Table of Contents

The Target Corporation (ISIN: US87612E1064) is one of the largest discounters in the United States and has established itself as a major player in the retail industry. For 53 years now, the company has been reliably increasing its dividend and thus enjoys the status of the dividend king – stocks with a series of dividend increases of more than 50 years.

With a price-earnings ratio of 16, the retail share is not expensive. The share price has also developed well over the years, as the 146 per cent increase reveals. Together with the annual dividend of around 2.6 per cent, the share has thus been an attractive investment for investors so far.

Source: Target stock price

But does this also apply to the future? Doubts are at least appropriate, because despite this stable base, weaknesses are emerging in growth and in e-commerce. While the company continues to create an attractive shopping experience in its stores and relies heavily on its own brands, Target is struggling to keep pace with its competitors, especially Amazon, in the rapidly growing online retail sector. But even arch-rival Walmart is doing better online than Target. The following Target stock analysis will examine what investors can now expect from the Target share and whether the share is ultimately a buy.

The most important information in brief

- Target is one of the largest discounters in the US

- The dividend king is not objectively expensive with a P/E ratio of 16

- However, weaknesses are emerging in growth and e-commerce

Company profile – leading discount retailer in the USA

Target Corporation's business model is based on a wide range of strategies aimed at providing customers with an attractive shopping experience, high-quality products and competitive prices. It sells clothing, household goods, electronics, food, cosmetics and much more – a bit like an all-rounder like Aldi or Lidl in Germany, except that its focus is more on non-food.

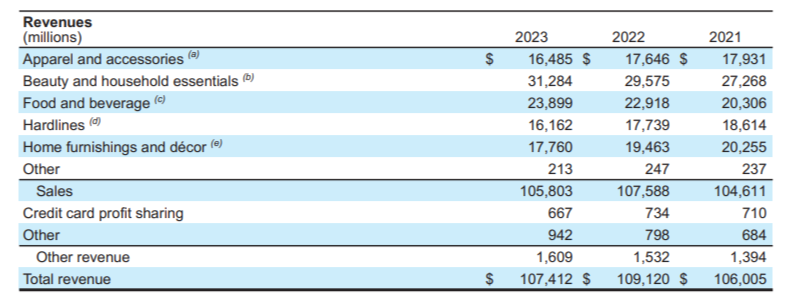

For example, the largest share of sales was achieved with beauty products and household goods. In 2023, the retailer sold goods worth over 31 billion US dollars in this category alone last year, followed by food and beverages with 23.9 billion US dollars. In third place were furniture and decorative items.

Source: Annual Report Target Corporation 2023

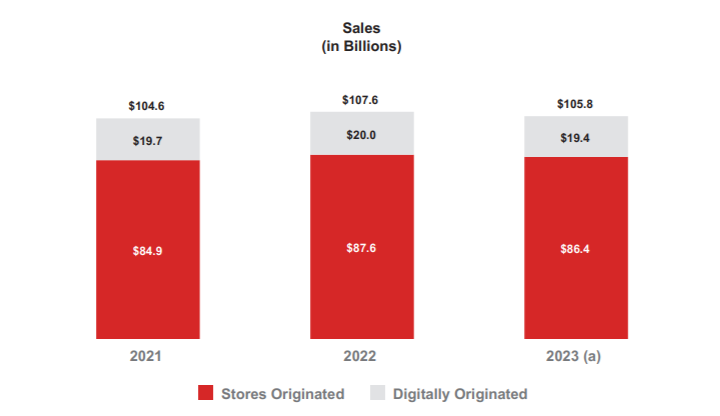

Due to the booming online trade, Target now pursues a hybrid approach that includes both brick-and-mortar retail and digital distribution. Its business is divided into two main segments: stores originated and digitally originated.

The dominance of physical stores is clearly evident, with a share of almost 82 per cent of total sales. Online sales stagnated at around 20 per cent. There has also been no significant increase in total sales in recent years.

Source: Target Corporation 2023 Annual Report

The Stores Originated segment is about sales that originate in Target's physical stores. Customers visit the stores to select and purchase products directly on site. This also includes services such as ‘Drive Up’ and ‘Order Pickup’, where customers order online but pick up the goods at the store. The goal of the segment is to offer customers a seamless shopping experience on site by also using the stores as warehouses and pick-up stations.

The Digitally Originated segment, on the other hand, includes all sales that are made online, regardless of whether the products are then delivered to the customer's home or picked up at a store. Target's e-commerce platform plays a central role here. It offers a wide range of products that can be accessed via the website and app. To make shopping more convenient, digital orders can be sent directly to the customer or delivered via services such as ‘Shipt’.

Overall, Target's approach combines the strengths of brick-and-mortar retailing with the growing demands of online shopping to provide customers with flexible and convenient shopping options. However, weaknesses in growth can be seen.

Competition

Target faces intense competition from a number of companies in the retail sector. Arguably its strongest direct competitor is Walmart, which is known as the market leader in US retail. Walmart pursues a similarly aggressive low-price strategy, but offers an even broader range of products, which appeals to price-conscious customers in particular. By contrast, Target positions itself more in the mid-price segment and relies on a better shopping experience with a modern and appealing store design.

Amazon is also a major competitor, especially in the area of online retailing. Amazon, on the other hand, dominates the e-commerce market, forcing companies like Target to improve their own online presence and develop digital strategies to compete with Amazon's fast delivery times and huge product range. Target has made good progress in this area in recent years, for example by expanding same-day delivery and the option of picking up online purchases at its stores. However, Target's online sales have stagnated, which does not exactly suggest that its digital business is successful. The same applies to its total sales.

In addition, there are specialised retailers such as Costco, Kohl's and Best Buy, which are also exerting pressure in various markets. Costco, for example, appeals to a similar target group, but often offers even lower prices through its membership model and focus on wholesale sales. Kohl's, on the other hand, competes in the fashion and household sectors, while Best Buy is a strong competitor in consumer electronics.

Meanwhile, Target is struggling among the largest retailers. Despite fierce competition, the second-largest brick-and-mortar retailer in the US is still holding its own, although its growth and margins could be better. Target is particularly lacking in momentum in the important online retailing sector, which points to a crucial weakness. But it is also not making a strong enough push to expand abroad. So far, foreign sales do not play a role in its business model.

Source: Sales growth of Target, Walmart, Costco and Best Buy compared

The last Target quarterly figures from June 2024

In the second quarter of 2024, Target delivered solid results reflecting a return to growth and strong earnings momentum. For example, comparable sales rose 2 per cent, which was at the high end of the company's expectations. Particularly noteworthy was the 3 per cent growth in customer traffic, with all six sales categories seeing an increase. Digital sales also rose sharply, up 8.7 per cent, with same-day delivery services such as Drive Up and Target Circle 360 seeing double-digit growth.

Source: Financial data Q2-2024 Target Inc.

The apparel category stood out with sales growth of more than three percent in Q2 2024, primarily indicating a recovery in discretionary (non-essential) consumer spending. Other categories, such as the largest sales segment Beauty, also continued to show strength. On the earnings side, there was also an upward trend, as the operating profit margin shows. In the second quarter, it was 6.4 per cent, an increase of 160 basis points compared to the previous year, which was ultimately due to a higher gross margin. The company was able to optimise costs here through improved purchasing activities, despite higher discounting and fulfilment costs.

Ultimately, earnings per share increased by more than 40 per cent year-on-year to USD 2.57. This shows that Target is not only experiencing a significant upturn in sales, but also in profitability. CEO Brian Cornell emphasised that the growth was driven entirely by increased customer traffic in both stores and digital channels.

Financially, Target not only reported higher sales and profits, but also reduced net debt through disciplined cost management. Higher dividends and share buybacks have increased the return to shareholders. Share buybacks are a particular focus. Over the last six years, more than 12 per cent of outstanding shares have been taken off the market in this way. Recently, however, the company has turned its back on buybacks due to operational weakness. This could change again in the future if business continues to pick up as it has done so far.

Source: StocksGuide Charts

Target stock forecast 2024 & 2025

For the third quarter, Target expects comparable sales growth of between zero and two per cent, while the full-year target is likely to be at the lower end of this range. Nevertheless, due to the strong profits in the first half of the year, full-year EPS is now forecast to rise to between $9 and $9.70. Compared to the previous year's figure of $8.94, this would be a visible increase. But even compared to the figures of the last ten years, these are exceptionally high EPS figures. They have never been matched, except in 2021. Despite the high figures, analysts do not expect this to be a one-time effect. They expect EPS to continue to rise to $11.39 by 2027.

Source: Earnings per share Target forecast 2025, 2026 to 2029

Revenues are also expected to continue to rise in the long term, although a slight decline is expected in the next two years. By 2029, revenues are expected to reach $125 billion, just under 17 per cent higher than the level expected in 2024.

Source: Target share sales and margin forecast 2025, 2026 to 2029

Key metrics for the Target stock from the dividend analysis

For dividend investors, Target could be a real gem in the portfolio, at least that's what the dividend score of twelve points suggests. The company not only has a long tradition of stable distributions, but also proves consistency in difficult market phases.

Source: Dividend analysis of the Target stock

In addition, the current dividend yield of 2.82 per cent is above the ten-year average of 2.56 per cent. Neither of these figures is exceptionally high, but they are solid. Accordingly, the first two criteria of the dividend analysis were only awarded one and two points respectively.

However, a particularly strong argument in favour of the Target share is the payout ratio, which has been low at 41 per cent over the last three years. In essence, this means that the company only uses a portion of its profits for dividend payments, while simultaneously ensuring that it has sufficient capital to invest in further growth, repay debt, buy back its own shares or react flexibly in times of crisis.

Source: Target stock dividends since 2000

It is also impressive that Target has paid uninterrupted dividends for more than ten years, which was rewarded with the full three points in the dividend analysis. Even better: the dividend has been increased every year for the last 53 years, which is a clear sign of confidence in the company's own financial strength. What's more, a dividend has always been paid since 1967.

Even more remarkable is the dividend growth of almost 12 per cent in the last five years. This ensures that investors receive dividends that increase faster than inflation itself. Combined with a strong share price performance of almost 150 per cent over the last ten years, the result is an attractive overall package.

The combination of stability, continuous growth and a responsible distribution policy could continue to make Target a truly top dividend investment, particularly for investors looking for reliable long-term income while also benefiting from rising dividends. With a low payout ratio and expected EPS growth over the medium term, the dividend should also continue to rise, although analysts expect a slight reduction over the next two years, before it visibly picks up again to USD 4.65 in 2027.

However, the risks should not be ignored. Stagnation at the operational level is the first warning signal for investors. No growth is being generated structurally in online retailing, and Target was also unable to make a mark in brick-and-mortar retailing last year. The figures for the first half of 2024, which showed low single-digit growth and strong profit increases, looked different.

Valuation of Target stock

At first glance, the valuation of Target shares appears attractive when you take a closer look at the key figures. The price-earnings ratio (P/E) is currently just under 16, which seems moderate compared to many other companies in the retail sector – especially in view of the stable earnings per share of $9.69 over the last twelve months (TTM). The forward price-to-earnings ratio of 16.6 also indicates a certain valuation stability. A further positive signal emerges from the enterprise value to free cash flow (EV/FCF) valuation. At 16.8, it is in a similar range to the price-to-earnings ratio.

Source: Valuation of the Target stock

The relatively inexpensive valuation could reflect the challenges that Target is facing. For example, sales growth over the last twelve months was slightly negative at -0.66 per cent, indicating that Target is currently operating in a difficult market environment. Nevertheless, free cash flow over the last twelve months remains robust at $5.27 billion, showing that the company is generating solid cash flows even in times of weaker sales.

In conclusion, the Target share appears fairly valued with a moderate P/E ratio and strong cash flows. The slight decline in sales over the last four quarters could be a warning signal, but the solid free cash flow and stable dividend could continue to make the company attractive for long-term dividend and value investors.

Conclusion on the Target stock

Overall, Target Corporation faces an exciting but challenging future in the dynamic US retail market. As one of the largest discounters in the country, the company has a solid base with a broad product range and a strong brand identity. The reliable dividend policy and a moderate P/E ratio make Target attractive for investors, no question.

However, the weaknesses in the areas of growth and e-commerce cannot be overlooked. To survive in the competitive arena, Target must further develop its digital strategy and proactively address the challenges of online retailing. The company has already taken steps in the right direction, but the pressure from competitors such as Amazon and Walmart remains high.

Future-oriented investments in technology, logistics and customer retention will be crucial to promoting growth and consolidating its market position. The strong free cash flow could be an important pillar in this regard. The latest quarterly figures have also shown that a great deal has already been achieved in terms of growth. This is also because the issue of inflation is no longer as much of a burden on consumers as it was a few quarters ago. By contrast, a potential economic downturn in the US could have a stronger impact on the figures.

Source: Analysts' opinions on Target stocks

Analysts tend to view the company as robust. However, they also expect a dividend cut in the coming year, 2025. In the long term, however, the trend could continue to be upward, as the forecast record dividend of USD 4.65 for the 2027 financial year indicates. In terms of recommendations, around half of analysts see the stock as a buy and half as a hold. The target price of $176.97 is 15.75 per cent above the current level.

If you would like to receive new investment ideas and free stock analyses selected according to the Levermann, High-Growth Investing or Dividend Strategy by email every week, you can now subscribe to our free StocksGuide newsletter.

The author and/or persons or companies associated with the StocksGuide own or may own shares in Target. This article represents an expression of opinion and not investment advice. Please note the legal information.