive with a P/E ratio of 15 and a respectable dividend yield. However, there are also risks, as the following analysis of CRH stocks will show.

The most important facts in brief

- CRH is the largest listed western building materials manufacturer

- Business is largely conducted in the USA and Europe

- Significant competitive advantages secure market leadership

- Takeovers drive growth, valuation is attractive

Company profile - leading building materials manufacturer

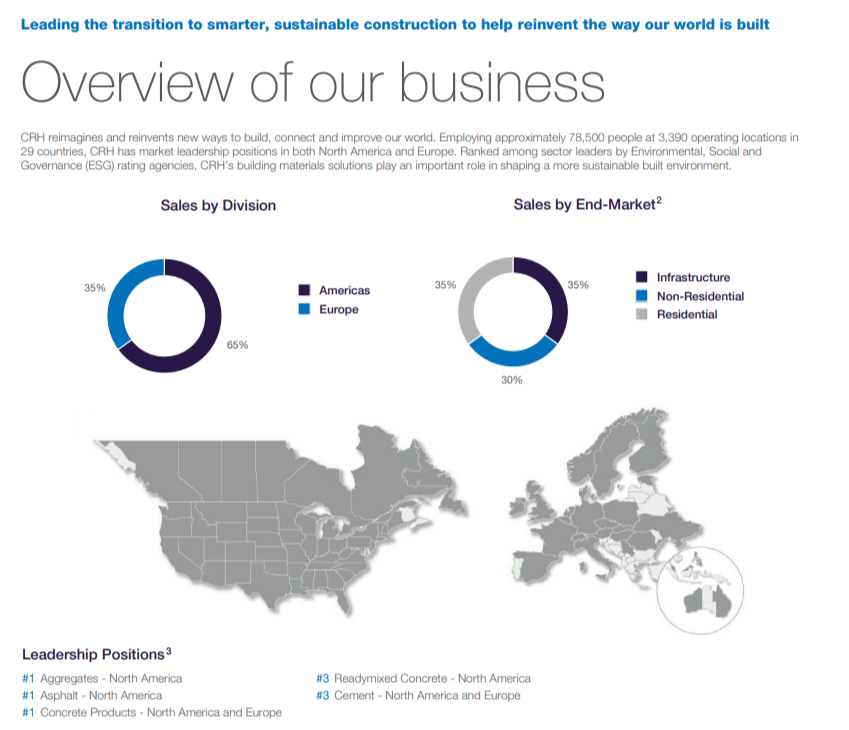

CRH plc is a leading company in the building materials industry. It was founded in Ireland in 1970 through the merger of Cement Limited (founded in 1936) and Roadstone Limited (founded in 1949). The Irish company grew rapidly through a series of acquisitions in Ireland, the UK and North America. In the decades that followed, CRH continued to expand internationally and diversified its businesses by acquiring companies in Europe, North America, Asia and other regions. Today, CRH is one of the world's largest building materials companies and operates in over 30 countries. However, the focus is on business in America and Europe. The company is particularly strong in the areas of infrastructure and residential construction as well as commercial real estate.

Source: CRH plc Annual Report 2023

In terms of market capitalization of 54 billion euros, CRH is significantly larger than its competitor Heidelberg Materials, which weighs in at 17 billion. Switzerland's Holcim (market capitalization of 48 billion euros) is hot on the Irish company's heels. Competitors such as Martin Marietta Materials (market capitalization of EUR 30 billion) and Vulcan Materials (market capitalization of EUR 29 billion) follow at a slight distance

CRH plc therefore operates in a highly competitive environment in which large multinational corporations dominate. Competition takes place both globally and locally, with price, product quality, innovation and service being important differentiating factors. In this industry, the local availability of raw materials, logistics and proximity to the market is crucial, which often leads to a high level of market concentration in certain regions. In some cases, monopoly-like structures can be established.

CRH classifies its business into the following areas:

-

Americas Materials Solutions

-

Americas Building Solutions

-

Europe Materials Solutions and

-

Europe Building Solutions

In the Americas Materials Solutions segment, CRH focuses on the production and sale of aggregates, asphalt, cement and concrete. These products are essential for the construction and maintenance of roads, highways and other infrastructure projects. In addition, CRH offers road and highway maintenance services in this segment. The focus is mainly on the North American market, particularly the USA, where the company benefits from government investment in transportation infrastructure.

The Americas Building Solutions segment is involved in the manufacture and sale of building products and solutions for residential, commercial and industrial construction. This includes products such as roof systems, windows, doors and prefabricated building elements. CRH serves the North American market in this segment and offers its customers both standard products and customized solutions for special construction projects.

CRH's Europe Materials Solutions segment primarily covers the production and sale of building materials such as cement, aggregates, concrete and asphalt in Europe. The products from this segment are used for a wide variety of construction projects, including road construction, residential construction and commercial construction projects. In this segment, CRH has a broad network of quarries, concrete plants and asphalt mixing plants throughout Europe and is a leading supplier in this market.

The Europe Building Solutions segment, on the other hand, focuses on the manufacture and sale of building products for building construction, including façade systems, roof elements, window and door solutions and prefabricated concrete elements. It primarily serves the European market and is aimed at customers in the residential, commercial and industrial construction sectors. CRH offers both standard solutions and customized products that are tailored to the specific requirements of its customers' construction projects.

Overall, CRH pursues a diversified business model with its segments, which is aimed at both the sale of building materials and the provision of construction and infrastructure services in order to cover various markets and customer needs worldwide. However, there is a focus on the western world.

Cyclical industry

The building materials industry is highly cyclical. Its performance is therefore closely linked to economic cycles. During economic booms, demand for building materials rises due to increased construction activity in the areas of residential construction, commercial construction and infrastructure projects.

Companies in the sector benefit from higher sales and profits in such times. However, during economic downturns or reviews, construction activity decreases, which tends to lead to lower demand for building materials. This can lead to overcapacity, price pressure and declining margins. Delays or cutbacks in government infrastructure projects can also have a negative impact on the industry.

Source: CRH plc Annual Report 2023

Source: Q2-2024 Investor Presentation CRH plc

Due to this cyclicality, companies such as CRH must be flexible in their business strategies in order to be able to react to economic fluctuations. The broader positioning with more in-depth services is a sensible step to compensate for fluctuations. However, the broader geographical positioning also reduces risks. Longer-term construction projects stand for planning security.

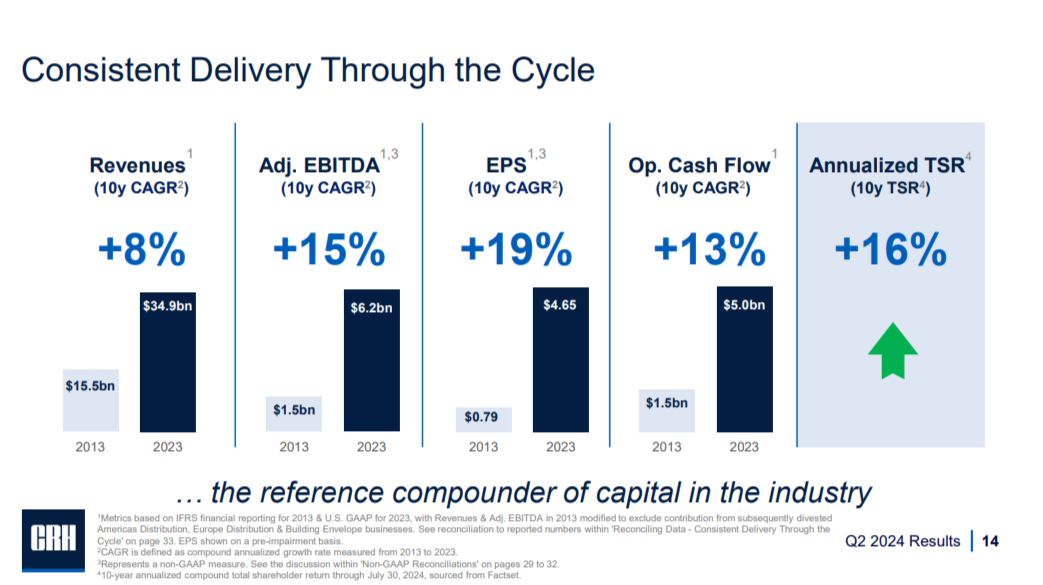

In the past, CRH has proven to be particularly good at making acquisitions. Since 1970, an average annual increase in value for stockholders of 15.7 percent has been achieved.

CRH and the competition: the market leader has visible strengths

Source:StocksGuide charts

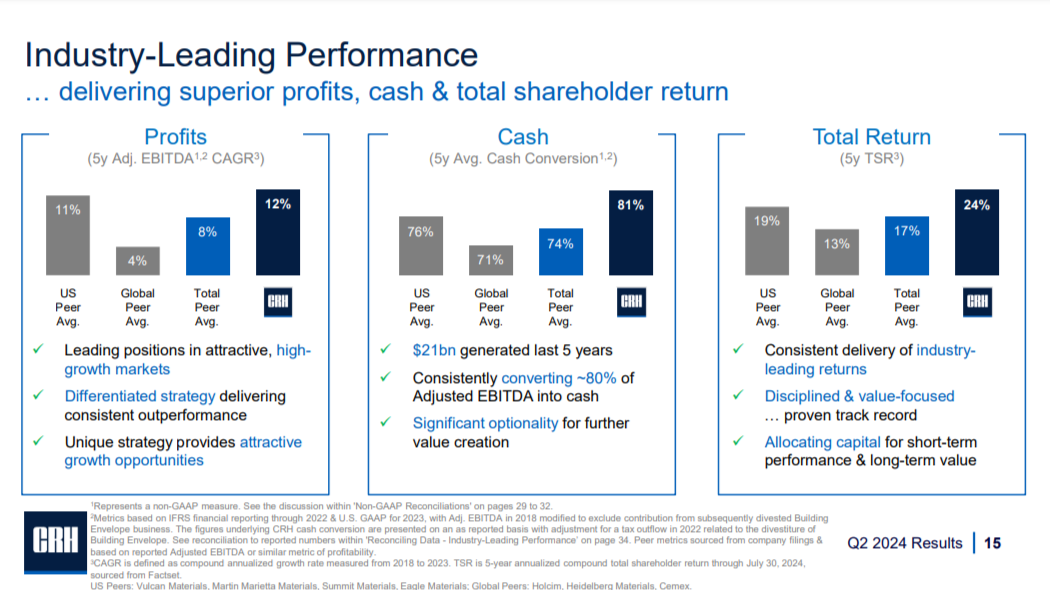

CRH plc has significant competitive advantages through its geographic diversification and strong market position, particularly in North America, as well as its extensive product portfolio covering a wide range of building materials and construction solutions.

Source: Q2-2024 Investor Presentation CRH plc

Efficient cost control and a successful acquisition strategy also strengthen the company's market position and enable it to react flexibly to market changes. The focus on sustainability and innovative building products also gives CRH an advantage in an increasingly environmentally conscious market environment.

The latest CRH quarterly figures from June 2024

Source: CRH stock Q2 2024 Results

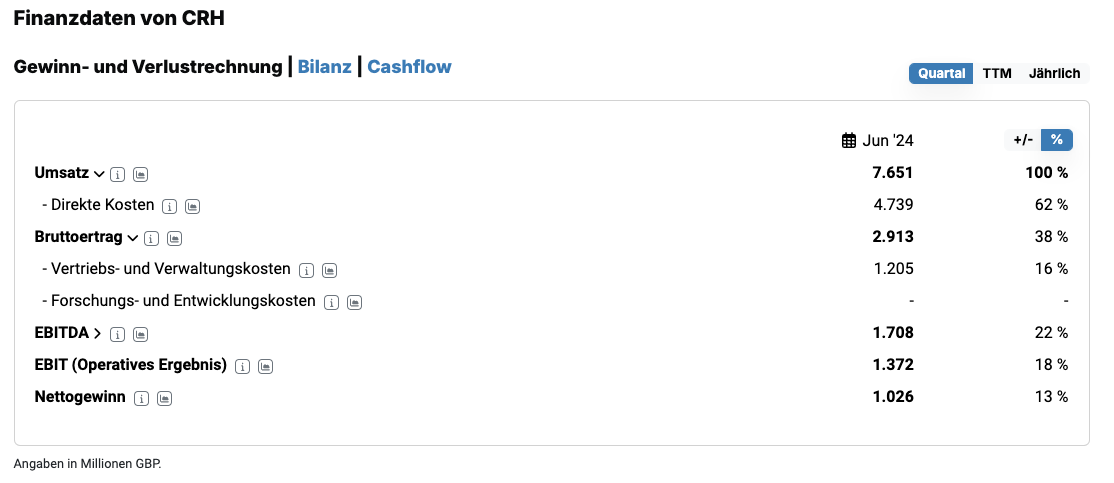

CRH plc has reported impressive results for the second quarter of 2024, showing that the company is well positioned despite challenging conditions - such as poor weather with no construction taking place.

Specifically, revenue fell by 1 percent to 9.7 billion US dollars in the second quarter of 2024. However, net income increased by 8% to USD 1.3 billion, while adjusted EBITDA grew at a double-digit rate.

What is particularly remarkable is how CRH not only manages to achieve stable sales in a difficult environment through targeted pricing and cost control strategies, but also to significantly increase profits. The consistent focus on a differentiated strategy is paying off here and shows that management is setting clear priorities.

The latest acquisitions and investments, such as the one in Texas and the majority stake in Adbri, appear well thought out and promise further growth in the long term. They are in line with the previous strategy of inorganic growth. The ongoing stock buyback and increased dividend also signal confidence in the company's future viability.

Overall, the first half of 2024 shows that CRH has mastered its challenges quite well and is taking advantage of opportunities to further strengthen its market position. It is therefore quite possible that 2024 will also be a record year for the company.

CRH stock forecast 2024

CRH's forecast for 2024 has been revised slightly upwards following the publication of the half-year figures, reflecting the strong financial performance, the positive business environment and the successful completion of recent portfolio transactions.

Source: Q2-2024 Presentation CRH plc

In North America, where around two thirds of adjusted EBITDA is generated, the company anticipates benefits from major infrastructure projects and increased investment in key non-residential segments.

In Europe, on the other hand, robust demand is expected in the infrastructure sector and in key non-residential markets, supported by disciplined cost control. The company sees opportunities in the area of high-tech production facilities.

In contrast, residential construction, particularly in the new construction sector, remains rather subdued in all markets in the short term. However, provided that weather conditions develop seasonally as normal and no unforeseen events occur, CRH remains optimistic about the coming year.

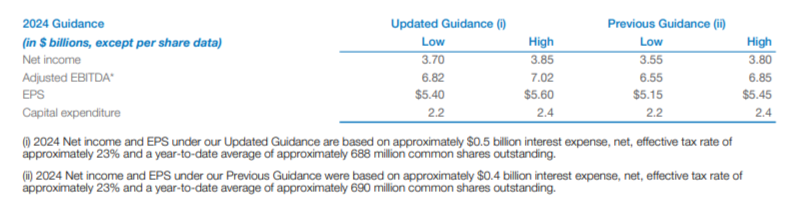

Source: Quarterly report Q2-2024, CRH

Specific annual targets have also been defined in figures. Net profit for the year is expected to be between 3.70 and 3.85 billion US dollars. This is a significant improvement on the previous forecast of USD 3.55 to 3.80 billion. The situation is similar for adjusted EBITDA and earnings per stock. The latter is expected to be between 5.4 and 5.6 US dollars.

Important key figures for CRH stocks from the dividend analysis

A particular highlight of CRH stocks is the regular dividend payments, which have also risen visibly over the long term in the past. Starting from a value of GBP 0.10 in 1999, an exceptionally high amount of GBP 2.36 was recently paid out.

Source: CRH stock dividend score

In the dividend analysis, the CRH stock impresses with a historically high dividend yield of over 4%. The payout ratio is conspicuously low, averaging less than 50% over the last three years. However, it should also be noted that this is a capital-intensive business model that is driven by acquisitions. Investments of between USD 2.2 billion and USD 2.4 billion are expected for the current financial year, which is no small amount given adjusted EBITDA of USD 6.2 billion in the 2023 financial year.

Nevertheless, the stock is also convincing in terms of dividend growth in the dividend analysis - thanks to the operational growth. Dividends have increased by almost 30% in the last five years. Points were only deducted for continuity over ten years and the current dividend yield. With 13 out of a possible 15 points, CRH stocks are a top scorer in the dividend strategy.

This status could also be maintained in the future, although the recent exceptionally high dividend is expected to be lower in the future. According to analysts, however, the expected value of GBP 1.12 for the 2024 financial year should rise significantly again in the coming years.

Valuation of the CRH stock

With an expected P/E ratio of 15.1, the valuation of CRH stocks is not objectively high. The sales growth of 5.4% in the last twelve months appears solid. Analysts' forecasts also assume sales growth in the mid-single-digit range in the medium term, which may support the narrative of a fair valuation.

Source: CRH stock valuations

But there are also negative points. Over USD 10 billion in long-term debt was on the books at the end of the last quarter. In addition, the numerous acquisitions have led to high goodwill of USD 10.2 billion. Although both figures are sustainable due to the strong adjusted EBITDA, they can also pose particular risks if the acquired companies fail to meet expectations.

Conclusion on CRH stocks

As the largest listed building materials manufacturer in the West, CRH plc has a solid foundation and benefits from a strong market position in the US and Europe. The combination of geographical diversification, an extensive product portfolio and a successful acquisition strategy secures the company sustainable competitive advantages and continuously drives its growth. stockholders also benefit from this.

Despite CRH plc's strong market position and growth prospects, there are also some risks that need to be kept in mind. As a cyclical company, CRH is susceptible to economic downturns, which can visibly affect construction activity and therefore demand for building materials. Residential construction in particular, which is already showing signs of weakness, could have a negative impact on business if this trend continues. In addition, like many international companies, CRH is exposed to geopolitical risks and currency fluctuations, which could be exacerbated by its broad geographical diversification. Finally, the continuous growth strategy through acquisitions harbors the risk of integration problems and unexpected costs that could reduce the expected synergies. Goodwill has already reached a substantial level and long-term financial debt is also high.

Source: Analysts' opinions on CRH stocks

Nevertheless, the majority of analysts see the stock as a buy. With 86% and 19 analysts respectively, the figure is actually quite high. In contrast, 10 percent and 5 percent of analysts see the stock as a hold or sell. The average target price of just under 22% is at an attractive level. This shows that the majority of analysts rate the opportunities higher than the risks.

With an attractive valuation and a positive outlook, particularly with regard to infrastructure investments, CRH remains a promising option for investors looking to benefit from the global construction industry in the long term.