Table of Contents

A roof over one's head is one of the most basic human needs. D.R. Horton (ISIN: US23331A1097) is often the right partner - at least in the USA. Since its founding in 1978, the company has grown to become America's largest homebuilder and now plays a leading role in the important residential construction sector. The company is benefiting from megatrends such as the continuing demand for affordable housing in the US, a nation characterized by industry and immigration.

The market is challenging, cyclical and highly competitive. Competition from existing buildings, but above all from competitors who are undertaking similar projects for clients. But despite the challenges in the construction industry, there is good money to be made in residential construction. In particular, the current high level of prices for existing homes could drive demand for new construction.

D.R. Horton's consistently high margins and healthy balance sheet, as well as the company's highly stable earnings and solid cash flows over the years, are strong arguments for the stock. This has been passed on to shareholders in the form of share buybacks, dividends and, ultimately, rising share prices. In the last ten years alone, the share price has increased almost eightfold!

Source: D.R. Horton share price performance over 10 years, StocksGuide

The current low valuation may suggest upside potential, especially given the market opportunities. However, economic headwinds from persistently high interest rates and inflation should also be taken into account. Both have an impact on overall market performance. Recent quarterly figures have revealed visible weaknesses in this regard. The following analysis of the D.R. Horton share will explain in more detail the arguments for and against the share.

Key facts in a nutshell

- D.R. Horton is America's largest homebuilder

- The business is cyclical and highly competitive

- Nevertheless, there is good money to be made in homebuilding

- Horton's balance sheet is strong and margins are high.

- A low valuation could be an argument for the stock, but there are uncertainties.

Company profile - America's largest homebuilder

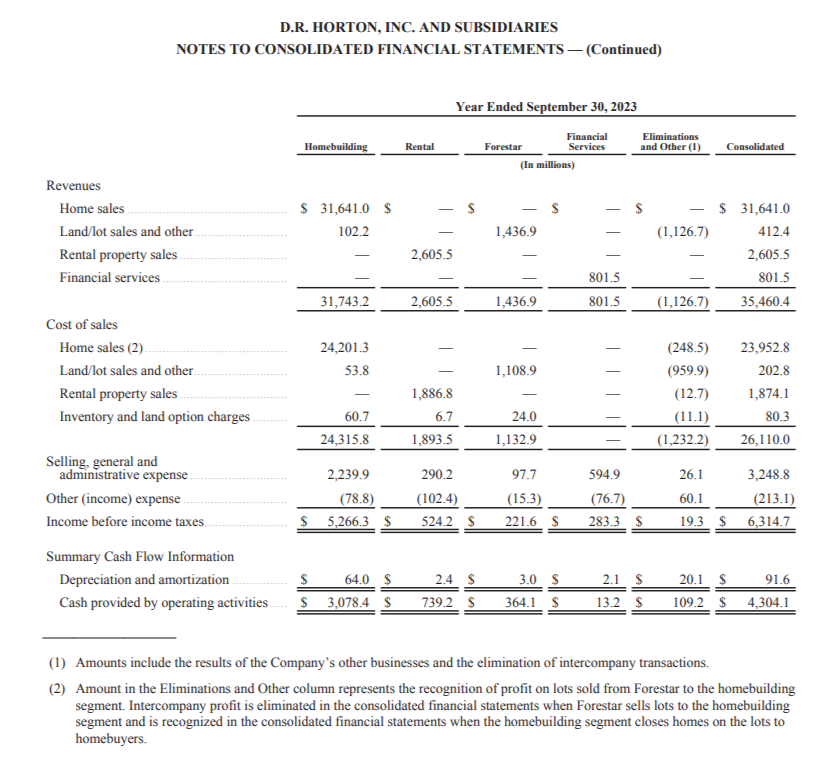

D.R. Horton is the largest homebuilder in the US and has a diversified business model that goes beyond just building and selling homes. The company's homebuilding, rental, Forestar and financial services businesses cover key areas of the housing market.

Source: D.R. Horton 2023 Annual Report

Founded in 1978 by Donald R. Horton, D.R. Horton designs, builds and sells single-family homes for a wide range of customers, from first-time homebuyers and young families to affluent buyers. The company serves a range of needs and price points through its Express Homes, Emerald Homes and Freedom Homes brands. With a large number of projects in more than 100 markets and 30 states, D.R. Horton can also build more cost-effectively and efficiently than many smaller builders, giving the company an advantage in a highly competitive market. With total revenues of $31.7 billion in fiscal 2023, this segment is by far the largest, accounting for nearly 90 percent of revenues.

In addition to homebuilding, D.R. Horton has developed a rental business to meet the growing demand for rental housing. The focus is on single-family homes in newly developed communities for rent. It is targeted at families and individuals who want the benefits of a single-family home without having to buy one. The Single-Family Homes division builds and rents out single-family homes in specially developed communities. Once these homes are rented out, the entire development is usually sold as a collection of rental properties. In the multi-family rental sector, the company develops, builds and rents out multi-family houses, i.e. larger residential complexes with several residential units. These developments are often sold as a whole after completion and letting. Both the single-family and multifamily segments provide D.R. Horton with additional revenue streams and the ability to meet the growing demand for rental housing.

But it also appeals to other buyer groups, such as institutional investors focused on stable rental income. In 2023, the sale of such rental properties will generate just over USD 2.6 billion in revenue. However, this is a relatively small sideline, accounting for only 7.2% of revenues.

Another important business is Forestar, a property development company in which D.R. Horton acquired a 75 percent stake in 2017. Forestar buys land, develops it and prepares it for homebuilding projects. This enables D.R. Horton to develop land independently of external land suppliers and owners and to include it in its home building projects at favorable prices. This ultimately lowers costs and gives the company a strategic advantage over its competitors. Forestar also sells land to other developers, generating additional revenue. In fiscal 2023, revenue from land sales amounted to approximately USD 1.4 billion. At 4% of sales, this is not a large proportion of consolidated sales, but it is strategically important.

The business model is rounded off by the Financial Services division, which provides financing and insurance for homebuyers. The subsidiary DHI Mortgage provides customers with mortgage financing. Home insurance is also offered. For D.R. Horton, this means that many buyers can complete the entire home buying process directly with the company - from financing to insurance to the actual purchase. This not only strengthens customer loyalty, but also gives D.R. Horton has more control over the actual sales process. The division generated sales of just over USD 800 million in fiscal 2023.

D.R. Horton offers a broad range of services combining homebuilding, home-rental, land development and financial services. This vertical integration helps the company meet the needs of its customers and compete successfully in the highly competitive US homebuilding market.

The market

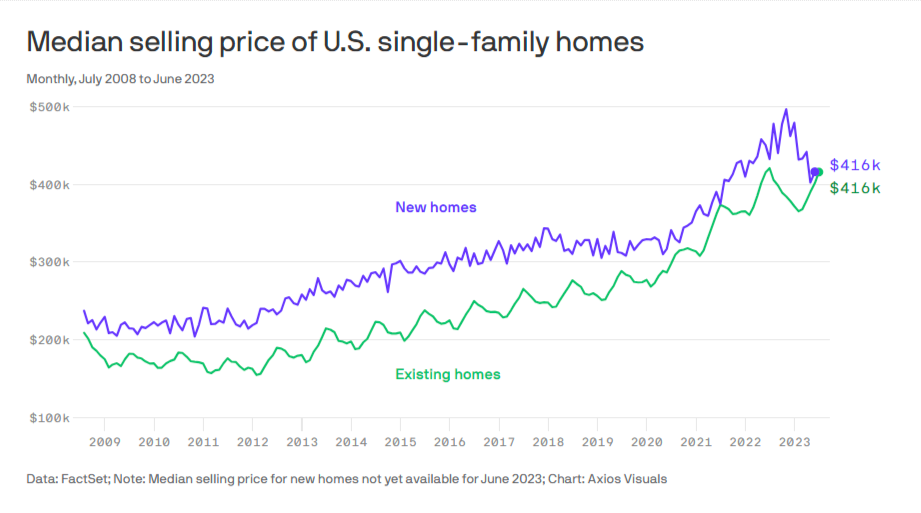

The US housing market is characterized by strong demand, driven by population growth, a high number of first-time buyers and an increasing demand for single-family homes (prosperity development). While demand for housing is stable over the long term, it often fluctuates in the short and medium term depending on economic factors such as interest rates, inflation and the state of the economy. Rising interest rates affect financing conditions and make it more expensive for many people to buy a home, but this increases the demand for affordable homes and rental accommodation. However, the price of existing homes also plays a role in the demand for new D.R. Horton homes. When existing home prices are high and construction costs are low, demand for new homes tends to be higher. Historically, however, this has rarely been the case, as the following chart shows.

Source: US sales price trends for existing and new homes, Axios.com

D.R. Horton relies primarily on subcontractors to complete its homebuilding projects. Although the company manages and oversees the entire construction process, the actual construction work is usually outsourced to specialized subcontractors. While this strategy is somewhat expensive, it allows for a flexible and scalable approach. It enables the company to respond quickly to fluctuations in demand without having to maintain a large in-house construction workforce. Ultimately, working with a variety of local subcontractors allows for effective cost control while taking advantage of the subcontractors' regional market knowledge. This is particularly important as D.R. Horton operates in many different geographies and must take into account varying regulatory requirements and local market conditions.

An important industry trend is the growing interest in single-family rental homes, driven in part by the desire for more flexible living. Many young buyers and families (Gen Z) now prefer to rent rather than buy, opening up new business opportunities for new players such as institutional landlords and housing associations.

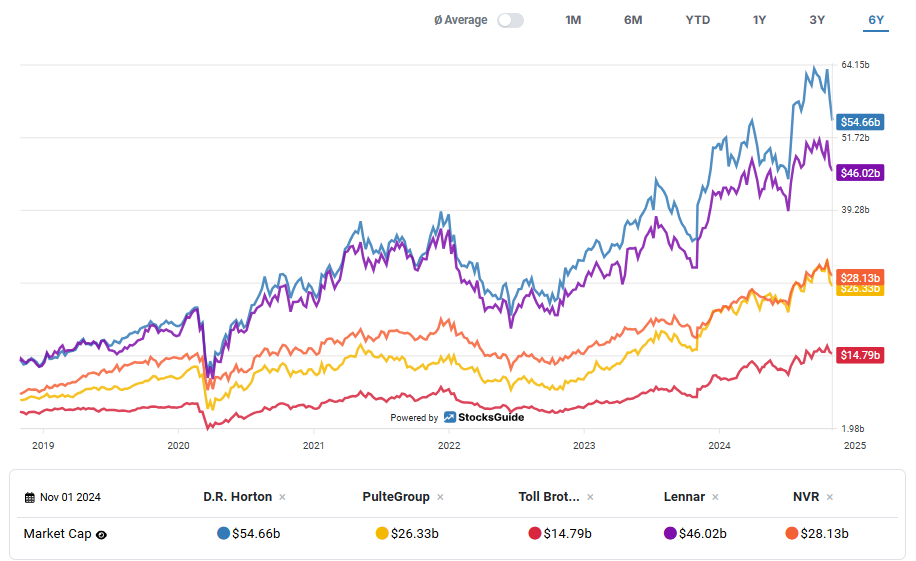

Competition

There is also strong competition for affordable land in popular and fast-growing regions. This competition is being intensified by companies specializing in land development. For homebuilders like D.R. Horton, this is a challenge, but also an opportunity to position ourselves strategically through our own land development projects. However, the market is also regulated, which has an impact on the construction and development of new neighborhoods. New legislation can affect both supply and demand. As mentioned earlier, competition is fierce. After all, anyone can build a house, and every citizen has free access to building materials. But a market leader like D.R. Horton can offer more. It starts with synergies and volume discounts when buying in bulk, and extends through the entire building, financing and marketing process.

Source: D.R. Horton's market capitalisation and peer group performance, StocksGuide Charts

D.R. Horton's main competitors include other leading homebuilders who, like D.R. Horton, focus on the US market and often target similar customers. One example is Lennar Corporation, one of the largest homebuilders in the US. Lennar also offers a wide range of homes for different target groups and supports the buying process with its own mortgage and insurance services. As a result, Lennar competes directly with D.R. Horton in almost all key regions and segments, particularly in the area of homes for first-time buyers.

Another significant competitor is PulteGroup. With brands such as Pulte Homes, Centex and Del Webb, it offers homes in a range of price segments, from affordable single-family homes to luxury properties. PulteGroup also emphasizes efficient building processes and has a strong presence in many regions of the US. It offers potential buyers a competitive alternative to D.R. Horton in the areas where it operates.

NVR is also a significant competitor, although it is less geographically diversified than D.R. Horton. NVR focuses on single-family homes and townhomes, particularly in the eastern and central United States. With a strategy focused on efficiency and profitability, NVR competes primarily in markets where there is high demand for affordable homes in good locations.

Toll Brothers, on the other hand, specializes in the upper end of the market and is best known for its luxury homes. Although D.R. Horton and Toll Brothers serve slightly different target groups, they compete in the upper price segment, particularly in affluent areas where demand for high-quality homes is high.

Finally, the slightly smaller KB Home is another direct competitor. KB Home focuses on affordable housing solutions for first-time buyers. The Californian company is present in the main US markets and, like D.R. Horton, offers financing and mortgage services to facilitate the home-buying process.

In addition to these major homebuilders, there is strong competition in the single-family rental sector. Companies such as Invitation Homes and American Homes 4 Rent have invested heavily in single-family rental housing in recent years. They are responding to the growing demand for rental housing in the US. However, these companies pose a challenge to D.R. Horton as they are also targeting valuable development land and the rental customer segment.

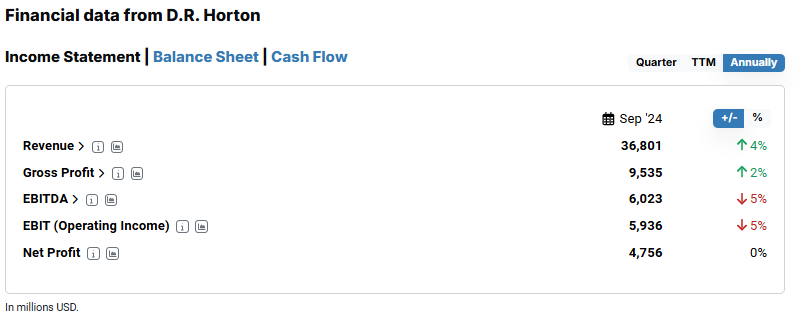

D.R. Horton's latest quarterly figures from September 2024

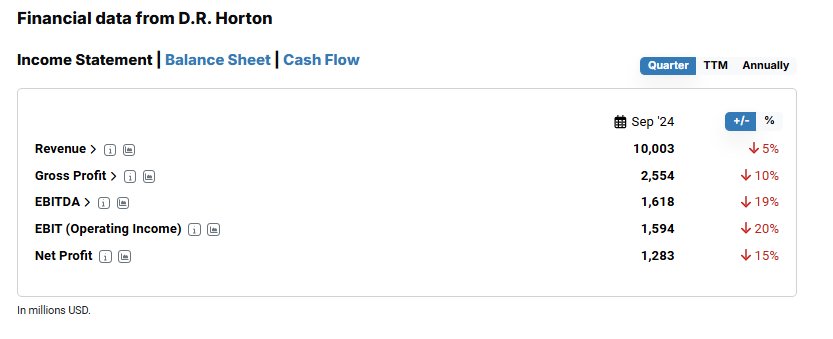

Due to the economic challenges, D.R. Horton was only able to report mediocre figures for the fourth quarter of fiscal 2024. This particularly disappointed investors who had expected more.

Source: D.R. Horton quarterly figures for Q4-2024, StocksGuide

Overall, Q4-2024 ended with revenues down five per cent to $10 billion. Net income was $1.3 billion, down nearly 15 percent from a year earlier. This compares with growth of one per cent in the previous quarter. This is a further deterioration in economic momentum compared to the previous quarter.

Source: D.R. Horton annual figures for Q4-2024, StocksGuide

For the full year 2024, revenues are now on track to reach $36.8bn. That's almost four percent more than last year. Net income reached 4.8 billion. This is in line with the comparable figure for the previous year. Although the sales forecast was just met, the company fell short of analysts' expectations.

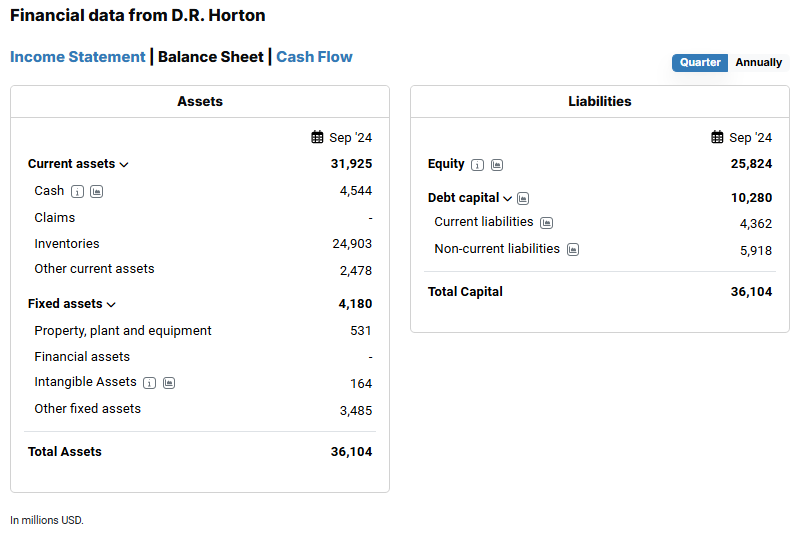

In the homebuilding segment, D.R. Horton increased full-year sales by 7 percent to $34 billion and increased the number of homes completed to nearly 89,700. Demand remained robust, although sales were down slightly on the previous year as a result of declining margins. Nevertheless, the company generated a solid cash flow of $2.2 billion and has a remarkably low gearing of 18.9%, providing additional financial flexibility for the year ahead. Inventories stood at 37,400 homes, which could provide a solid base for the new year given the expected demand for affordable housing.

The rental business, however, was down on the previous year. The segment reported a pre-tax profit of $229 million on revenues of $1.7 billion, down from the previous year. The decline was due to a lower number of home sales. D.R. Horton continued to focus on smaller and more affordable developments.

In contrast, Forestar, D.R. Horton's majority-owned homebuilding subsidiary, experienced an upturn. Sales increased slightly to USD 1.5 billion and pre-tax profit rose to USD 270 million. This was driven by an increase in the number of homes sold and improved margins.

Finally, the company was able to significantly increase returns to shareholders through improved construction cycles and targeted adjustments such as the expansion of the affordable housing offering and strategic share buybacks. The quarterly dividend was increased by one third to $0.40 per share. With robust liquidity of $7.6 billion and a $500 million repayment of existing bonds, the company remains strategically well positioned to meet the challenges and demand of 2025.

However, more momentum could come from the core business as a whole. The figures reflect the impact of recent central bank policy. Many new home buyers are still holding back in anticipation of falling interest rates. The persistently high price level for existing homes does not change this. On average in the US, it is now more expensive to buy an existing home than to build a new one.

D.R. Horton stock forecast 2025

D.R. Horton has provided cautious but optimistic guidance for fiscal year 2025 based on current market conditions. The company now expects total revenues to be between $36 billion and $37.5 billion and plans to deliver between 90,000 and 92,000 homes. The tax rate is expected to be around 24.5%. In addition, operating cash flow is expected to be higher than in 2024. Significant capital measures are planned, including share buybacks of approximately USD 2.4 billion and dividend payments of approximately USD 500 million.

Analysts' views on D.R. Horton stock

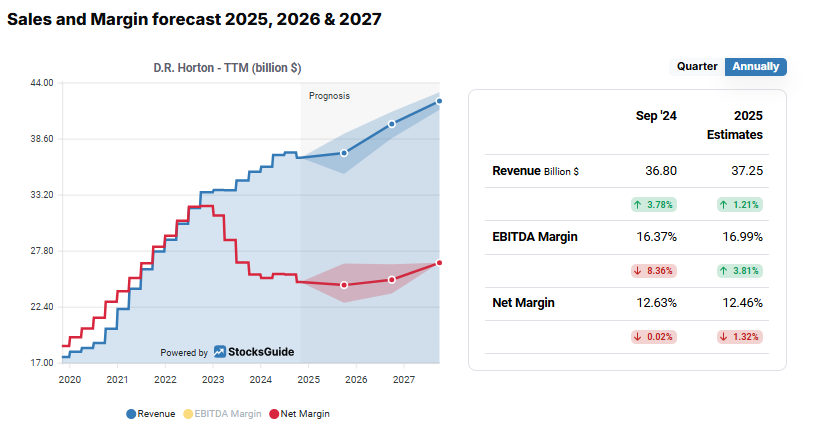

Analysts' views on D.R. Horton's sales and earnings forecasts are consistently positive. Promising growth potential is seen for the coming years. Moderate sales growth of 1.2% is forecast for 2025. This is respectable given the challenging market conditions, such as high interest rates and inflation, and the current weak economy.

Source: D.R. Horton sales and margin forecasts

Analysts also have a positive outlook for the coming years. For example, sales are expected to grow at a mid-single-digit rate. Even if the growth rate declines somewhat in 2027, the analysts believe that D.R. Horton is well positioned to benefit from the continued demand for housing in the US. As a megatrend, population growth should have a positive impact.

Net income is also expected to continue to grow in the medium term, with double-digit growth from 2026 onwards. This should keep the company on a profitable growth path. Overall, the analysts' opinions reflect strong confidence in D.R. Horton's long-term prospects.

D.R. Horton stock key metrics from the Levermann analysis

D.R. Horton's stock scores 5 out of 13 points in the Levermann analysis, and is particularly strong on fundamental measures such as EBIT margin and equity ratio. The stock is also supported by solid future earnings growth and a moderate valuation with low debt.

Source: Levermann Score for D.R. Horton stock, StocksGuide

The EBIT margin of 16.1% shows a strong performance. It shows how much profit D.R. Horton has left before interest and taxes. The higher the better. The extremely high equity ratio of 70 percent also shows that D.R. Horton has a solid financial base, despite share buybacks and dividends. Ultimately, a high equity ratio indicates financial stability and low dependence on banks. This is particularly beneficial in an industry that is often affected by interest rates and financing costs.

D.R. Horton's strong financial position not only allows it to invest in growth, but also protects it from the risks of market volatility and economic downturns.

Source: D.R. Horton balance sheet data September 2024, StocksGuide

The expected earnings growth of over 10% is also positive and resulted in a point in the Levermann analysis. From a technical point of view, D.R. Horton's shares also look promising for short and medium-term gains. The stock's sell-off on the day of its quarterly and full-year results did little to change this.

Valuation of D.R. Horton stock

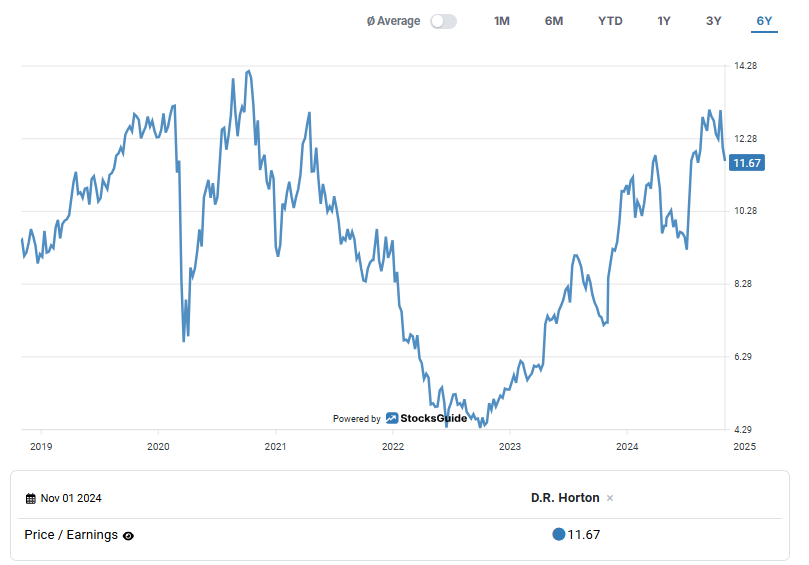

The valuation of D.R. Horton's shares provide some interesting metrics that may be of interest to potential investors. For example, the price-to-earnings (P/E) ratio of around 12 is relatively cheap compared to the earnings generated by a company with low debt, a high equity ratio and growth prospects. The same goes for the forward P/E of 11.8. This view is supported once again. However, both are at the upper end of the historical valuation scale.

Source: Historical P/E of D.R. Horton stock

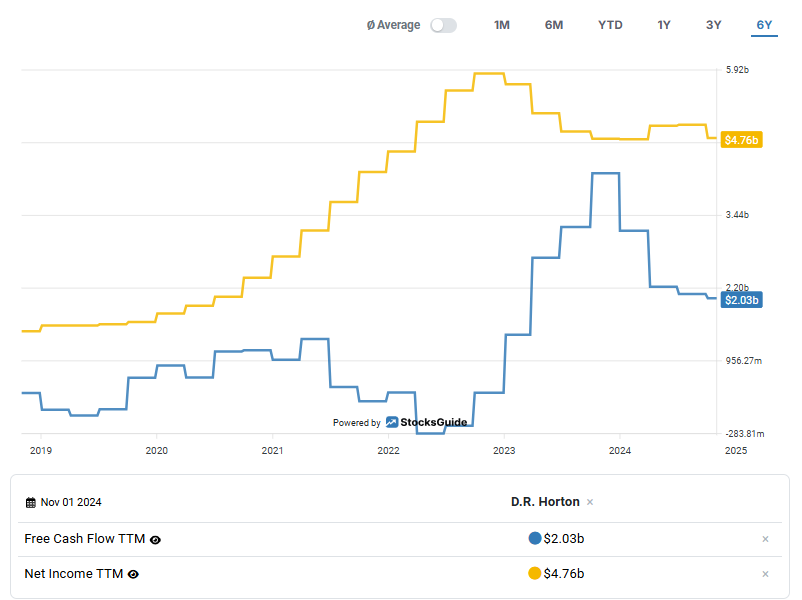

In contrast, the EV/FCF ratio of 28 paints a different picture. It shows the market's valuation of the company in relation to its free cash flow. The divergence from the P/E ratio indicates weakness in free cash generation. Although sufficient funds are generated, the free cash flow of USD 2 billion over the last twelve months is significantly lower than the reported profit of USD 4.8 billion over the last four quarters. This is not a new phenomenon. It can be explained by the large sums paid for completed properties, which are then held as current assets on the balance sheet. The difference between net profit and free cash flow arises because property expenditure affects cash flow but does not directly affect profit: when the company buys property, it uses cash to do so, reducing free cash flow. However, this property is then entered on the balance sheet as a current asset, with no initial impact on the profit and loss account - so net profit is higher than free cash flow.

Source: Earnings and Free Cash Flow Trends for D.R. Horton stock

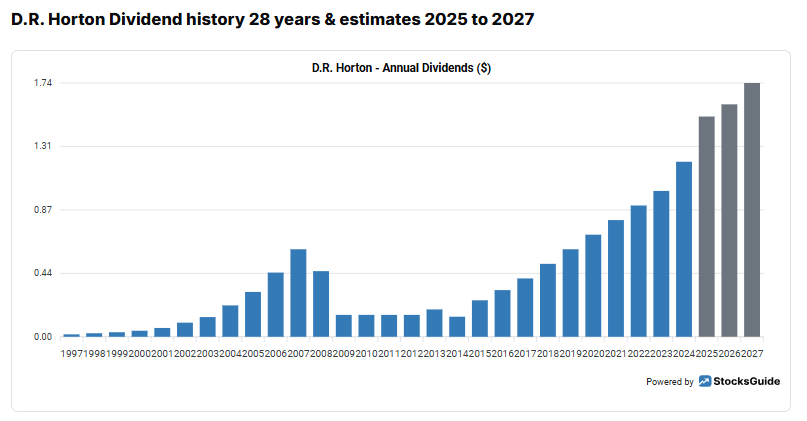

The dividend yield is also nothing to get excited about. At 0.7%, it is extremely low. This is mainly due to the low payout ratio. The payout ratio, for example, is very low at 6.9%. As the dividend history shows, the dividend is also quickly reduced in times of crisis.

Source: D.R. Horton Dividend History 25 Years & Forecast to 2027

A similar picture emerges for share buybacks. They have been carried out consistently in recent years, but only in good times. From 2013 to 2018, the number of shares outstanding increased, complementing periods of weak economic activity.

The valuation could therefore reflect certain systemic risks related to the capital intensity of the business model. Especially during the financial crisis of 2008/2009, companies like D.R. Horton was exposed to existential risks. A collapsing housing market in America was not a good business environment. At the time, the share price plummeted from over USD 40 to under USD 5. We saw a similar development during the coronavirus crisis. Ultimately, the stock is a bet on the state of the US housing market, especially the new construction market, which competes with existing properties.

Conclusion on D.R. Horton stock

Despite the current challenges associated with the cyclical nature of homebuilding and strong competition, D.R. Horton stock could be an interesting investment opportunity. As America's largest homebuilder, the company has a strong market position that translates into significant financial advantages over its competitors. Its healthy balance sheet, solid margins and high return on equity and assets speak for themselves. Its attractive valuation and growth potential should also not be overlooked.

However, investors should keep an eye on economic risks, such as high interest rates and inflation, to guard against a potential decline in demand for new homes. The financial crisis of 2008/2009 highlighted the vulnerability of the housebuilding sector. The coronavirus crisis also highlighted the high sensitivity of investors when it comes to trading housing stocks on the stock exchange.

However, the continued demand for housing, combined with D.R. Horton's strong market position and flexible product offerings, could enable the company to operate successfully even in a challenging environment. In particular, the current high level of prices for existing homes could lead to increased demand in the medium term. This should be taken into account. The central banks' policy of lowering interest rates is currently having a negative effect. Buyers are holding back in the market in anticipation of more favorable financing conditions.

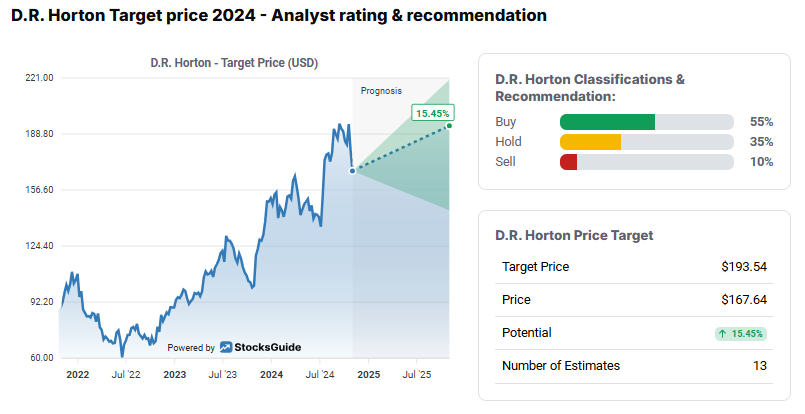

Source: Analysts' price targets for D.R. Horton stock, StocksGuide

Analysts have a similar view of the stock. They currently see it with an average target price of US$193. Based on the most recent share price, this represents an upside potential of a good 14.5 per cent. More than half of the analysts recommend buying the stock, 35 percent view it as a hold and only 10 per cent recommend selling it.

If you would like to receive new investment ideas and free stock analyses selected according to the Levermann, High-Growth Investing or Dividend Strategy by email every week, you can now subscribe to our free StocksGuide newsletter.

The author and/or persons or companies associated with the StocksGuide own or may own shares in D.R. Horton. This article represents an expression of opinion and not investment advice. Please note the legal information.

.jpg)