Table of Contents

- Company profile - Third largest exchange operator in the USA

- The latest Nasdaq quarterly figures from June 2024

- Nasdaq share forecast 2024

- Key figures of the Nasdaq share from the Levermann analysis

- Valuation of the Nasdaq share

- Conclusion on the Nasdaq share

Nasdaq shares (ISIN: US6311031081) may have been on the radar of many investors for some time. The share is likely to be of interest as it benefits directly from the upswing in technology stocks. As the leading stock exchange in the USA with a strong focus on technology stocks, the Nasdaq is undoubtedly a direct beneficiary of rising share prices in this sector.

It is hardly surprising that the company has recently recorded solid growth. Through strategic acquisitions, Nasdaq is also strengthening its focus on software and service solutions, which should lead to further increases in sales and profits in the long term and make the operating business less susceptible to fluctuations.

In the short term, however, cyclical business dominates, which may seem problematic in the current environment. However, in market crises such as the current one, the Nasdaq benefits from the nervousness of market participants. High volatility tends to be good for stock exchange operators, as there is significantly more trading.

Source: Nasdaq share price

The share price also seems to be rewarding these developments positively. Over the year, the share price has risen by more than 34 percent. At USD 67.92, the stock is now almost five times as expensive as it was ten years ago.

Although the expected price/earnings ratio (P/E ratio) of 34 already anticipates some future successes, the share could still be attractive for investors who believe in the continued growth potential of the technology and financial technology sector.

In the following Nasdaq share analysis, we will take a closer look at what exactly characterizes the Nasdaq share and whether it might be worth paying this premium.

The most important facts in brief

- With its focus on technology stocks, Nasdaq is a strong beneficiary of rising share prices, especially for technology stocks in the USA

- Takeovers are accelerating the strategic focus on software and services

- Higher sales and profits are likely in the long term

- An expected P/E ratio of 34 already anticipates a lot

Company profile - third largest stock exchange operator in the USA

Nasdaq is one of the world's largest marketplace operators. The company is known for the technology exchange of the same name. And in fact, it also earns the most money. The duel with the New York Stock Exchange (NYSE), which is now part of the Intercontinental Exchange Group (ICE), is both legendary and serious.

While the Nasdaq is dominated by innovative and technology-oriented companies, the NYSE is far more often home to value stocks. However, both are likely to have good business prospects. After all, they are growing in line with an ever-expanding financial market.

Several business areas diversify earnings

Source: Nasdaq 10-K Filing

Nasdaq's business model is divided into several business segments that focus on different aspects of the financial markets and financial technology. A key area is access to capital markets (Capital Access Platform). It accounts for the largest share of sales in terms of value. Around 46 percent of total sales are generated here.

In this area, Nasdaq offers data and listing services. Companies can list their shares on the Nasdaq exchange, which helps them to raise capital and increase their visibility. Specifically, Nasdaq earns from listing fees and for providing market information. The index segment comprises the development and management of indices, such as the well-known Nasdaq 100, which are used by investment funds and ETFs to map strategies. Here, too, Nasdaq earns handsomely through license fees for their use. Nasdaq also offers workflow and insight solutions that help companies to optimize their trading and analysis processes.

Financial technology

Another important business area that is becoming increasingly important is financial technology. It accounts for around 29 percent of total sales - and the trend is rising sharply thanks to acquisitions. In comparison to the largest business segment, significantly higher growth was recently reported here. This area is also less affected by the cyclical nature of the financial markets, which is crucial for the strategic direction of growth.

Specifically, Nasdaq offers technologies to combat financial crime, which help banks and other financial institutions to detect and prevent fraud and money laundering. In addition, Nasdaq develops regulatory technologies that help companies meet regulatory requirements. For example, Nasdaq's capital markets technology includes trading systems and software solutions that enable efficient and secure trading on exchanges and other trading venues.

Market Services

The third major area is market services, also known as Market Services. They accounted for around a quarter of revenue in the 2023 financial year. Nasdaq generates revenue in this area through the trading of shares and other securities. Other revenues also play a role, for example from the administration of clearing and settlement services. Finally, there are the transaction fees.

Together, these businesses enable Nasdaq to play a central role in the global financial markets by providing companies, investors and financial institutions with important services and technologies. Looking at the nature of its revenues, these are predominantly transaction-based revenues. As they are very cyclical and highly dependent on the mood on the capital market, they are naturally subject to major fluctuations.

A clear specialization compared to the competition

Nasdaq is uniquely positioned compared to its US competitors CME Group (Chicago Mercantile Exchange) and Intercontinental Exchange (ICE), although all three companies play an important role on the global financial markets.

Nasdaq, for example, is a leader in the equity markets, particularly for technology companies. The CME Group is a different story. It dominates derivatives trading, including futures and options, and is strong in agricultural, energy and financial derivatives. The Intercontinental Exchange (ICE) in turn has a strong position in commodities and equities trading and operates the New York Stock Exchange, an exchange specializing in lower-growth companies.

The strong focus on the USA is also a sign of specialization. Competitors from Europe such as Deutsche Börse, Euronext or the London Stock Exchange have no entry opportunities here due to the large moat. On the other hand, Nasdaq is also active in Europe with OMX. OMX AB is a leading exchange operator in the Nordic and Baltic countries and was acquired by Nasdaq in 2008 and integrated into the Nasdaq OMX Group. The OMX brand name was abandoned over time, but the Nordic business was further expanded. As far as international expansion is concerned, however, it must be admitted that it is limited. Although foreign sales are constantly increasing, they still play a subordinate role compared to total sales.

Source: aktien.guide Charts

In terms of market capitalization, Nasdaq is well behind its American competitors with a value of just under USD 40 billion. Compared to its international competitors, however, it has a visible size.

Here, too, it would be quite conceivable to strengthen the international business through a takeover. However, it has been shown that national stock exchange operators in Europe tend to compartmentalize their own business models and are rather critical of takeovers, which would make it more difficult for Nasdaq to expand outside the USA. This is not a bad thing, because even without this, Nasdaq has great potential for expansion. From an expansion of the software and services offering to an increase in the number of technology companies on the Nasdaq. Nasdaq is a direct beneficiary of the technology boom.

Deep moats secure the business model

Uniquely, the business of stock exchange operators is characterized by strict regulations that are monitored by national and international supervisory authorities. Such regulations aim to ensure market integrity, protect investors and minimize systemic risks. Established exchanges also benefit from high barriers to market entry, as setting up a new exchange requires huge investments in technology, infrastructure and regulatory requirements.

Stock exchanges have strong moats created by their network effects: The more companies and investors trade on an exchange, the more attractive it becomes for additional participants. This effect strengthens the position of existing exchanges and makes it more difficult for new competitors to enter the market. Technology also plays a key role in the industry: advanced trading systems and data analysis tools help to enable fast and efficient trading. Ultimately, it is precisely these technological investments and innovations that protect existing exchanges and strengthen their market position.

Takeovers drive growth

Let's move on to acquisitions. The growth of the Nasdaq names has been accelerated in recent years by inorganic acquisitions. Starting in 2000, Cinnober Financial Technology, a provider of multi-asset technology solutions for trading and clearing, was acquired for around USD 220 million. This was followed a year later by the acquisition of OneReport, a provider of environmental, social and governance (ESG) reporting solutions.

A year later, the acquisition of Verafin, a leading provider of solutions for combating financial crime, was announced. A total of 2.75 billion US dollars was put on the table for it. The acquisition strengthened the position in RegTech (regulatory technology) and made it possible to offer expanded solutions to combat money laundering and fraud.

In October 2021, AxiomSL, another provider of RegTech solutions, was finally acquired. AxiomSL's platform enables companies to efficiently manage large volumes of data and meet the requirements of various regulatory frameworks.

In 2022, Metrio, a Software-as-a-Service (SaaS) provider with a platform for collecting, monitoring, analyzing, disclosing and communicating detailed ESG data, was acquired. At USD 2.7 million, this was a smaller transaction.

This was followed in 2023 by the acquisition of the Adenza Group (USD 10.5 billion). Adenza is the joint venture of AxiomSL and Calypso, formed from the merger of the two companies. Adenza offers a comprehensive suite of software solutions for risk and regulatory management as well as for the trading and settlement of capital market products. The acquisition also strengthens Nasdaq's position in the areas of RegTech and financial technology.

Nasdaq's strategy clearly shows that it wants to further expand its range of technology and RegTech solutions and offer its customers more comprehensive services in the area of compliance. In addition, these business areas are less cyclical.

However, Nasdaq is also taking a certain balance sheet risk with its acquisitions. Intangible assets now account for 70% of total assets and are therefore almost twice as high as reported equity. In particular, the goodwill arising from acquisitions represents a potential write-down if the acquired companies do not develop as originally assumed at the time of acquisition. Of the 21.2 billion US dollars in intangible assets reported in the last quarter, just under 14 billion can be directly attributed to goodwill.

Source: Nasdaq Equity

The latest Nasdaq quarterly figures from June 2024

Source: Financial data from Nasdaq Q2/2024

The latest business figures from June 2024 were convincing across the board - also thanks to the numerous acquisitions. Revenue increased by a quarter to 1.8 billion US dollars. A similarly strong increase in profits was also reported at EBITDA level. However, the net result of USD 222 million was 17% below the comparable figure for the previous year.

The second quarter of 2024 was primarily impacted by write-downs on the acquisition of the platform operator Adenza. Extraordinary expenses of USD 85 million were incurred here. Unfortunately, the costs of the acquired companies AxiomSL and Calypso also increased. They drove up the cost base by 67 million. Finally, further restructuring costs of 37 million led to corresponding charges.

Nasdaq share forecast 2024

Source: Nasdaq Q2 earnings presentation 2024

The management has not provided shareholders with a concrete outlook for 2024 as a whole. The medium-term outlook also remains meagre. One explanation here could be the extreme cyclicality of the financial markets.

However, growth is expected in the medium term. In the somewhat more predictable areas (Financial Technology and Capital Access Platforms), for example, solid growth is forecast for the next three to five years. In the Financial Technology segment, this is likely to be well into double figures due to acquisitions.

Source: Analysts' sales forecast for Nasdaq shares

The analysts reveal more about their assessment for the current financial year 2024 on Nasdaq. They expect turnover to fall by 23% to USD 4.7 billion.

On the earnings side, EPS is expected to fall by just under 8 percent to USD 1.92. In the medium term, however, there should be a strong recovery here. EPS of USD 3.62 in 2028 would represent a significant increase on the last record EPS of the equivalent of USD 2.38 from 2021.

Source: Analysts' EPS forecast for the Nasdaq share

Key figures for the Nasdaq share from the Levermann analysis

The Nasdaq share appears promising in the Levermann analysis. From a fundamental point of view, the trading platform operator impresses with a good equity ratio of 33.5% for a financial company. The high EBIT margin of over 30 percent also deserves a point. However, as the company is classified as belonging to the financial sector, the analysis criteria do not award any points for this value. However, the expected profit growth of almost 29% is all the more convincing.

Source: Levermann analysis of the Nasdaq share

Points were also scored on the technical side. One point was awarded for the good medium to long-term share price performance. The same applies to the earnings revision and the reaction to the quarterly figures.

The main negative factor is the high valuation with an expected P/E ratio of over 35. The rolling 5-year P/E ratio is also not significantly lower at 30.7. A rather low return on equity of less than 10 % could also look better.

Valuation of the Nasdaq share

With an expected P/E ratio of 35.2, the valuation of Nasdaq shares can be described as ambitious. Especially as the company has only achieved moderate sales growth of 7.5% in the last twelve months and has a not inconsiderable level of debt. However, the gearing ratio is still visibly below 1, which is anything but critical.

Source: Valuation of the Nasdaq share

The dividend yield is also not providing any positive impetus. At 1.3%, it is currently even slightly below the 10-year average of 1.6%. On the other hand, high dividend growth of 8.7% over the last five years is convincing.

Conclusion on the Nasdaq share

To summarize, Nasdaq shares could offer an attractive opportunity for investors who want to benefit from the continued growth of technology stocks. After all, the Nasdaq is the largest technology stock exchange in the USA. And it is precisely here that the current sell-off in technology stocks is temporarily creating new opportunities, as high volatility tends to be good for stock exchange operators who earn money from fees. On the negative side, however, Nasdaq shares themselves are not spared from a market sell-off. The beta ratio, which measures the intensity of fluctuation compared to the market as a whole, is slightly less than 1.

The business model also stands for deep moats. As takeovers in the trading platform sector are extremely difficult, horizontal expansion is an obvious choice for Nasdaq. This is precisely where the company is making its mark with numerous acquisitions. The strategic focus on software and services is striking. They strengthen the long-term sales and profit potential and thus ensure a more predictable business. However, the acquisitions also entail risks. Intangible assets now dominate the balance sheet structure. Goodwill is greater than the equity shown in the balance sheet.

If it were not for the high price/earnings ratio of 38, which already reflects the equally high expectations for future earnings, the share could represent an interesting investment opportunity for long-term investors due to its leading market position and innovative strength. Above all, however, the strong market positioning and high margins show that the company could have earned a quality premium.

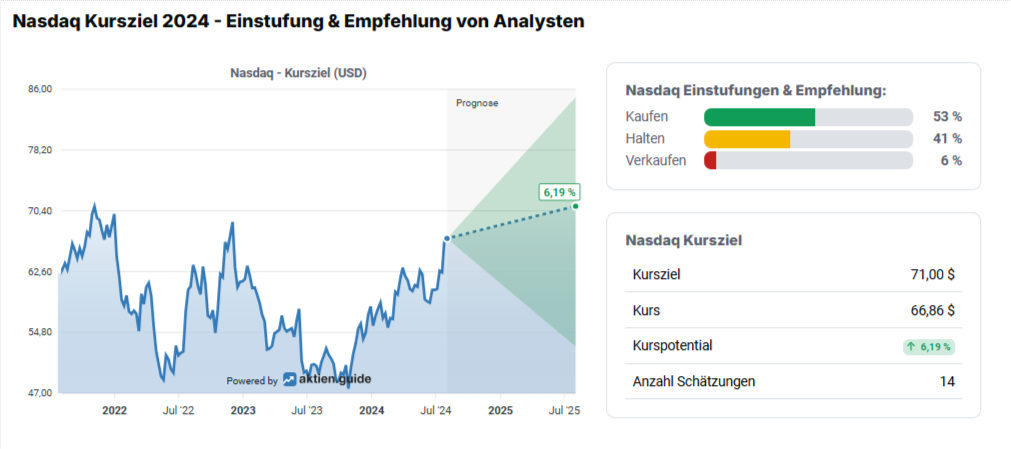

Source: Analysts' opinions on the Nasdaq share

The majority of analysts also see the share as a buy. More than half of the analysts recommend the share as a buy with an average price target of USD 71. However, the upside potential of 6.2 percent is not particularly high. Due to the high valuation, a hold position could therefore make sense, which 41% of analysts also recommend.