Table of Contents

You have to break an egg to make an omelet. In industry, this means that equipment sometimes breaks or needs to be repaired. This is where Snap-On (ISIN: US8330341012) comes in, providing the right tool for (almost) any repair.

Source: Snap-On stock

The company, based in Kenosha County, Wisconsin (USA), not only sells products it has developed itself, but also regularly acquires smaller manufacturers of repair or measuring equipment. This has enabled it to create a diversified product offering.

Another unique selling point is the combination of its own sales channels and an extensive network of franchisees. This reduces administrative costs and increases reach.

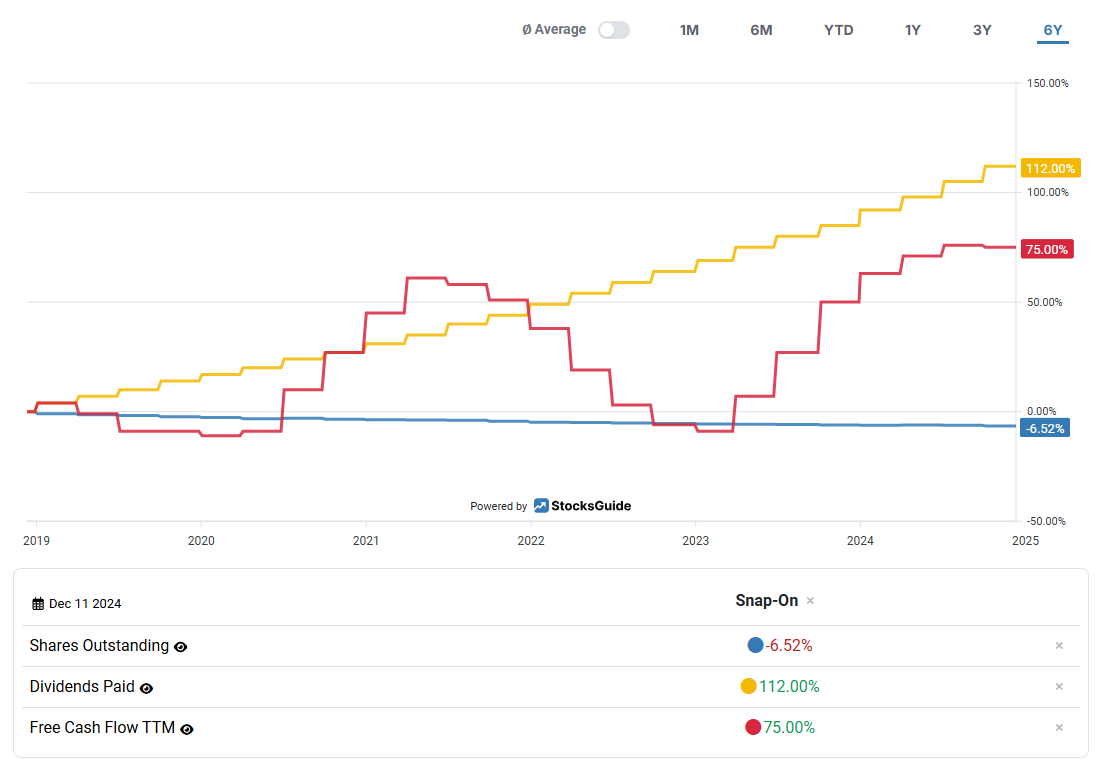

The resulting cash flows are not only used for new acquisitions. Snap-On's shareholders also benefit from the company's positive development.

Source: Snap-On Fundamental Charts

In recent years, not only has the dividend more than doubled, but the number of outstanding shares has also been reduced by more than one percent annually.

All these are sufficient reasons to take a closer look at Snap-On.

Company profile Snap-On – Tools for (almost) every repair

As early as 1920, engineer Joseph Johnson started developing the first simple tools, such as a wrench, in Milwaukee, Wisconsin (USA). In collaboration with his colleague William Seidemann, he developed various wrenches and ratchets. In 1923, the first patent was registered for “Ratchet No. 6”. Automotive companies and workshops appreciated the easy handling of Snap-On tools, so that by 1925 more than 165 salespeople were working for the company in the United States. In the decades following its foundation, the company repeatedly acquired smaller companies, not all of which were in the automotive sector.

The Snap-On portfolio also includes the German companies Hofmann and Cartec. Both companies manufacture equipment for the automotive industry. Hofmann's portfolio includes, among other things, car lifts and tools for tire balancing and tire changing. Cartec's product portfolio includes test equipment for checking CO2 emissions, headlight height and brakes.

Source: Brands Snap-On

Snap-on Tools today offers a wide range of products and solutions for repairs, diagnostics, measurements, tests and much more. Snap-on tools are used in a variety of sectors, including the oil and gas industry, the aerospace industry, the military, the automotive industry, railways, the manufacturing industry, agriculture and the medical sector.

In the US, independent store managers can decide to become a Snap-On franchisee. The franchisee receives support from Snap-On for initial financing, inventory and help with business registration. In addition, new franchisees have to complete a crash course. Snap-On wants to ensure that new franchisees get a basic understanding of their business so that both sides benefit from each other for as long as possible. In return, franchisees have to pay a fee for using the Snap-On brand and the marketing provided by Snap-On.

Source: Snap-On: New Franchisee

Snap-On received multiple awards for its franchise model last year. This has enabled the American company to continue to attract new franchisees and thereby expand its reach.

Acquisitions will continue to play an important role as a strategic corporate development measure in the future. In 2023, the company Saveteq was acquired for a purchase price of 3 million US dollars. With the acquisition of Saveteq, Snap-On is expanding its range of calibration solutions. Furthermore, Mountz was acquired for 39 million US dollars. With Mountz, Snap-On can further expand its portfolio of torque tools.

After an acquisition, the companies continue to operate under their existing name. This allows them to benefit from Snap-On's distribution channels and offer their products to a wider customer base. Snap-On does not need to develop any new products to achieve its targeted sales growth. This saves research and development costs.

Sales mix Snap-On stock

In fiscal year 2023, sales of $4.73 billion were generated.

Snap-On's sales mix is based on the various applications of its products.

Commercial & Industrial Group

The division for equipment for, for example, the military, aerospace or the oil and gas industry, achieved sales of approximately $1.46 billion, an increase of 4.26 percent over 2022.

With an increase of 14.4 percent, EBIT grew particularly strongly in this area. Although this area is the smallest segment of Snap-On in terms of sales, after Financial Services, it was the area that grew the most in terms of EBIT last year.

Snap-On achieves better margins here than in the other areas.

Snap-On Tools Group

The area around the workshops of franchisees in the US. Both the franchise fees and all sales for the US automotive sector belong to this segment. With sales of $2.09 billion, this segment accounts for around half of the sales of the three major segments. It grew by just under 1 percent last year and reflects the weakness of the US automotive industry in 2023. EBIT increased by 7.7 percent.

Repair Systems & Information Group

All sales of tools for the automotive industry outside the U.S. are attributed to this area. Sales in this segment increased by around 7 percent to $1.78 billion and EBIT reached an increase of 10 percent to $433 million.

Financial Services

At Snap-On, customers can use credit offers to finance the purchase of their equipment with debt capital.

This area reached sales of $378 million in 2023. Thus, this segment accounts for only 8 percent of sales.

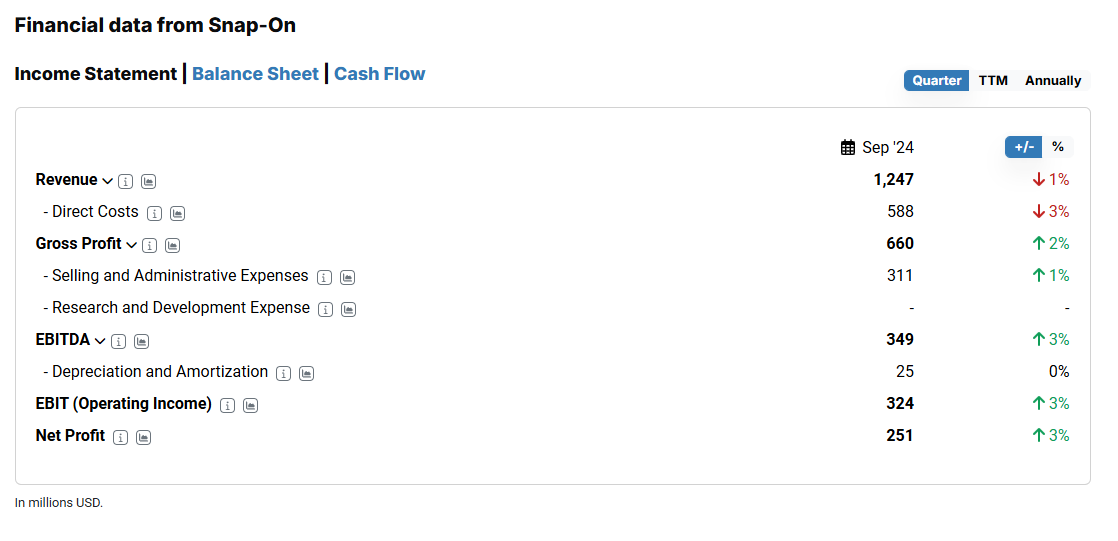

The last Snap On quarterly figures September 2024

Snap-On's most recently reported quarterly figures were celebrated by investors on the day of their publication with a 10 percent share price increase. However, revenue fell by 1 percent to $1.25 billion.

Source: Snap-On quarterly figures September 2024

The profitability picture was better. EBIT rose by 3 percent to $324 million and net profit of $251 million was reported. This was still 3 percent more than in the previous year.

Despite a generally weak economy in the automotive sector, Snap-On impressed with good cost management and very good margins for an industrial company.

Source: Snap-On quarterly figures with margins September 2024

The gross margin of 53 percent already shows significantly lower product costs than in the automotive sector, for example. By way of comparison, the German carmakers Porsche and Volkswagen have gross margins of 23 and 19 percent respectively. Automotive supplier Continental also has a gross margin of 23 percent.

Snap-On's EBIT margin of 26 percent indicates a lean administrative structure and low marketing expenses. In view of this, the net profit margin of 20 percent is no longer surprising.

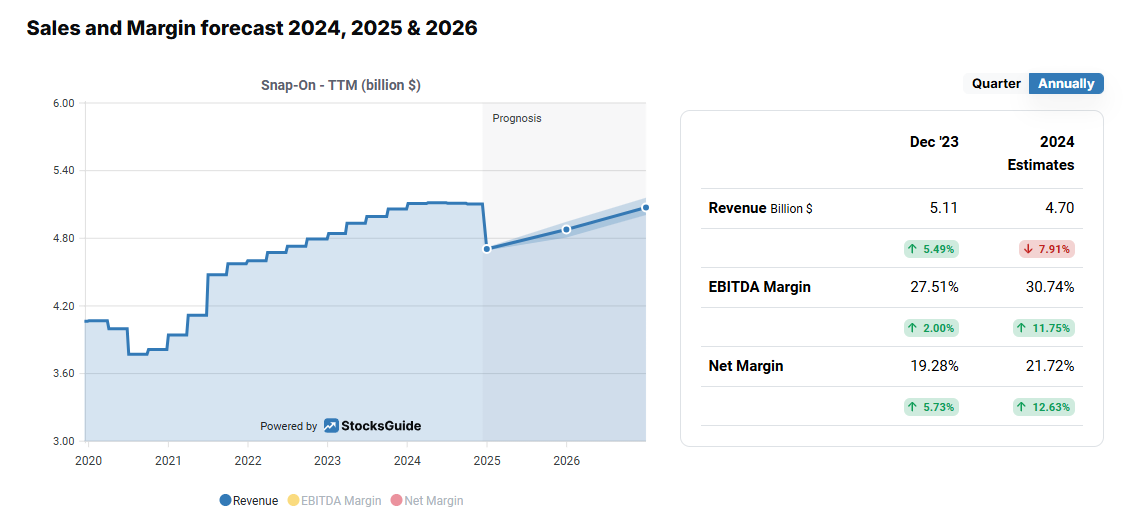

Snap On Forecast 2024

Due to the weak demand in the global automotive business, analysts remain cautious. Sales for the current fiscal year are therefore expected to decline by almost 8 percent to $4.7 billion.

Source: Snap-On forecast 2024

On the other hand, margins are expected to increase further. The EBITDA margin (EBIT plus depreciation and amortization) is expected to be almost 31 percent and the net margin almost 22 percent.

According to the recently reported quarterly figures, this average forecast by analysts does not appear out of the question, as the American company's management has already been able to impress with good cost management.

Source: Snap-On Sales Forecast 2024-2026

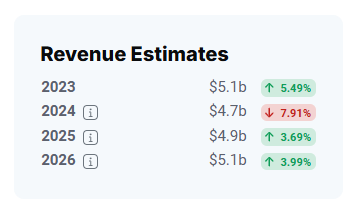

According to analysts' forecasts, sales growth should remain in the low single digits over the next few years. An increase of only 3 to 4 percent is expected for both 2025 and 2026.

Source: Snap-On Sales Forecast 2024-2026

After the significant increase in net profit this year, the increases in the next few years could be lower. For the next two years, net profit is expected to increase only in line with sales.

With an expected net margin of 21.72 percent for this year, there is not much room for further improvement. For this reason, analysts do not expect any major increases here in the coming years.

Key metrics for the Snap On stock from the dividend analysis

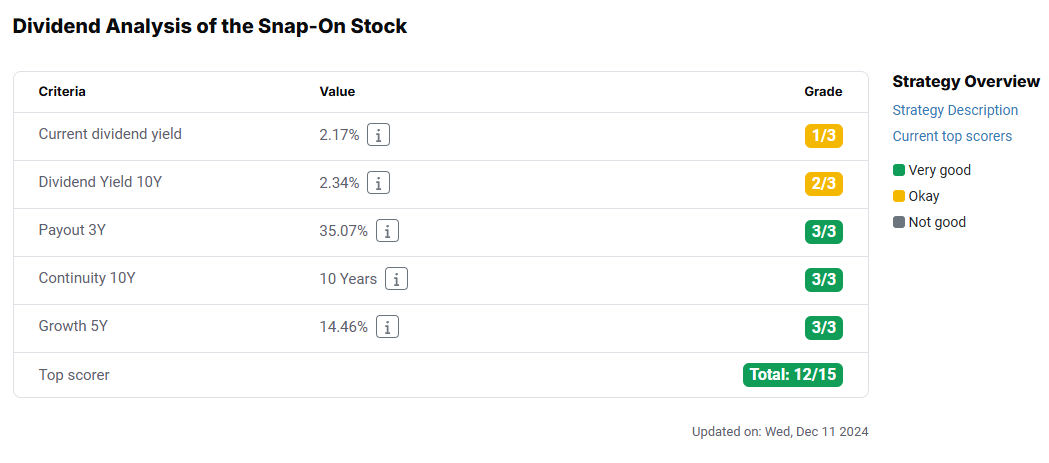

The Snap-On stock is currently the top scorer with 12 points according to the dividend strategy. We have already seen that Snap-On knows how to impress with very good margins.

Source: Snap-On stock dividend

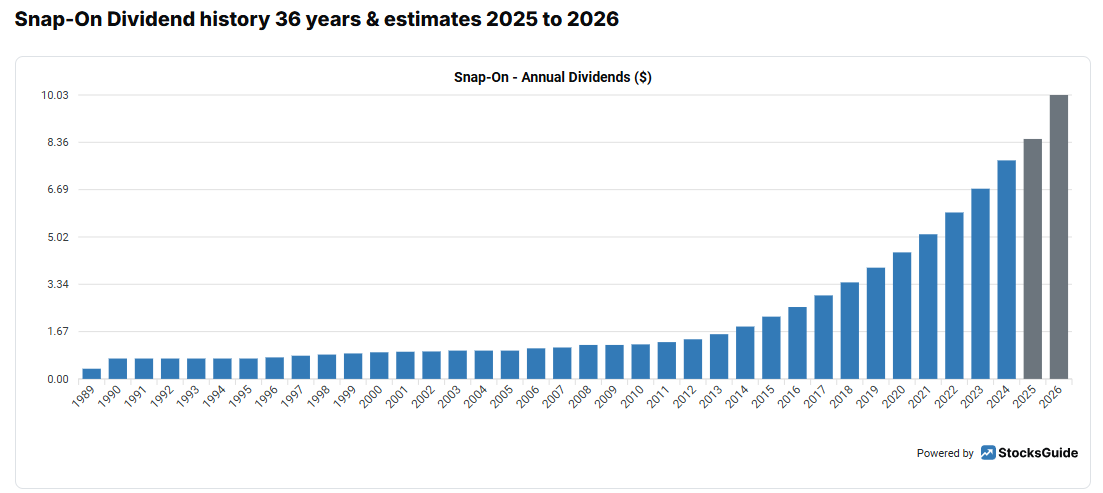

For this reason, part of the annual profit has been used for profit distributions for many years. The dividend has not been cut in the last 25 years. It was kept constant during the years of the dot-com bubble and the financial crisis.

The growth in dividends has been particularly dynamic in the years since the financial crisis. The annual increase is over 13 percent. However, the current dividend yield is only 2.16 percent. With continued high annual increases, the dividend yield could be significantly higher in just a few years.

Source: Snap-On stock dividend

The average dividend yield over the last 10 years was only around 2.34 percent. On the other hand, the low payout ratio of 35 percent is convincing. This also allows for dividend growth if Snap-On's management were to suffer a decline in its annual profit. It also allows for further buybacks of outstanding shares to further increase shareholder value.

The dividend history goes back more than 30 years, so the hurdle of 10 years of continuity can easily be overcome according to the dividend strategy. The stock receives 3 points for this, as well as for the low payout ratio.

Dividend growth over the last five years is actually around 14.5 percent, for which the stock receives an additional three points. Together with the current dividend yield and the average dividend yield over the last ten years, the Snap-On stock scores 12 points in the dividend strategy, which is the minimum required for the stock to be among the top scorers.

Investors can also be reassured at present with regard to the free cash flow (FCF).

Source: Snap-On dividend and free cash flow TTM

Although the increase in FCF is below the increase in the dividend, the free cash flow comfortably covers the profit distribution. Here, the payout ratio is also around 35 percent.

The Snap-On dividend currently appears secure. The low payout ratio still allows for an increase even if cash flows decline. In addition, the Snap-On management knows how to convince its shareholders with high dividend increases.

Valuation of Snap-On stock

We now look at the valuation ratio of Snap-On stock.

Source: Snap-On Stock Valuation Ratio

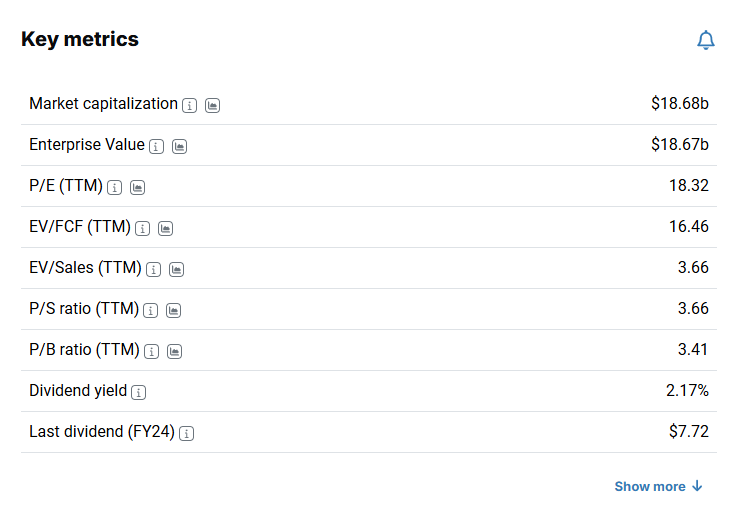

First of all, a solid capital structure is evident, as the enterprise value is on a par with the market capitalization, which in turn means that Snap-On's balance sheet shows low debt.

The current P/E ratio is 18, which means that the stock does not appear to be favorably valued. The enterprise value/free cash flow (EV/FCF) ratio of 16.5 looks a little better.

Both values are above the average values of recent years. The average P/E ratio is 14 and the average EV/FCF ratio is 15.

Taking into account the current economic situation in the automotive sector, the Snap-On share appears to be fairly valued at best.

Therefore, let's add a comparison with Snap-On's competitors.

Snap-On compared to Makita and Stanley Black & Decker

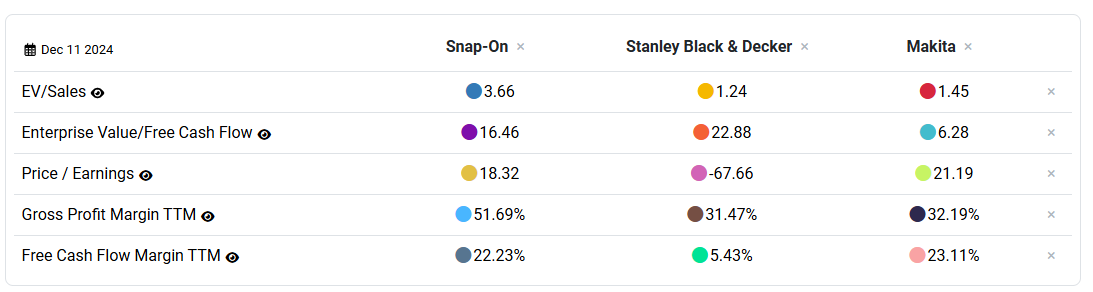

Snap-On's competitors are the also American manufacturer Stanley Black & Decker (SWK) and the Japanese toolmaker Makita.

Source: Snap-On Peergroup Comparison

Based on the P/E ratio, Snap-On is valued lower than its competitors. Makita has a value of 21. Stanley Black & Decker has a negative P/E ratio of 68. Snap-On's EV/Sales of around 3.7 is more than twice as high as that of its competitors.

Makita's EV/FCF ratio appears very low at just 6. By contrast, the factor is 23 for SWK and 16 for Snap-On. Makita also has the highest free cash flow margin at 23 percent.

Even after a brief comparison with its competitors, the Snap-On share does not appear to be a compelling buy.

Conclusion on the Snap-On stock

We come to the conclusion of the Snap-On stock analysis. The company impresses with very good margins and steady growth in its cash flow. However, the company's development is dependent on the general economic situation in the automotive sector, so investors cannot expect significant increases in sales or profits in the near future.

In addition, the valuation range currently appears high, with a price-earnings ratio of 18.

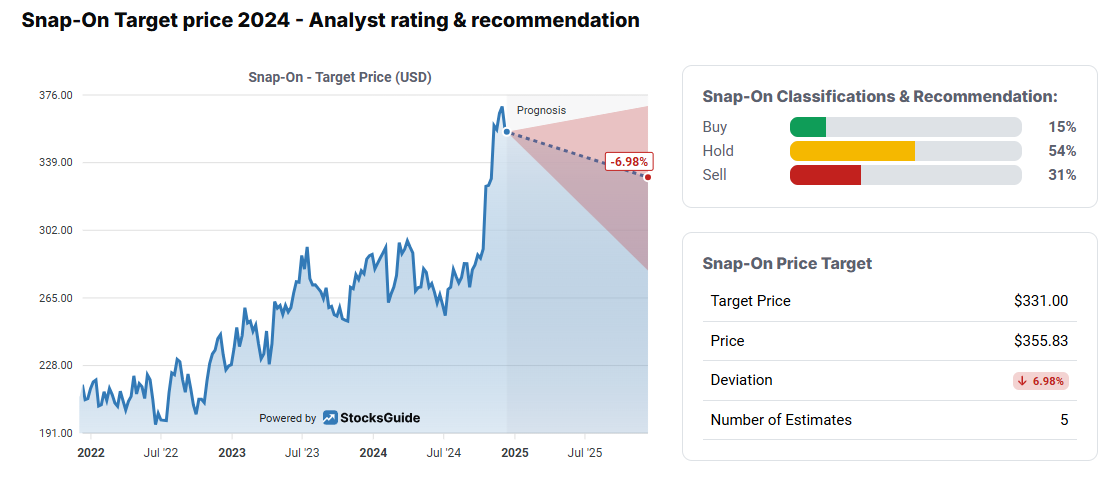

Source: Snap-On Price targets from analysts

Analysts take a similar view and therefore mostly rate the stock as a hold. Around half of the experts currently come to this conclusion. Therefore, the Snap-On share could not be a buy for the moment. By contrast, investors who are already invested should continue to enjoy steady dividend growth in the future. For interested investors, setting up a PE ratio alarm at a value of 15 could be helpful to review the stock again.

If you would like to receive new investment ideas and free stock analyses selected according to the Levermann, High-Growth Investing or Dividend Strategy by email every week, you can now subscribe to our free StocksGuide newsletter.

The author and/or persons or companies associated with the StocksGuide own or may own shares in Snap-On. This article represents an expression of opinion and not investment advice. Please note the legal information.