Table of Contents

Fashion stocks are currently being avoided by investors as they are considered cyclical and many companies in this sector have recently had to contend with declining sales and weaker demand.

It is therefore no wonder that some stocks in this sector have lost significant market capitalization over the last 12 months.

Source: Price losses of TTM Mode stocks

Whether it is the Canadian high-quality sports fashion manufacturer Lululemon Athletica, the German suit manufacturer Hugo Boss, the French luxury holding Kering (which includes Gucci, Bottega Veneta and Yves Saint Laurent) or the British luxury brand Burberry - what they all have in common is that their stock prices have plummeted by between 31% (Lululemon) and 68% (Burberry).

However, there is one company that manufactures such exclusive products that their demand has not waned even in the current times and this company continues to record high sales growth and profit growth. This company is the luxury company Hermès International (ISIN: FR0000052292), which was founded in Paris in 1837.

The Hermès stock price has increased eightfold in the last 10 years, providing its investors with a very good return.

In terms of market capitalization, Hermès is the second largest luxury company in the world. Only the LVMH holding company (Louis Vuitton, Dior, Marc Jacobs, etc.), which also comes from France, is ahead of it with a market capitalization of around 340 billion euros.

Source: Hermès market capitalization

Over the last 12 months, Hermès has continued to significantly increase its turnover and net profit, so there can be no question of weaker demand and a gloomy outlook.

Source: Hermès sales and profit growth TTM

But what makes Hermès so special that demand for its products continues to rise and how does the company intend to maintain its growth?

We now want to answer these and other questions as part of a Hermès stock analysis.

The most important facts in brief

- Second largest luxury goods manufacturer in the world by market capitalization behind LVMH

- Very high valuation of the stock

- Resilient business model thanks to high exclusivity

- All items are handmade and only available in limited quantities

- Birkin Bag is the status for expensive women's handbags

Company profile Hermès - premium luxury since 1837

Hermès was founded by Thierry Hermès in Paris in 1837. He produced high-quality tableware for the Parisian upper class. From the very beginning, he attached great importance to high-quality materials and simple designs. From 1880, the founder's son, Charles-Émile Hermès, also began to include horse saddles in the range. The harness and saddles became famous throughout Europe.

It is precisely these basic principles from back then that still characterize Hermès today. Only the highest quality materials are used and all items are still made by hand today. Whether scarf, shoe, tie, cushion, belt, trousers, dress or handbag. Each item takes many hours to make by hand and is only available in limited quantities. For a horse saddle, a Hermès employee comes specially to measure the contours of the horse so that each saddle is unique and numbered in a Hermès card index.

Hermès has had a partnership with its 50 most important suppliers for over 19 years and with its textile suppliers for 65 years. These long-term partnerships ensure that Hermès is able to purchase the high quality products it needs for its exclusive luxury products and the suppliers can count on Hermès as a long-term partner that can easily pass on increased product costs to its customers thanks to its pricing power.

The legendary Birkin Bag has been part of the Hermès range since 1984. It is named after the actress Jane Birkin, who happened to meet the then CEO Jean-Louis Dumas on a flight from Paris to London and spoke to him about the mess in her handbag when it fell on the floor. Dumas promised to develop a better handbag and then gave her the prototype. In return, Dumas was allowed to add it to the range as the Birkin Bag.

Today, this handbag is a symbol of luxury, as its value continues to rise rather than fall. At auctions, sums of over 200,000 dollars have been paid for a single Birkin Bag. This is due to the high uniqueness and desirability of the handbag, as it takes a bag maker between three days and two weeks to produce a single Birkin bag. This means that the finished quantity is deliberately low and the demand for the product is correspondingly high.

But it is not just fashion products that Hermès carries in its range.

Like its French competitors Kering and LVMH, it also offers other luxury goods such as watches, jewelry, make-up, perfumes and accessories.

Unlike the two competitors mentioned, all products are sold under the Hermès brand.

There are 294 stores in 45 countries. These are usually located in city centers or directly at major airports.

In Germany, for example, Hermès stores are located on Königsallee in Düsseldorf or in Berlin in the Kaufhaus des Westens (KaDeWe) and on Kurfürstendamm.

In New York City, there are three stores in Manhattan, including on Wall Street and Madison Avenue on the Upper East Side.

In this way, Hermès ensures its presence in places where customers with the means to buy such luxurious products go shopping. However, many items can also be ordered online.

From the analysis of the business model, we see that Hermès can demand a lot of money for its items, as each item is made by hand and only the best raw materials are used for production. To achieve this, Hermès relies on its long-standing partnerships with its suppliers. In addition, many items are only available for a limited time, which triggers a certain desirability among affluent customers. All these factors contribute to the high pricing power that makes Hermès so attractive to investors.

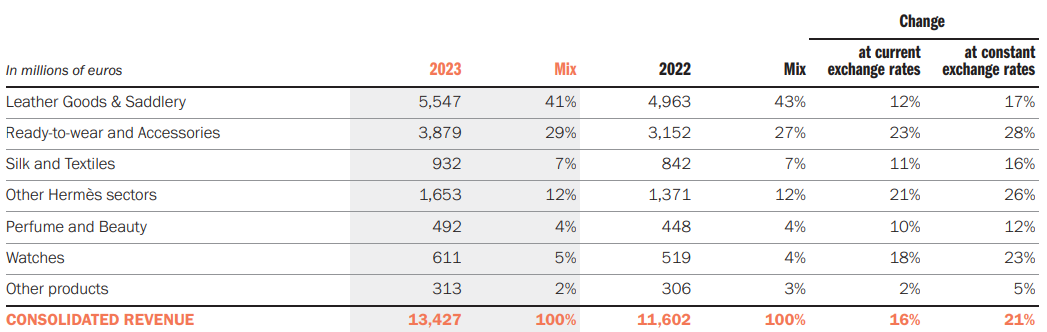

Hermès sales distribution

Hermès was able to increase its turnover by 16% to 13.43 billion euros in 2023. In constant currencies, this would even have been 21 percent. 21% organic sales growth is an impressive figure for a company of this size and against the backdrop of the aforementioned weakness in consumption at other companies in this sector. Let us now take a look at the distribution of the individual divisions and the geographical distribution of sales.

Source: Hermès 2023 annual report

As with LVMH, the Leather Goods & Saddlery division (handbags, saddles, travel bags, etc.) accounts for the largest stock of sales. In 2023, this segment accounted for 41%. It was followed by the Ready-to-Wear and Accessories sector (including shoes, belts, hats, etc.) with 29%

The Silk and Textiles segment includes ties, scarves and shawls. These only accounted for 7 percent of sales.

Taking all three segments together, Hermès generates 77 percent of its sales with fashion and equestrian articles.

Other Hermès sectors accounted for 12 percent. These include items such as jewelry, porcelain and furniture.

Perfume and Beauty accounts for only 4 percent and the Watches sector accounts for 5 percent. The remaining 2 percent belongs to the Other products segment, which offers glasses and special shoes and boots.

The high sales generation with fashion and equestrian articles is striking. There are also interesting observations in the geographical distribution of sales.

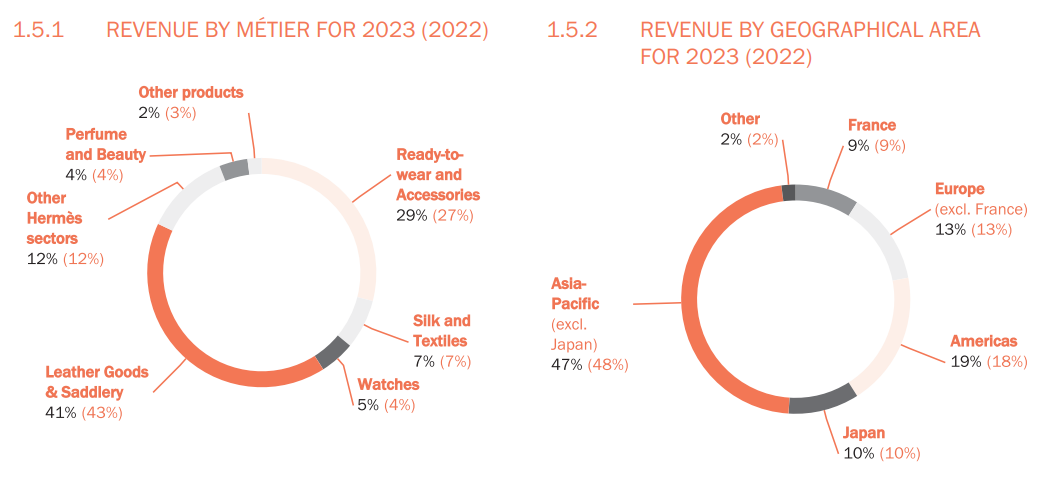

Source: Hermès 2023 annual report

At 47%, around half of annual sales are generated in the Asia-Pacific region, which largely comprises China and excludes Japan. Japan accounts for 10 percent of sales, while the Americas (North and South America) accounts for 19 percent. Europe accounts for 13% of sales, but not including France , which accounts for 9% of sales. Other (Near and Middle East) still accounts for 2 percent of sales.

Hermès' high exposure to Asia is striking. This area accounts for almost half of sales, making it a particular focus for investors, as possible declines in sales from this region would be more noticeable in the overall balance sheet than in France or Japan, for example. Not forgetting the political risks from this region, as China's government in particular regularly intervenes in the domestic economy and this could have a direct impact on Hermès' business.

All in all, however, it is clear that Hermès is a company with high barriers to market entry and a deep moat.

The latest quarterly figures from Hermès 2024

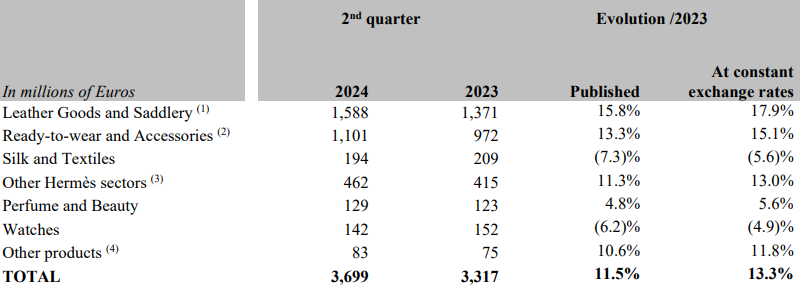

Hermès ' recently reported quarterly figures once again show the aforementioned pricing power and quality of the company and its products.

Source: Hermès 2024 half-year report

Sales increased by 11.5 percent to 3.7 billion euros. In organic terms, i.e. adjusted for currency effects, this would even be 13.3 percent. Sales growth was particularly strong in the Leather Goods & Saddlery and Ready-to-Wear and Accessories divisions. Growth of 16% (Leather Goods) and 13% (Ready-to-Wear) was reported here. However, there were also declines in two divisions. The Watches segment recorded a 6% drop in sales and the Silk and Textiles segment reported 7% less sales than in the same quarter of the previous year.

Measured against the economic environment, these sales increases are proof of pricing power and high corporate quality. In the course of the analysis, we will also look at the two competitors.

Based on the last 12 months (Trailing Twelve Months (TTM)), the situation at Hermès is as follows.

Source: Hermès P&L TTM

As administrative costs increased more than sales, EBIT still amounted to 5.94 billion euros. On the other hand, net profit rose by 13 percent to 4.45 billion euros.

Hermès compares very favorably with its two largest competitors.

Source: Hermès KPI comparison with LVMH and Kering

While LVMH' s sales and EBIT are virtually stagnating, the situation at Kering is much tighter. Sales fell by 10 percent and EBIT even plummeted by 35 percent. In terms of the free cash flow margin, it is noticeable that Hermès is once again clearly ahead with 26 percent.

LVMH currently achieves 15 percent, while Kering only reaches just under 12 percent.

Hermès' efficiency and market position can be seen most clearly in its turnover per employee. Kering and LVMH each achieve €400,000 per employee, Hermès €610,000. While Kering and LVMH require many employees for the marketing and sales of the individual brands due to the different Maisons (as the individual brands within the two holdings are called), Hermès can concentrate on one brand, which requires a significantly smaller marketing budget. In addition, LVMH and Kering have to offer stores in prime locations for each brand of their holdings, which in turn results in higher costs. This is where Hermès' advantage comes into play again, as it only sells its products under one brand and therefore requires fewer stores.

Hermès stock forecast 2024

How will Hermès growth continue? Let's take a look at the analysts' estimates for the current year.

Source: Hermès analysts' sales estimates

In addition to further double-digit sales growth for the current year, growth is expected to remain at a similar level in the coming years.

Source: Hermès analyst estimates revenue

Single-digit growth in sales to around EUR 20 billion is not expected until 2027. The net margin is expected to remain at over 30 percent of sales.

As Hermès continues to generate stable earnings even in the current rather challenging environment for consumer companies, the estimates for the following years could be realistic. As Hermès' target group appears to be much more resilient to economic fluctuations, growth could well be even higher.

Important key figures of the Hermès stock from the Levermann analysis

Only recently, Hermès was valued at 4 points according to the Levermann strategy. The stock had therefore briefly cleared the required hurdle of 4 points. It was therefore listed as a top scorer stock.

Recently, however, the score has fallen to zero points.

Source: Hermès (Hermes International) - Levermann strategy: Key figures

The equity ratio of 75 percent is impressively high, as is the return on equity of 28 percent. One point is awarded for each.

The EBIT margin of 42 percent is also exceptional. Here, 12 percent would have already earned one point.

The value receives deductions for its valuation. Both the average P/E ratio (price/earnings ratio) over the last 5 years is 57 and the P/E ratio in relation to next year's earnings is 49. Hermès would have to significantly increase its earnings per stock (EPS) or the stock price would have to fall significantly in order to reach the target value of 16, which would no longer lead to a deduction of points. The stock receives a further point for earnings growth of 11 percent.

While many companies are currently struggling to stay in the profit zone at all, Hermès' profit growth has rarely been below 10 percent.

Source: Hermès stock profit growth

Although profit growth has fluctuated over the last five years, it has generally been consistently above 10% and the increase during the pandemic year 2020 is very clear, when the French company was even able to report a profit increase of over 40%.

The Levermann analysis highlights all the aspects of the Hermès stock already mentioned. The company scores with a very good capital structure, return on capital and earnings growth, while the valuation suggests that Hermès' stocks and products appear to be similarly priced.

Valuation of the Hermès stock

It has already become clear that the Hermès stock appears to be very highly valued.

With a current P/E ratio of 50, the stock looks expensively valued. Based on this, analysts expect only moderate growth in EPS (earnings per stock).

Source: Hermès EPS forecast 2024

With an average EPS forecast for 2028 of EUR 135, the stock still appears to be highly valued with a P/E ratio of 35 for 2028. The average expected annual earnings growth of just over 10% seems too low in comparison, as LVMH stocks, for example, are expected to see similarly high earnings growth in the coming years and the valuation of the Louis Vuitton parent company is currently only around half as high as that of Hermès.

Let's see how the Hermès stock compares with its two biggest competitors.

Hermès comparison with Kering and LVMH

Even in comparison with the stocks of LVMH and Kering, Hermès stocks still appear highly valued.

Source: Hermès comparison with LVMH and Kering

With a ratio of enterprise value to sales (EV/sales) of 15, the stock appears to be valued like a premium cloud company from America with recurring sales thanks to the subscription model, very high sales growth and an 80% gross margin. The peer group here is at values of 2.6 (Kering) and 4 (LVMH).

The enterprise value - free cash flow ratio (EV/FCF) for Hermès is 58, which appears to be similar to the P/E ratio. In contrast, the peer group looks different. LVMH's free cash flow multiple is around 28 and Kering's is 22. If the growth rates of both companies are taken into account, Hermès' two competitors do not appear favorable either.

Although Hermès is currently holding its own against its competitors in terms of growth factors such as sales and profit growth, the stock still looks highly valued even after the comparison. It seems as if the stock and its legendary Burkin Bag have a similar price.

Conclusion on the Hermès stock

The fact that Hermès appears to be a great luxury company has become clear in every single point considered in the analysis.

The clientele is wealthy and does not have to hold back its spending on expensive luxury consumption. Hermès continues to supply high-quality items with rarity value and its products are correspondingly sought-after.

This ensures stable cash flows, which are also used to pay a (small) dividend.

Source: Hermès stock dividend

Although the current dividend yield is only 0.71%, the growth in dividend payments has averaged 27% per year over the last 5 years. This means that dividend investors could also achieve a good dividend yield in relation to their entry price in just a few years.

Analysts are divided when it comes to a current rating for Hermès stocks.

Source: Hermès analyst estimates

10 out of 22 analysts still see the stock as a buy even at the current level, but the average price potential is estimated at only 8 percent. In contrast, 10 analysts would currently only hold the stock and 2 experts even rate the stock as a sell.

The high valuation of the stock must once again be noted as a point of criticism, as the stocks of its largest competitor LVMH are currently available to buy at a much lower valuation level in comparison. The growth expected by analysts for both companies is estimated to be similarly high.

The fact that Hermès appears to be somewhat less susceptible to economic fluctuations is shown by the companies' latest quarterly figures.

The premium luxury stock thus appears to be Hermès and seems to demand a corresponding fortune for it - as well as for its products.

A lower level such as a P/E ratio of 35 could be a valuation to re-analyze the stock. Therefore, a P/E alert of 35 might seem reasonable.

.jpg)