Table of Contents

-

Company profile - leading producer and marketer of food products, particularly meat, in the US

-

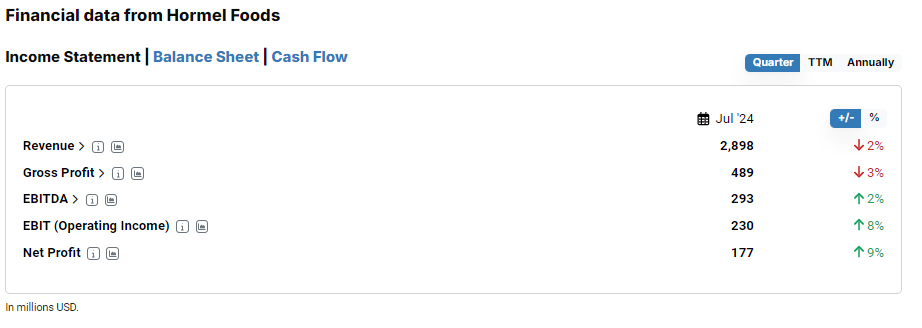

The latest quarterly figures for Hormel Foods from July 2024

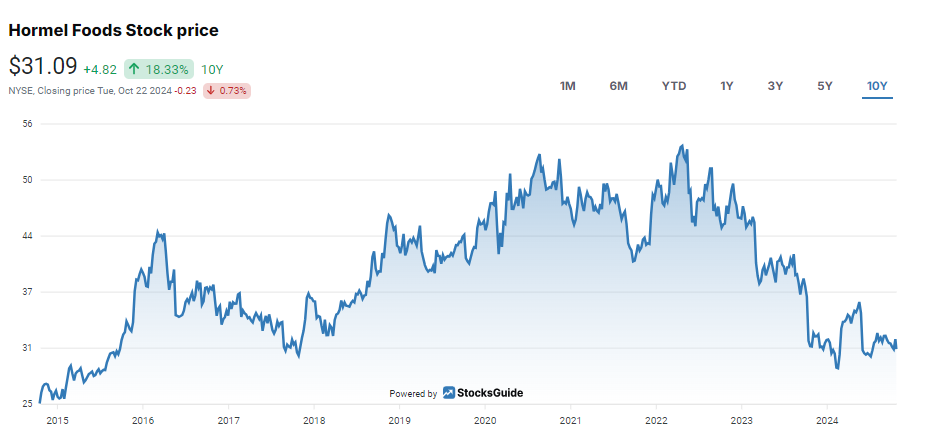

Defensive stocks offer investors many advantages: a predictable business, low volatility and mostly stable cash flows with solid pricing power. Hormel Foods (ISIN: US4404521001) falls into this category and could be attractive to investors as it is considered one of the major players in the production and distribution of food in the United States.

With an attractive dividend yield of over three percent and a 58-year history of uninterrupted dividend increases, Hormel is particularly appealing to dividend-oriented investors. In addition, the share price has consolidated strongly after a long period of appreciation, with new all-time highs in 2022. The stock is down more than 40%. An opportunity?

Source: Hormel Foods Stock Price

Perhaps! But the business is also weak in terms of margins and, above all, growth, which means that dynamic growth opportunities are limited. Despite the strong brands and a clean dividend history, the forward P/E of 22 does not look particularly cheap given the recent moderate growth. Nevertheless, the stock could be an interesting choice for long-term defensive investors due to its stability, dividend yield and presence in key food markets. Let's take a closer look at the universe of the largest publicly traded US canned meat producer in the following Hormel Foods stock analysis.

The most important information in brief

- Hormel Foods is a major player in the production and distribution of food products in the US, particularly meat products.

- The business is considered stable and predictable, but also weak in terms of margins and growth.

- An expected P/E ratio of 22 is not favourable given recent growth.

Company profile - leading producer and marketer of food products, particularly meat, in the US

Hormel Foods' business model revolves around the production, marketing and distribution of food products, with a particular focus on shelf-stable and processed meat products. The company offers a wide range of foods, from protein-based products such as canned meats and sausages to plant-based alternatives. With well-known brands such as SPAM, Skippy and Planters, Hormel caters to a wide range of consumers, from the price-conscious to those who value organic and natural products. Hormel products are sold through a variety of channels, including supermarkets, restaurants and online platforms. The company also operates in the US and internationally.

Source: Hormel Foods 2023 Annual Report

Hormel Foods divides its business into three main segments: Retail, Foodservice and International. Each segment serves different markets and customer needs, presenting different challenges and opportunities.

The Retail segment sells Hormel products directly to consumers through supermarkets and retail outlets. Well-known brands such as SPAM, Skippy and Planters are key drivers. The retail segment is the largest and most important to Hormel.

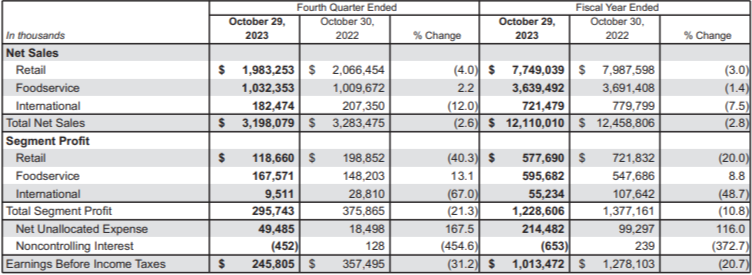

However, retailers are under pressure from changing consumer habits. Customers are also feeling the effects of inflation and are increasingly looking for cheaper alternatives. This is reflected in the figures: in the retail segment, which accounts for the majority of sales (64 per cent), sales fell by 3 per cent to about $7.8 billion. The decline in segment profit was even more pronounced. It fell 40 percent in the fourth quarter and 20 percent for the full year.

The Food Service segment serves restaurants, hotels, cafeterias and other food service establishments. Hormel Foods sells primarily high-protein products such as meat and sausage, which are processed in large quantities. The segment was stable last year. It contributed around 30 percent of total sales in the last financial year and was slightly down at 1.4 percent in 2023. It is interesting to note that profits in this segment increased significantly, by 8.8% for the year as a whole.

The International segment covers the global activities of Hormel Foods. This segment exports Hormel products to markets outside the US, where demand is strongly influenced by regional factors such as currency fluctuations or import regulations. Hormel sees long-term growth potential in Asia and Latin America, although the segment is currently being held back by global uncertainties such as rising costs and fluctuating demand. One advantage is the high quality of US products compared to domestic products, which are high by Asian standards. The international segment represents the smallest sales base. It accounts for just under 6% of total sales. Revenues in this segment also fell sharply, with total revenues in the international segment down 7.5 percent in 2023. Segment profit fell by almost 49 per cent during the year.

Overall, Hormel's three segments are experiencing different trends: retail is struggling with changing demand, foodservice is benefiting from the recovery of the restaurant sector and long-term megatrends, and the international business is facing challenges as well as opportunities in growth markets.

Notwithstanding the opportunities and risks, Hormel Foods' FY2023 was generally weak due to lower sales volumes in key retail and international segments and lower prices for some commodities, such as bacon, despite price adjustments to manage inflation. In particular, reduced availability of pork and turkey affected supply and led to lower sales. In addition, profits fell sharply as an unfavourable arbitration decision resulted in additional costs on top of the declining segment profit.

Hormel Foods' risks and competition

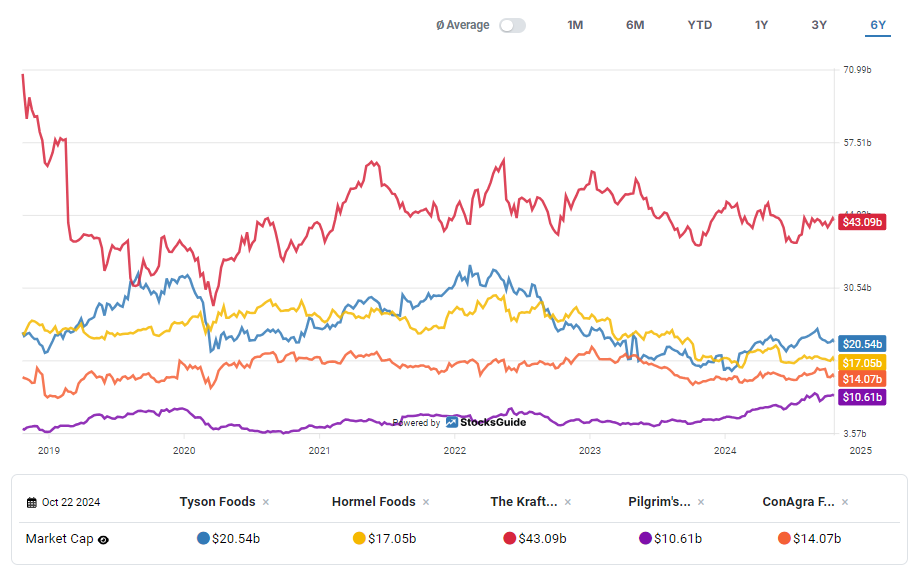

Hormel Foods faces intense competition, particularly from large companies such as Tyson Foods, JBS and Smithfield Foods. These companies offer similar products and have strong positions in both the retail and foodservice sectors.

Tyson Foods, for example, is one of the world's largest meat producers, with a wide range of chicken, pork and beef products. Its similarly large market share and international reach make Tyson one of its closest competitors. Tyson Foods is also investing heavily in plant-based alternatives and sustainable production methods, posing a challenge to Hormel as these segments become increasingly important. JBS, on the other hand, is a Brazilian meat processing giant. Its competition is mainly global. It also operates in the US through its listed subsidiary Pilgrim's Pride. With its huge production capacity and international distribution network, JBS can often operate more efficiently and at lower prices. This puts pressure on Hormel to differentiate its brands and products, which can be difficult in a highly competitive market.

Smithfield Foods, part of China's WH Group, is a particularly strong competitor in the pork market. Through their parent company, they have a clear advantage in accessing the Chinese market, which is an important growth region for Hormel. However, access to Asia is also crucial for investors as these markets offer great potential.

A major risk for Hormel is that competitors such as Tyson and JBS can offer lower prices due to their size and efficiency. As a result, Hormel must either cut costs or focus more on the value of its branded products, which is difficult in a price-sensitive market. Another risk is that consumer preferences may change in favour of plant-based and sustainably produced foods. Although Hormel has already invested in these areas, competition remains fierce in this growing market segment.

In addition, Hormel is vulnerable to fluctuations in raw material prices and supply chain issues. Prices for meat and other commodities can fluctuate significantly due to external factors such as weather, disease or geopolitical tensions, adding uncertainty to production costs.

In international markets, particularly in Asia and Latin America, Hormel also faces high barriers to entry and strong competition from local suppliers. These regional competitors can often offer lower-cost and culturally adapted products, which tends to limit Hormel's growth potential. Smithfield has a particular advantage in the important Chinese market due to its close ties with China, making it difficult for Hormel to gain a foothold there. But Hormel is also under pressure to remain technologically innovative. In particular, its major competitors are investing heavily in sustainable production processes and new technologies that increase their efficiency. If Hormel does not keep pace in these areas, it could lose market share in the long run, especially among consumers who value greener and healthier products.

Source: Peer comparison Hormel Foods, StocksGuide Charts

On the stock market, however, Hormel Foods competes with other large food and meat producers that are also listed and seeking investor interest. In addition to Tyson Foods and Pilgrim's Pride, its biggest competitors in similar businesses include Conagra Brands and Kraft Heinz.

The latest quarterly figures for Hormel Foods from July 2024

In the third quarter of 2024, Hormel Foods posted a slight decline in net sales of minus 2 per cent to US$2.9 billion. However, operating income increased by 8 per cent to $230 million.

Source: Hormel Foods Quarterly Results Q3-2024

Jim Snee, CEO of Hormel Foods, was upbeat about the results, noting that many of Hormel Foods' key retail brands grew and exceeded expectations. The foodservice business grew ahead of the market and the international segment rebounded strongly, driven by global brands. He also stressed that the company remains focused on its strategic priorities and expects continued growth in retail, foodservice and international in the fourth quarter.

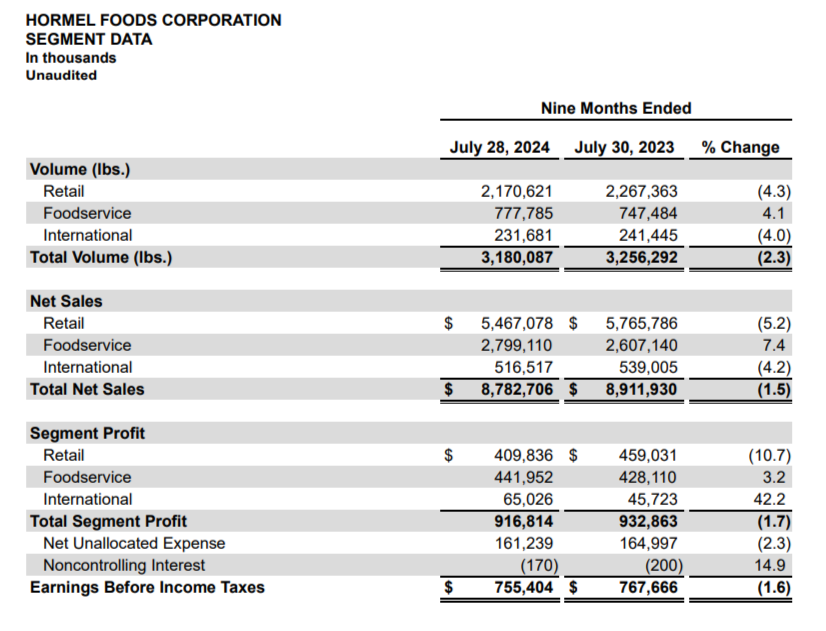

Hormel 9 Months 20/24

Source: Hormel Foods 9-month 2024 press release

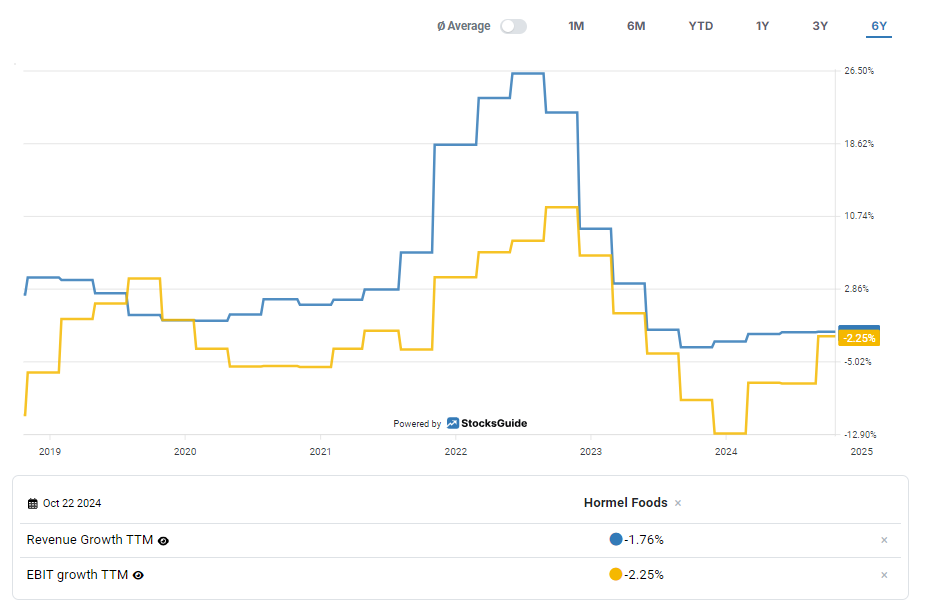

Growth is quite variable. Over the last six years, sales have ranged from -4% to +26%. EBIT has ranged from -13% to +12% over the same period.

Source: Hormel Foods share growth rates

In 2022, however, growth was mainly driven by strong price adjustments made by the company to mitigate the significant inflationary impact on raw materials and operating costs - an exceptional effect. These price increases resulted in significant sales growth, despite volume declines in some segments, such as retail. In addition, Hormel benefited from robust demand in the foodservice sector as more restaurants and hotels reopened following the pandemic. The recovery of international business, particularly in key markets such as Asia, also contributed to growth.

Hormel Foods stock guidance 2024

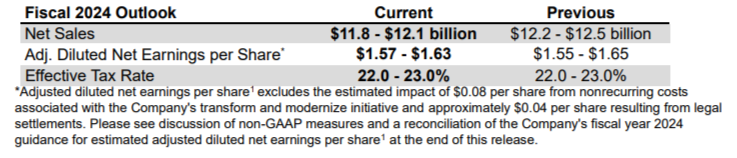

Hormel Foods updated its guidance for the full year 2024. For example, net sales expectations have been narrowed to a range of $11.8 billion to $12.1 billion. Compared to 2023, this represents zero growth at best. The revision ultimately reflects weaker-than-expected commodity markets, production disruptions at the Suffolk, Virginia plant and declines in contract manufacturing.

Source: Hormel Foods Q3-2024 Quarterly Statement

In addition, the adjusted earnings per share estimate was narrowed to a range of $1.57 to $1.63. An additional charge of $0.06 per share is expected from the Suffolk production interruption. In addition, the financial impact of storm damage at the Papillion, Nebraska facility is being assessed. However, Hormel expects its transformation and modernisation initiatives to continue to have a positive impact on net income. The expected effective tax rate remains unchanged at 22-23%. Compared to the prior year, when non-GAAP EPS was $1.61, a range of -2.5 to +1.2 percent should be possible.

Hormel Foods Stock Key Metrics from the Dividend Analysis

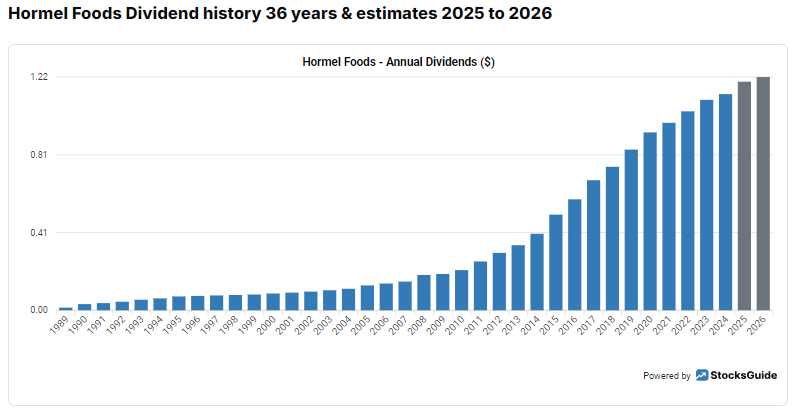

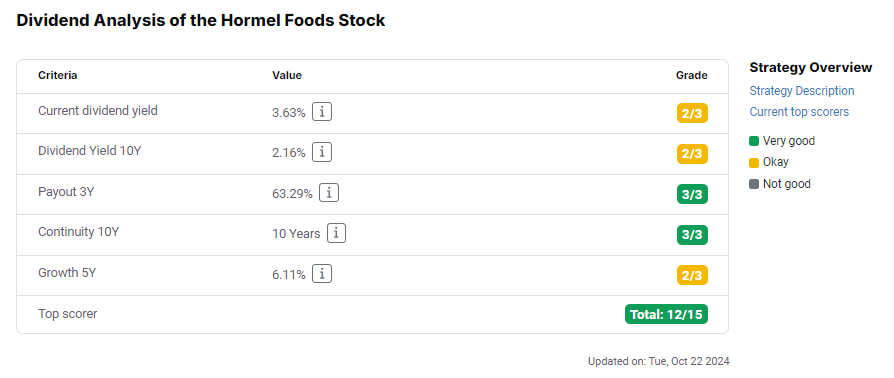

Hormel Foods is a true dividend aristocrat with 58 consecutive dividend increases. In addition, the company has paid a dividend every year for the past 96 years. Investors have great confidence in the company. However, the weak sales and earnings trends should not be overlooked. Given the current level of debt, chronic earnings weakness could quickly lead to a break in the streak.

Source: Hormel Foods dividend history since 2000

However, Hormel Foods scores well in many areas of dividend analysis. For example, the current dividend yield of 3.6% is competitive with peers. Over the past ten years, the average dividend yield has been only 2.2%. This is mainly due to a lower stock price.

Source: Hormel Foods Dividend Score

The three-year payout ratio, i.e. the payout ratio of the last three years, is at a solid level of 63%. The company is returning a healthy portion of its profits to shareholders, while still retaining sufficient funds for investment and growth. For this reason, the Dividend Analysis awarded the company the full score of three points. The same number of points was also awarded for dividend continuity. The dividend has been increased for 58 years without exception. A dividend has always been paid since the IPO in 1928. In contrast, only two points were awarded for dividend growth itself. At 6.1% over the past five years, it was solid, but not above average.

Overall, Hormel Foods scored twelve out of a possible 15 points in the dividend analysis, demonstrating the strength and reliability of its dividend policy.

How safe is Hormel Foods' dividend?

Hormel Foods' dividend appears to be relatively safe in the Dividend Analysis. In particular, the moderate payout ratio of less than 70% provides some cushion in the event of a significant earnings decline. It is also covered by strong cash flows.

Source: Hormel Foods financial data

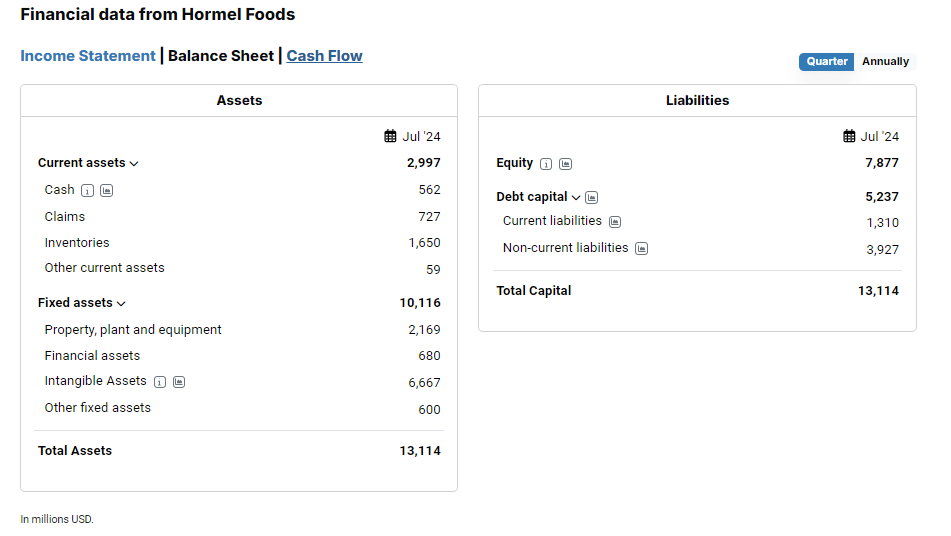

However, the company is burdened by a high level of debt. Long-term debt alone amounted to $2.9 billion in the last quarter. This was offset by cash and short-term investments of $538m. With an annual EBITDA of around $1.3 to $1.5 billion, this is perfectly acceptable. The relatively high equity ratio of almost 60% also speaks for itself. Less threatening is the equally high level of goodwill, which accounts for 73% of intangible assets and around 38% of total assets.

Valuation of the Hormel Foods stock

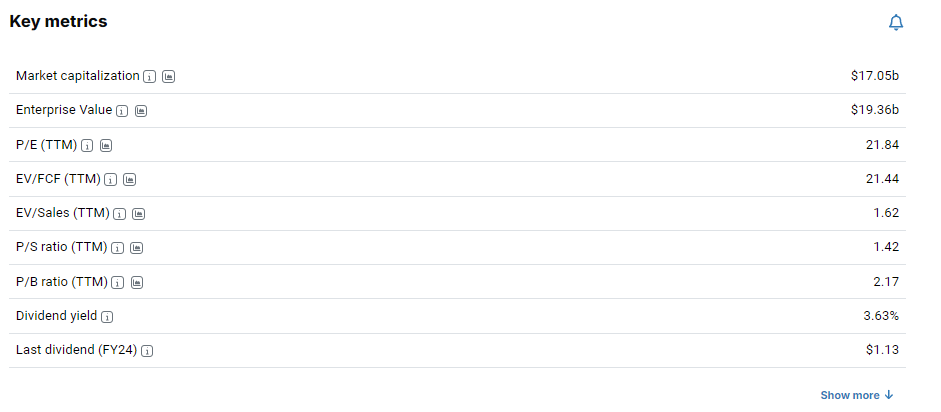

Based on current metrics, the valuation of Hormel Foods appears relatively fair, although not particularly cheap. The price-to-earnings (P/E) ratio of around 22x is still at the upper end of the food sector. Investors are therefore willing to pay a higher price for the company's stable business model and very solid dividend history. However, the P/E could also be too high given that sales growth has recently slowed and Hormel is operating in an environment of uncertainty and inflationary pressure. Competitive pressure is high and margins do not leave much room for manoeuvre. In 2023, the net profit margin is 6.5%, which is in line with the historical average.

Source: Valuations of Hormel Foods stock

The dividend yield of 3.6% is quite attractive, especially for long-term investors who rely on consistent payouts. The food company has a solid dividend history and pays or raises it reliably, which adds to confidence in the stability of its cash flow. The price-to-book (P/B) ratio of 2.2 is also not overly high, which makes Hormel look reasonably valued in terms of its substance.

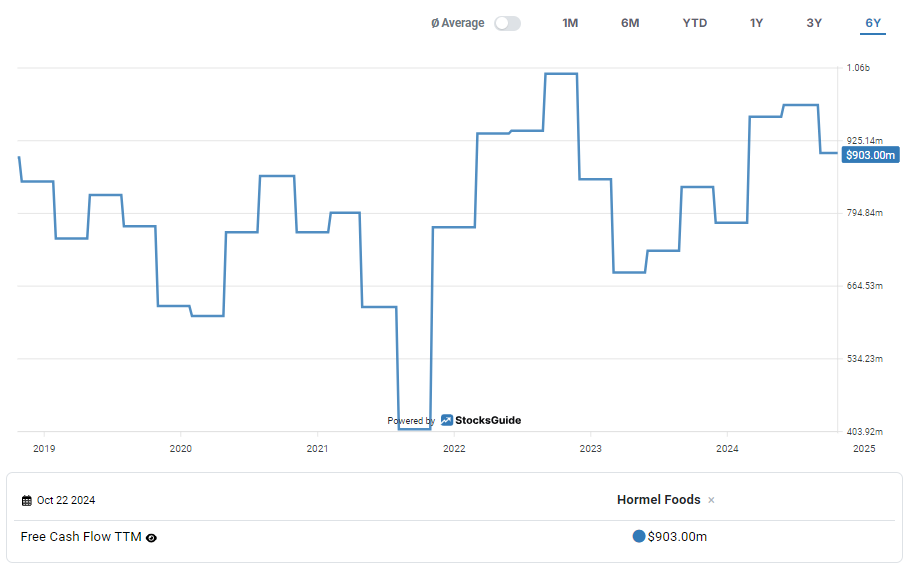

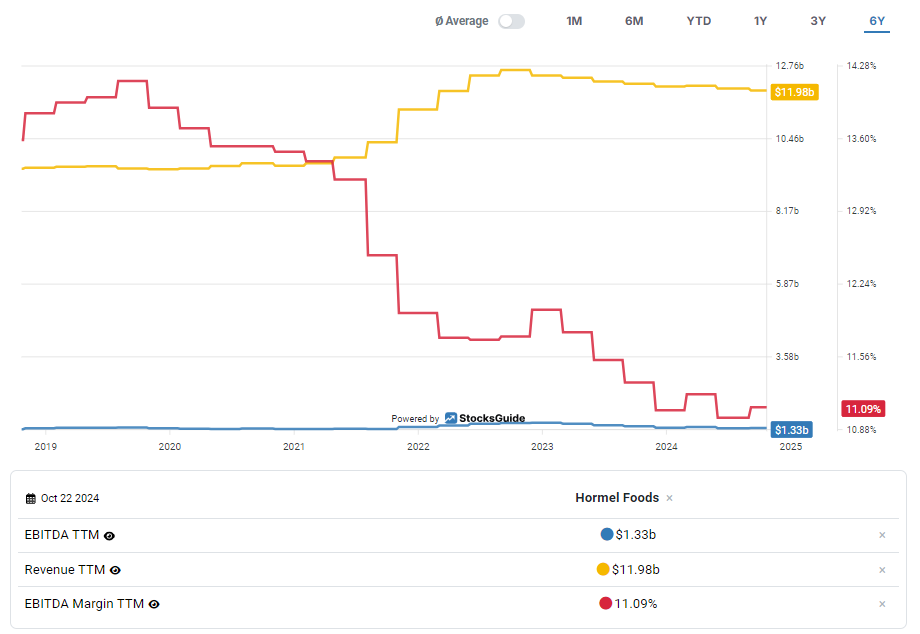

What strikes me, however, is that sales growth is slightly negative and free cash flow is also under pressure, although it is still high at USD 902 million over the last twelve months.

Source: Hormel Foods Free Cash Flow Trend

Source: Hormel Foods sales, EBITDA and margin trends

This shows that it is currently difficult for Hormel Foods to grow organically in a challenging market environment. The EBITDA margin is also deteriorating significantly.

Conclusion on the Hormel Foods stock

Overall, Hormel Foods' stock offers a mix of stability and reliability, particularly for dividend-oriented investors who value consistent payouts. However, the current dividend status is by no means set in stone. Dividend cuts or suspensions are possible at any time. In this context, particular attention should be paid to the earnings situation. And here it is particularly noticeable that the EBITDA margin has lost percentage points. To be fair, the company tended to benefit from soft commodity inflation in 2021/2022 and these effects are slowly disappearing from Hormel Foods' figures. Nevertheless, Hormel Foods seems to suffer from chronic growth weakness. Sales growth over a ten-year period is only in the low single digits. The picture is similar for profits. There is little that can be done without acquisitions, and these are limited by the company's high level of debt.

The company benefits from its established market position in the food industry and impresses with its crisis-resistant orientation. However, with an expected P/E ratio of 22, the stock currently looks rather expensive, especially given its moderate growth. A premium is therefore being paid for the company's good market positioning. It could be affordable for investors looking for long-term security and stable dividends. However, it would be less attractive for growth-oriented investors.

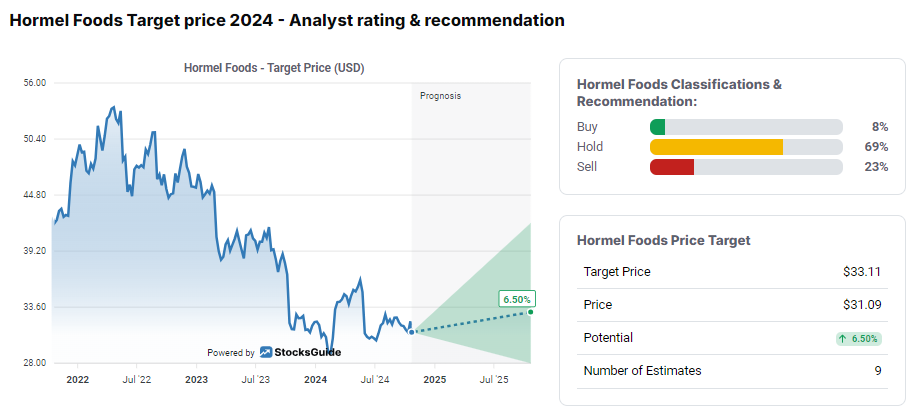

Source: Analysts' views on Hormel Foods stock

The majority of analysts rate the stock as "hold". With a target price of $33.75, the upside is only 8.4%. This reinforces the impression that the current price is too high for the stock to deliver good returns in the future.

If you would like to receive new investment ideas and free stock analyses selected according to the Levermann, High-Growth Investing or Dividend Strategy by email every week, you can now subscribe to our free StocksGuide newsletter.

The author and/or persons or companies associated with the StocksGuide own or may own shares in Hormel Foods. This article represents an expression of opinion and not investment advice. Please note the legal information.