Table of Contents

-

Company profile – leading hardware producer of computers, notebooks, desktops and printers

-

Important key metrics for HP stock from the dividend analysis

The technology sector offers investors numerous opportunities. And although most technology stocks are highly valued, old-tech companies like HP (ISIN: US40434L1052) stand out with a P/E ratio of 10 and solid growth potential. As one of the world's leading providers of computers and printing solutions, HP operates in a dynamic market characterized by technological innovation, intense competition and geopolitical challenges. The size of the California-based company makes it a potential winner in the consolidation that is taking place in the industry. But the increasing demand for home office solutions and the need for efficient business solutions also provide food for thought. The technology conflict between the US and China is no less interesting. It could boost demand for products from domestic providers.

Source: HP stock price performance over ten years; StocksGuide

Meanwhile, the share price is developing solidly in this environment. An increase of 85 percent in the last ten years speaks for itself. Dividends of more than three percent per year on average increase the total return for investors. The distributions have risen continuously in recent years. There have been regular share buybacks on top of this – high free cash flows make both possible. And they could continue to rise, as management predicts.

So there is potential for this value stock from the technology sector. The following HP stock analysis will examine how the opportunities and risks should be weighed up in the end and whether the current valuation could justify an investment.

Company profile – leading hardware producer of computers, notebooks, desktops and printers

Hewlett Packard, as HP is written out, is one of the leading computer manufacturers in the Western world. The business model is geared towards developing and selling technology products and solutions to both end users and companies. The company, based in Palo Alto, focuses on two central business areas: personal systems and printing. Together, they account for the majority of the group's sales.

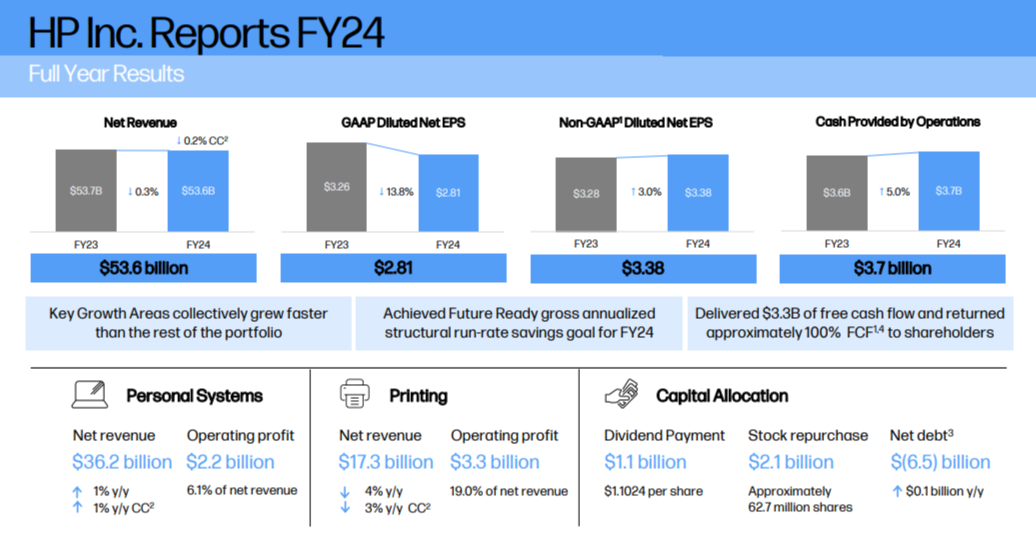

Source: Earnings Summary 2024 of HP

Personal Systems

In the Personal Systems division, HP offers a wide range of computers, notebooks, desktops and workstations, as well as accessory products and services. The division addresses the growing demand for powerful, portable and networked devices that can be used in both professional and private environments. HP has been able to strengthen its market position through innovative product lines and targeted partnerships, particularly in the context of remote working and digital transformation. In addition to hardware, software also plays an important role in this segment, for example through security solutions and management software for corporate environments. Despite software and services, product sales dominate. In fiscal 2024, the business area generated revenue of $36.6 billion and segment operating profit of $2.2 billion. The corresponding margin was 6.1 percent. Segment revenue represents 68 percent of total revenue. With revenue growth of one percent, only a slight increase was achieved in the full year.

Printing

The Printing division includes the development and distribution of printers, printer supplies such as inks and toner, and services related to managed print services. In particular, the after-sales business with cartridges stands for high margins and reliable cash flows. HP pursues a dual strategy here that aims to combine hardware sales and long-term sales of consumables. Solutions such as Instant Ink, a subscription model for ink supply, create stable sources of income. In addition, the company is increasingly focusing on commercial printing solutions, including 3D printing technologies for industrial applications. Not to be forgotten is the Smart Tank system, which allows customers to purchase refill products at a relatively low cost. The focus here is on efficiency, sustainability and adaptation to digital workflows. The segment generated revenues of $17.3 billion in fiscal year 2024, which represented a 32 percent share of revenues. At $3.3 billion, the operating profit of $1 billion was earned in the segment with computers, notebooks, desktops and workstations. The margin here is attractive at 19 percent, which can be explained by the expensive ink cartridges for the cheap printers sold. However, growth here has recently declined significantly at 4 percent.

Looking at the ratio of products to services at the group level, the product business clearly dominates with a revenue share of 94 percent, compared to the service business with a revenue share of 5.8 percent. HP's business model is therefore very hardware-heavy, strongly influenced by cycles, but also by raw materials and supply chains.

Market & competition

The market for personal systems and printing is anything but simple. It is characterized by intense competition, rapid technological innovation and changing customer needs. The Asians, in particular, are stepping on the gas. In the Western world, on the other hand, there is almost no serious competition from the core business.

In the personal systems segment, developments such as cloud computing, artificial intelligence and increasing mobility requirements are driving demand for powerful, flexible and secure devices. The printer market, on the other hand, is increasingly influenced by the trend towards digitization, which is leading to a decline in traditional print volume, while demand for specialized printing solutions such as 3D printing is on the rise. However, this is still a niche market that has yet to develop into a mass market.

However, growth opportunities also arise from technological change and new business models. For example, the increasing demand for home office solutions and hybrid working models offers great potential for PCs, notebooks and accessories. In the printing sector, further growth lies in innovative solutions such as managed print services, subscription models such as Instant Ink or industrial applications such as 3D printing. Sustainability is also gaining importance as a sales argument.

However, there are also risks. In particular, high price sensitivity and competition from Chinese companies such as Lenovo and Huawei, which offer products at competitive prices, are putting pressure on margins. A strong trend towards consolidation has been observed for years. Supply chain problems, geopolitical tensions and dependence on commodity markets pose further challenges. Another risk is the growing trend towards digitization, which is likely to reduce demand for traditional printing solutions in the long term. In this dynamic environment, HP has to impress with innovation, service orientation and sustainable products. In the past, it has only partially succeeded in doing so.

HP is therefore operating in a highly competitive market in which both global brands and emerging Chinese companies are serious competitors. In the Personal Systems segment, HP primarily competes with established providers such as Dell, Apple and Lenovo. In particular, the Chinese company Lenovo is an extremely serious competitor with fundamental competitive advantages. Lenovo scores with competitive prices, high production capacities and a global supply chain that allows it to react flexibly to market fluctuations. Against this backdrop, the Chinese have pursued a successful international acquisition strategy in recent years. Names like Medion or IBM Thinkpad are now part of the Chinese company's product portfolio. The local Chinese hero Huawei is also continuously expanding its presence in the notebook and tablet market and uses its technological know-how from the telecommunications sector to offer high-quality products. However, Huawei is increasingly being viewed critically by Western governments due to its close ties to the Chinese government.

Source: Revenue development Peer HP; StocksGuide Charts

The competitive situation in the printing sector is different. This market is traditionally dominated by Western and Japanese companies such as Canon, Epson and Xerox. However, Chinese companies are also gaining in importance here. Companies like Xiaomi and smaller providers started offering affordable printers and accessories years ago, which could challenge the established brands for market share. In the consumables segment in particular, there is strong competition from low-priced alternatives from China, which are not only more attractive in terms of price, but are also increasingly competitive in terms of quality. HP's Smart Tank Systems are countering this.

One important aspect of the Chinese competition is their ability to create competitive advantages through government support, low-cost production and rapid innovation cycles. They are increasingly entering international markets with low-cost but technologically advanced products. HP is therefore under particular pressure. It must not only invest in innovation and quality, but also in strategies to retain existing customers – for example, through subscription-based services or sustainable solutions that set it apart from the competition. However, differentiation opportunities are difficult due to the platform independence of the products. When it comes to innovation, the Americans are also lagging behind the competition.

HP has only grown to its current size thanks to numerous acquisitions in the past. For example, more than 175 acquisitions have been made since the mid-1980s. A recent example is the 2022 acquisition of Poly (formerly Plantronics) for $3.3 billion. Poly is a leader in communication and conferencing technology that addresses the hybrid work market. The pandemic has given this area a greater importance and it is likely to offer further potential for the period after the pandemic. Another important acquisition was the purchase of the printer business of Samsung Printing in 2017 for $1.05 billion. The aim of the acquisition was to expand HP's leading position in the printer market and to focus more on A3 printing solutions, which are particularly relevant for business customers. This was a prime example of the ongoing consolidation in the highly competitive printer market. One particularly high-profile attempt in this context was the planned merger with Xerox in 2019. The much smaller company Xerox attempted a hostile takeover at the time, offering HP $33 billion. However, HP rejected the offer on the grounds that a merger was not in the interest of shareholders. The takeover attempt failed, but it underscored HP's attractiveness as a takeover target. However, it is also conceivable that HP will increasingly look for competitors in the future to further consolidate the market. After all, it is considered a consolidation winner due to its size.

But HP has also taken important steps in other areas to better position itself. The acquisition of the HyperX brand in 2021 for $425 million was a prime example of this. HyperX is known for gaming accessories such as headsets, keyboards and mice. In addition, HP has acquired smaller companies in the software and 3D printing sectors in recent years. These include, for example, the British print service provider Apogee, with which HP expanded its services in the managed print segment in 2018.

A major problem remains the pure focus on device-independent volume markets. Even if it were theoretically possible for HP to develop into a second Apple, this is unlikely from today's perspective, as the business models, target groups and brand strategies are fundamentally different. While Apple relies on premium products and a closed ecosystem, HP is more focused on broad markets and open standards. Nevertheless, HP could adapt elements of Apple's recipe for success by investing in design, innovation, services and sustainability in order to better differentiate itself in a highly competitive market.

The situation could be different when it comes to the US-China trade war: the technology conflict between the two major powers offers HP several opportunities, particularly due to the reorganization of global supply chains and the changing competitive situation. Since Chinese technology companies such as Huawei and Lenovo are restricted in Western markets by trade restrictions and sanctions, HP could expand its market share in these regions – at least that is the hope. In addition, government subsidies and investments in the US could create new growth impulses for domestic technology companies, for example through preferential treatment in tenders or tax incentives. Another opportunity lies in the diversification of supply chains. The pressure to disengage from Chinese suppliers could prompt HP to shift production more to countries like India, Vietnam or Mexico. This would ultimately reduce the risk of geopolitical dependencies while strengthening the company's resilience. Finally, geopolitical tensions could also increase demand for secure and trusted technologies, from which HP could benefit by expanding its security solutions and cloud-based services for businesses. So, all in all, there are some arguments in favor of the stock. However, these are not yet really concrete. The strong pressure to consolidate remains in the foreground. Here it is important to find solutions to increase margins and growth.

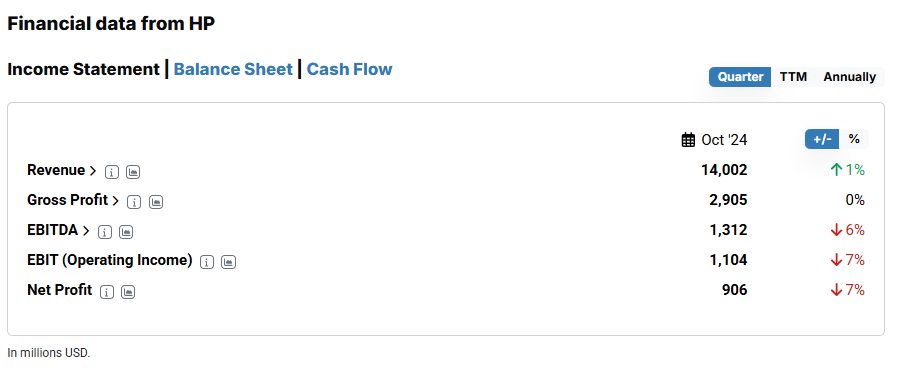

The last HP quarterly figures from October 2024

At the end of November 2024, HP had already published its figures for the fourth quarter and the entire 2024 financial year. And it shows that despite some challenges, the company is still well positioned. Even though revenue was down slightly on an annualized basis, the printer and PC giant continued to grow in key areas such as Personal Systems and Printing Solutions in the fourth quarter, offering a positive outlook for the future.

Source: Financial data Q4/2024 from HP; StocksGuide

However, if we compare these figures with the previous quarter (Q3), we see a slowdown in momentum. The large Personal Systems division grew by 5 percent in the previous quarter. Most recently, it was only up two percent. The smaller but significantly more profitable Printing division recorded a minus of 3 percent in the third quarter, and even a minus of 4 percent in the fourth quarter.

What we can see from the quarterly figures is that the economic environment is not exactly developing in HP's favor. Nor is there any sign of the dynamics of a special AI cycle.

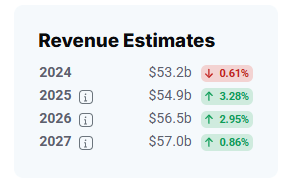

HP stock forecast 2025

The situation is similar for the outlook for the full year 2025. No specific revenue forecast is given here. However, analysts expect slight growth in the low single digits. This direction also applies in the medium term, with sales of $57 billion expected in 2027. Compared to 2024, however, this would only correspond to an overall increase of 7.1 percent.

Source: Sales forecast 2027 HP stock; StocksGuide

Things could move much faster on the earnings side: HP itself expects adjusted EPS of between 3.45 and 3.75 in 2025. Compared to the figure of $3.38 for fiscal 2024, that's still an increase of almost 11 percent, which is already more than analysts expect for revenue growth in the coming years.

For 2025, HP is expected to generate a free cash flow between $3.2 and $3.6 billion. At $3.3 billion, the 2024 figure is at the lower end of this range. However, 100 percent of this figure was returned to shareholders in the form of dividends ($1.1 billion) and share buybacks ($2.1 billion). In the best case, dividends and share buybacks can therefore be expected to rise again in 2025. However, the technology group's high debt should not be overlooked. A net debt of $6.5 billion weighs heavily. However, thanks to strong free cash flows, it is manageable.

Important key metrics for HP stock from the dividend analysis

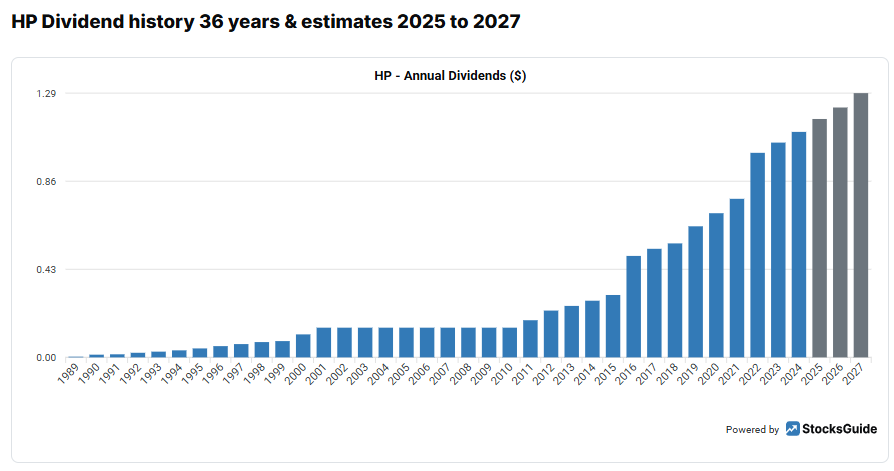

The dividend analysis of HP stock shows an overall positive picture for long-term investors who rely on regular distributions. There have been no cuts in the HP dividend in the last ten years. On the contrary, HP's dividend has increased every year since 2011 – from $0.15 to $1.10 at last count. This continuity shows that HP has been able to maintain its dividend policy even in difficult market phases, which speaks to the reliability of the company. Consequently, the HP share received the full three points in the dividend analysis.

Source: Dividend development of HP stock since 2000; StocksGuide

HP shares also performed well in terms of dividend growth. In the last five years, for example, the HP dividend has increased by an average of 11.5 percent per year, which is a good pace and indicates a progressive dividend policy and positive business development.

Operationally, however, the company has not grown as strongly. In the long term, sales have declined, and earnings growth has remained only slightly positive. Nevertheless, analysts predict a further increase in HP's dividend – by a further 17 percent over the next three years. Is that a good thing?

Measured by the payout ratio, further potential can at least be seen. It was 35 percent for the last three years and shows that HP tends to act responsibly. However, since large amounts regularly flowed into share buybacks, the payout ratio must be assessed separately. Consequently, more distribution can only be financed by growth in free cash flow or a reduction in share buybacks.

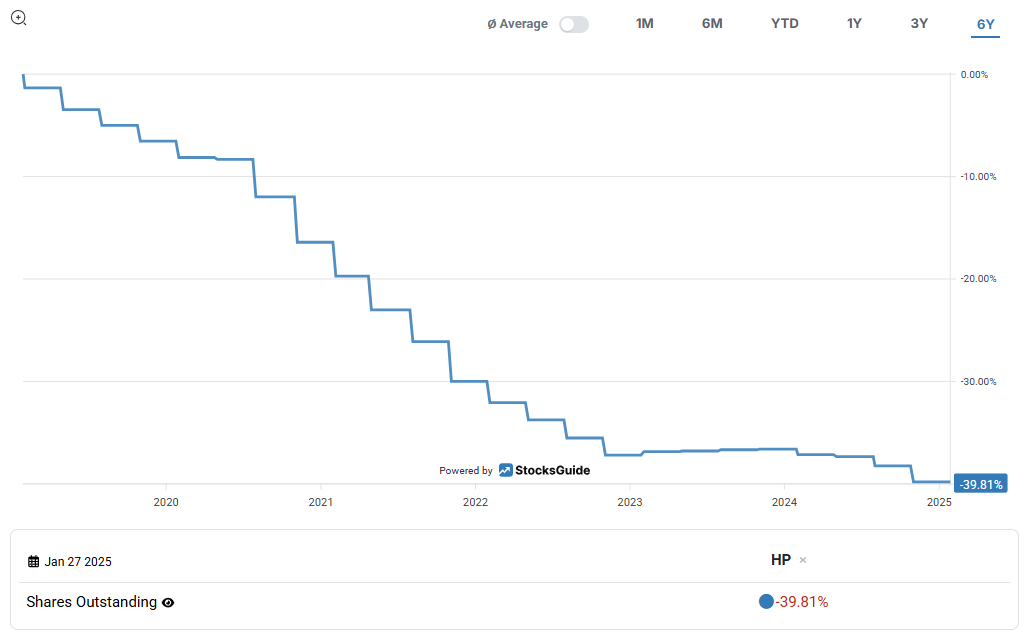

Source: Development of the number of HP shares; StocksGuide

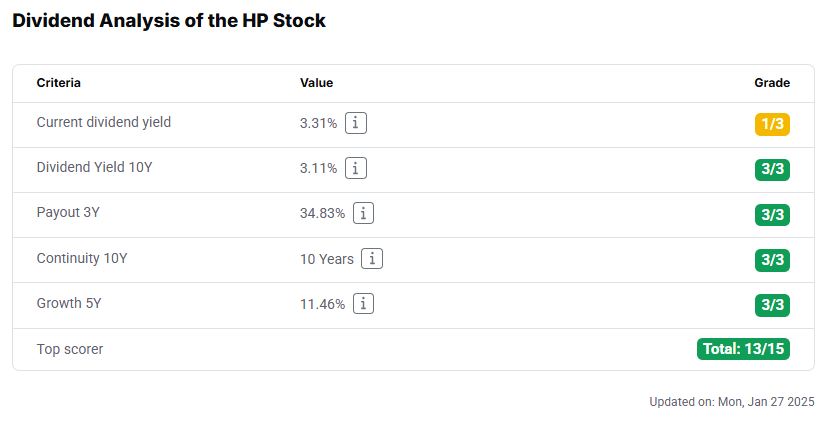

With a current dividend yield of 3.4 percent, the stock still offers a solid entry yield, even if it is considered average compared to other high-dividend companies. In this regard, the HP share receives 1 out of 3 possible points. However, in view of the historical dividend yield of 3.1 percent over the last ten years, one currently receives a little more than in the past, which could indicate a more attractive valuation. But more on this in the next chapter.

Source: Dividend analysis HP stock; StocksGuide

Overall, the HP stock achieves 13 out of a possible 15 points and is therefore one of the top scorers in the dividend strategy. The company offers a good mix of attractive returns, continuity and dividend growth. For investors who value stability and dividend growth, the HP share could therefore potentially be an interesting choice. However, the historically weak growth of the technology stock remains the main problem. The low software and service revenues do not exactly speak in favor of HP shares either. All this is also reflected in the valuation of the stock.

Valuation of HP stock

The valuation of HP stock initially suggests that the company is currently valued very moderately and could offer potential for investors with a long-term orientation – especially for value investors. With an expected price-to-earnings ratio (P/E) of less than 10, the share price is well below the average for many technology companies. However, there are reasons why the market is cautious about HP – possibly due to the challenges in the traditional PC and printer market. The traditionally weak growth does not exactly speak in favor of the group, nor does the high level of debt.

Source: Valuations of HP stock

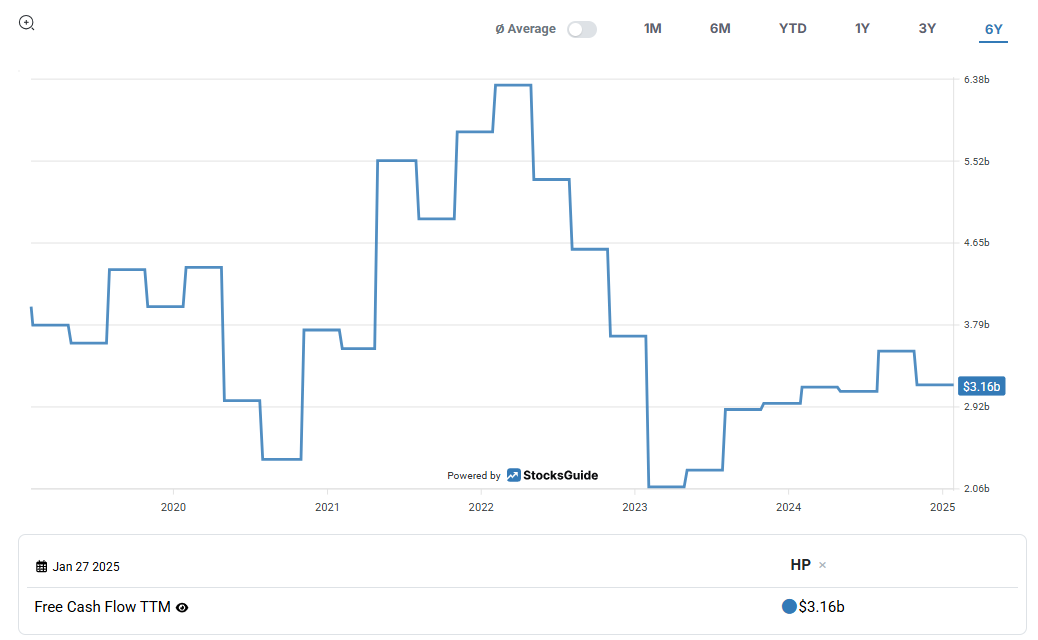

The free cash flows from the core business, on the other hand, are quite reliable, which could make the stock a value pick, especially for investors looking for stability and dividend growth. On average, over the last few years, this has been around 3.8 billion US dollars per year, as the following graphic from the Chart Tool of StocksGuide shows.

Source: Development of HP's free cash flow; StocksGuide

HP's relatively reliable free cash flows result from its high market shares in the stable core segments of PCs and printers. Above all, however, every printer sold has to be supplied with ink cartridges for years.

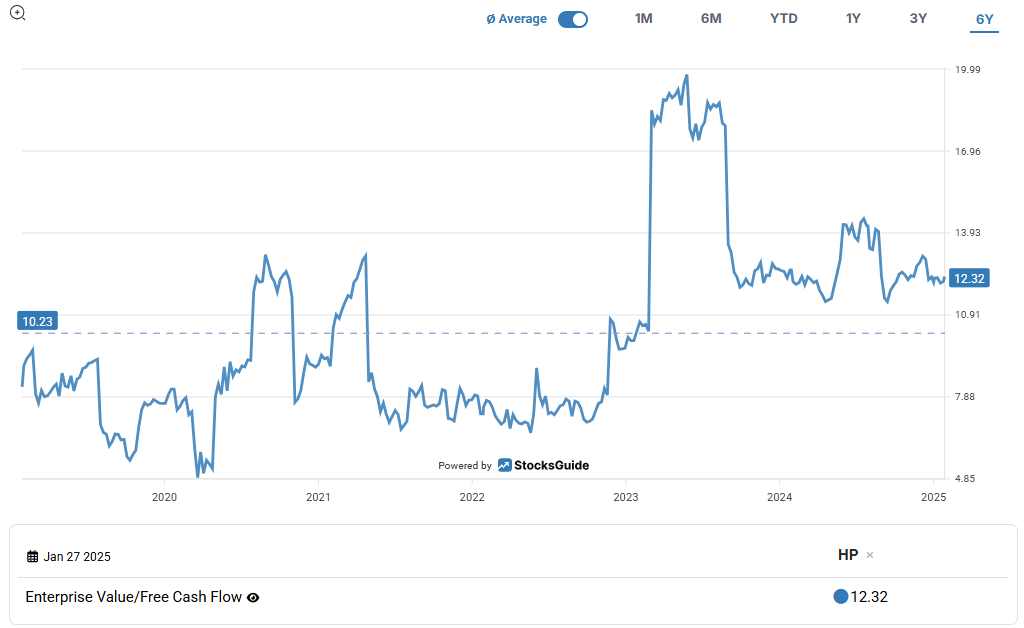

However, the enterprise value to free cash flow (EV/FCF) ratio of 12 shows a different picture. Although the value appears attractive at first glance, it is significantly higher than the P/E ratio due to the debt. At USD 2.78 billion, net income was recently well below the free cash flow. Above all, however, a historical analysis of the EV/FCF ratio shows that the current value is around 20 percent above the average value of the last six years.

Source: Development EV/Free Cashflow; StocksGuide Charts

In combination with zero growth, this means that there should no longer be any bargains. Specifically, analysts expect revenue growth of just 3.3 percent, which, while solid in a mature market like technology hardware, does not justify higher valuations as for high-growth stocks. In this context, however, the adjusted earnings per share (EPS) growth, which HP estimates at 11 percent by 2025, is all the more impressive. This discrepancy between revenue and earnings growth initially points to an improvement in margins. This should be achieved primarily through cost optimization, a higher share of high-margin products or services, and strategic acquisitions. However, the high share buybacks also contribute significantly to the disproportionate increase in EPS.

For technology companies, however, innovation is an important currency on the capital market. This needs to be converted into growth in order to achieve a higher market capitalization. A high innovation rate usually leads to higher growth in the long term. However, this is precisely the strategy that is missing at HP. A re-evaluation in terms of prospects therefore does not appear justified at present.

Conclusion on HP stock

HP stock is potentially a solid value stock, characterized in particular by stable cash flows and a favorable valuation. With a P/E ratio of 10 and an EV/FCF of 12.3, the stock is currently trading well below the average of many technology companies. This makes it fundamentally attractive for value investors looking for a good balance of risk and return. Even Warren Buffett bought the stock in 2022, probably with the ulterior motive of a good market development for hybrid work models. However, he sold his position again in 2023 and 2024.

The high proportion of product sales from the so-called “Old Technologies” – such as PCs and printers – may initially seem unattractive, especially when compared to a company like Apple. Here, the i-group's service revenues accounted for around one-third of total revenues – and the trend is sharply rising.

Above all, growth is lacking at HP. Sales are just bobbing along. Product sales dominate everything, and growth in the service segment is by no means in double digits. However, HP's high market share and strong position in both large corporate segments is a major advantage. For example, its market share in the PC market was around 22 percent, and in the printer market 35 percent. HP has extremely deep moats, especially in the printer market and in solutions for hybrid working. The Chinese competition is out of reach here. With an adjusted profit growth of 11 percent, the company shows that it is able to operate efficiently and optimize its margins despite moderate sales growth of 3.3 percent. Above all, however, the high share buyback volumes are partly responsible for the disproportionate increase in EPS.

However, the challenges for HP cannot be overlooked. The market is characterized by strong Asian competition and without a far-reaching strategic realignment, the technology company could lack share price potential in the long term. We have already seen something similar at Ebay. Here, too, a lot of money was set aside for shareholder value, but little was spent on technological innovation. This initially boosted the share price, but an extraordinary share price increase was not achieved.

This makes it all the more important to assess the opportunities that could arise from HP's most recent acquisitions. By buying Poly and HyperX, HP has invested in high-growth areas such as communication technology and gaming. These strategic steps could help to drive the company's transformation from a provider of traditional hardware to a provider of modern solutions for work and entertainment. However, I do not see this as a game changer, nor as a strategic shift that could justify a higher valuation.

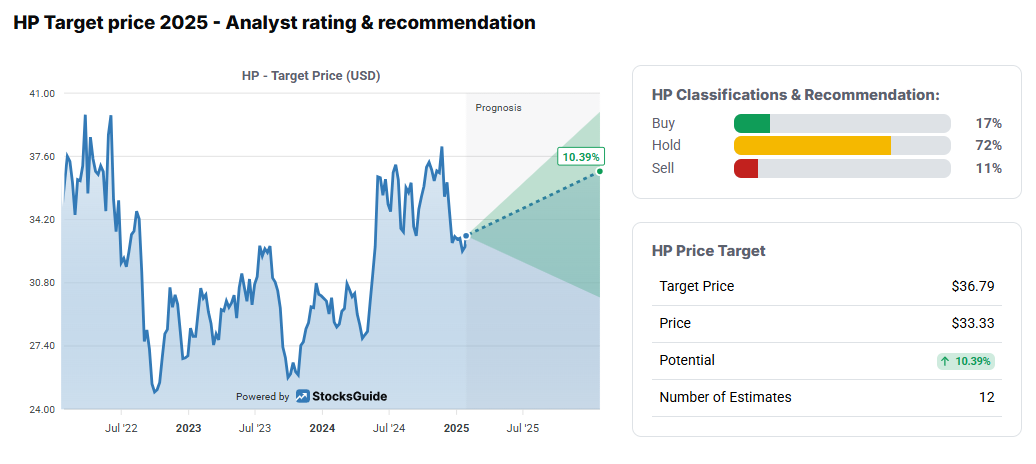

Source: Analysts' opinions on HP stock; StocksGuide

The analysts seem to have a similar view. The vast majority (72 percent) recommend holding the stock. The average price target is $36.79, around 12 percent above the current price. At least 17% of analysts see the stock as a buy, with only 11% taking a sell position. Whether more than a few percentage points can be made on the stock market will likely depend primarily on the company's strategy and long-term growth.

If you would like to receive new investment ideas and free stock analyses selected according to the Levermann, High-Growth Investing or Dividend Strategy by email every week, you can now subscribe to our free StocksGuide newsletter.

The author and/or persons or companies associated with the StocksGuide own or may own shares in HP. This article represents an expression of opinion and not investment advice. Please note the legal information.