Table of Contents

- Company profile – globally active financial services provider

- The latest S&P Global quarterly figures for March 2025

- S&P Global stock forecast for 2025

- Key figures for S&P Global stock from the Levermann analysis

- Valuation of S&P Global stock

Reliable information is a key competitive factor. Companies, investors, banks, governments, and regulatory authorities need accurate, comparable, and timely data to make informed decisions—for example, when investing, lending, analyzing risk, regulating, or strategic planning.

Financial services provider S&P Global (ISIN: US78409V1044) provides precisely this information. The New York-based company is one of the world's leading sources of credit ratings, financial market analysis, macroeconomic data, commodity prices, benchmark indices, and ESG ratings. This content is often deeply integrated into regulatory processes, financial products, and internal control mechanisms of customers. Many of its products, such as credit ratings and the S&P 500 Index, are not only economically relevant but also legally relevant and are considered market standards. In today's increasingly information-driven economy, the business of a data provider is comparable to a gold mine.

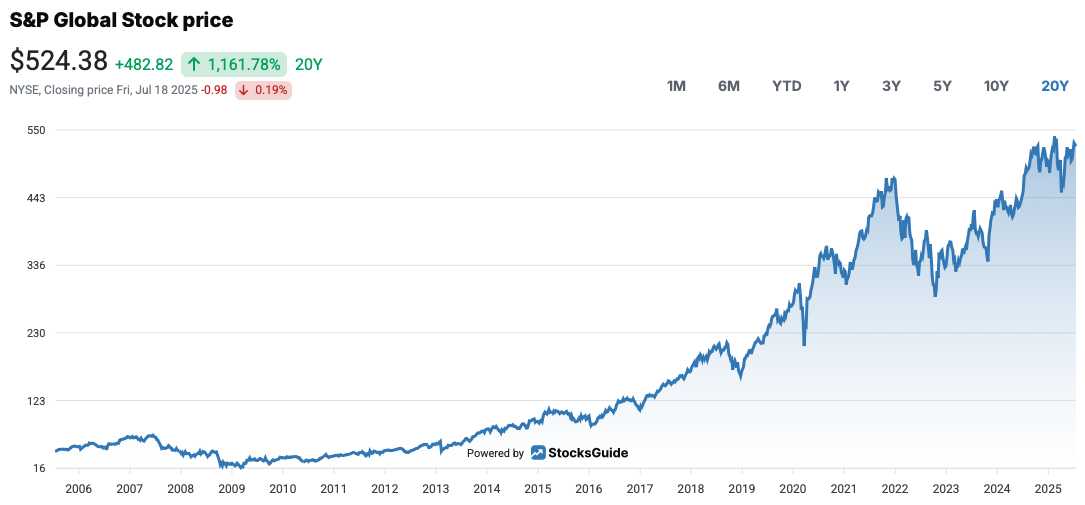

Investors have also recognized this, as the steadily rising stock price shows. Over a period of 20 years, it has been a tenbagger.

Source: S&P Global stock price

But not everything is rosy. The stock has often fallen sharply in times of crisis. For example, it lost 75 percent of its all-time high during the 2009 financial crisis. It also fell by almost 40 percent during the coronavirus pandemic. This is mainly due to the stock's high valuation and its link to the cyclical financial sector.

However, S&P Global is in a strong position thanks to long-term subscription payments. In addition, long-term trends should provide tailwinds. Especially in times of economic uncertainty, geopolitical tensions, or monetary policy upheavals, demand for high-quality data and independent assessments increases. Market participants rely on S&P Global more than ever to gain transparency, identify risks, and evaluate opportunities. It is no longer just about historical figures, but about in-depth analysis, scenarios, automated signals, and, increasingly, AI-powered forecasts—all of which S&P Global provides. In addition, the strategic importance of such information services is growing with the requirements for sustainability reporting, regulatory compliance, and digital transformation. In this environment, S&P Global benefits from its unique combination of data breadth, analytical depth, technological expertise, and global reach. This gives the company a stable competitive position and strong pricing power.

Against this backdrop, it is clear why S&P Global stock is not only an investment in a data company, but also, in a sense, an indirect investment in the functioning of global markets themselves. This could pay off for shareholders in the long term, as the following S&P Global stock analysis will show.

Company profile – globally active financial services provider

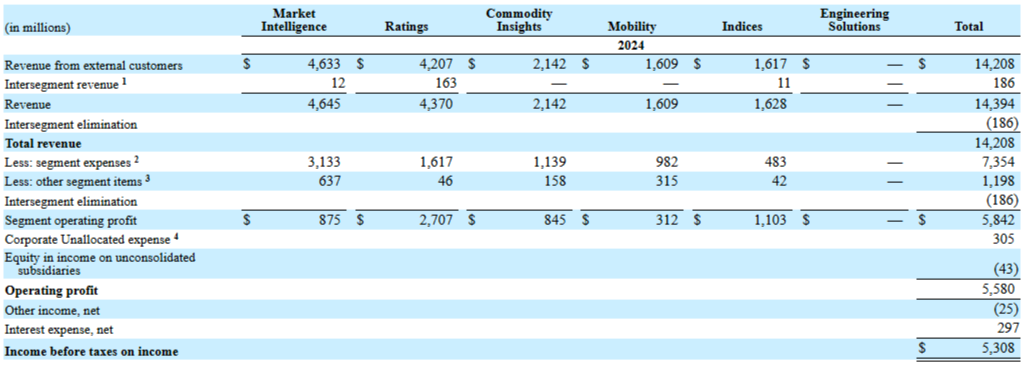

S&P Global is a leading global provider of financial information. It offers data, analytics, benchmarks, and ratings that help companies, investors, and governments make informed decisions. The business is divided into several specialized segments, each tailored to specific information needs and customer groups. In its financial reporting, S&P Global identifies the following areas, which we discuss in more detail below:

- Market Intelligence,

- Ratings,

- Commodity Insights,

- Mobility, and

- Indices.

Source: 10-K Form S&P Global 2024

The Global Market Intelligence segment offers comprehensive financial and economic data, analysis, and software solutions. It is the largest segment, accounting for around 33 percent of revenue. The products are aimed at banks, insurance companies, asset managers, and companies that require accurate, up-to-date, and integrable information. Customers use these services to make strategic decisions, assess risks, and conduct competitive analyses. Market Intelligence platforms such as Capital IQ and S&P Global Desktop also enable data from different sources to be analyzed efficiently and integrated into existing workflows.

The Global Ratings segment, on the other hand, generates revenues of US$4.2 billion, which corresponds to around 30 percent of total revenues. The focus here is on assigning credit ratings to companies, governments, and structured financial products. These ratings also provide investors with a reliable assessment of the creditworthiness and default risk of issuers and financial instruments—something that has been subject to greater scrutiny since the 2009 financial crisis. Nevertheless, investors have regained confidence in S&P Global's analytical expertise. The segment remains one of the best known within the Group and contributes significantly to the transparency and stability of the capital markets. Revenue is generated both from the fees paid by issuers for ratings and from the sale of analyses and related services.

The Commodity Insights division (formerly Platts), on the other hand, provides the energy, raw materials, and chemicals industries with specific price information, market analyses, and benchmark data. Customers use this information for price negotiations, risk management, and the implementation of their market strategies. Since commodity markets are heavily dependent on transparent and objective data, this data is of immense importance for global commodity trading. Revenue here comes mainly from the sale of market data and benchmark prices. In 2024, the segment generated an impressive $2.1 billion in revenue, which corresponded to around 15 percent of total revenue.

The Mobility segment is relatively young and was created from the merger with IHS Markit, which was completed in 2022. It provides data-based solutions for the automotive and transportation industries. Among other things, it offers forecasts on vehicle production, market demand, CO₂ regulation, e-mobility, and supply chain analyses. This specialized information is widely used by automakers, suppliers, governments, and mobility service providers for strategic planning and regulatory compliance.

Finally, with its last segment, Indices, the company operates one of the largest index businesses in the world. Well-known benchmarks include the S&P 500 and the Dow Jones Industrial Average. Such indices serve as the basis for a wide range of investment products, in particular ETFs, structured products, and derivatives. S&P Global earns license fees from asset managers and stock exchanges that use these indices.

The most profitable areas are ratings and indices. They generated operating income of US$2.7 billion and US$1.1 billion, respectively, and together accounted for around 68 percent of consolidated EBIT in 2024. These are also the areas with the strongest growth.

The Engineering Solutions segment, which appeared in the last annual financial statements, was also created through the acquisition of IHS Markit and is aimed at customers in the engineering, aerospace, energy, and manufacturing sectors. This business was sold to financial investor KKR in 2023.

However, one thing is particularly important for investors: S&P Global generates the majority of its revenue through subscription models and licensing, which ensures a high level of revenue stability.

Market and competition

Despite the attractiveness of the market, there are only a handful of companies with which S&P Global has to compete, depending on the segment. A key competitor is Moody’s Corporation. S&P Global Ratings and Moody’s Investors Service are direct rivals, particularly in the area of credit ratings. Both companies are among the world's leading rating agencies, each with a market share of around 40 percent. Moody's is also active in the field of data and analysis products, particularly through its subsidiary Moody's Analytics, which offers services similar to those of S&P Global's Market Intelligence. The third player in the credit rating market is Fitch Ratings.

Another significant competitor is Bloomberg. Founded by Michael Bloomberg, the company is a major player in financial data and news and competes with S&P Global Market Intelligence for institutional clients such as banks, investment companies, and corporations. The legendary Bloomberg terminals offer comprehensive data, analysis, market information, and communication tools and are deeply integrated into the daily work of financial professionals. The situation is similar at Refinitiv, which formerly belonged to Thomson Reuters and is now part of the London Stock Exchange Group. It is also a strong competitor in the areas of market data, trading platforms, and financial analysis. Refinitiv offers comprehensive data feeds, research platforms, and solutions for regulatory reporting. In the index business, S&P Global competes with MSCI and FTSE Russell (also a subsidiary of the London Stock Exchange Group). MSCI is particularly strong in ESG indices and equity benchmarks, which are widely used by institutional investors. FTSE Russell is a major provider of global equity and bond indices and a licensor for numerous exchange-traded products. In the commodity insights segment, S&P Global competes with companies such as Argus Media and ICIS. These companies offer price data, market analysis, and benchmarks for commodities, particularly in the energy, chemicals, and agriculture sectors. They are particularly strong in certain niche markets or regions.

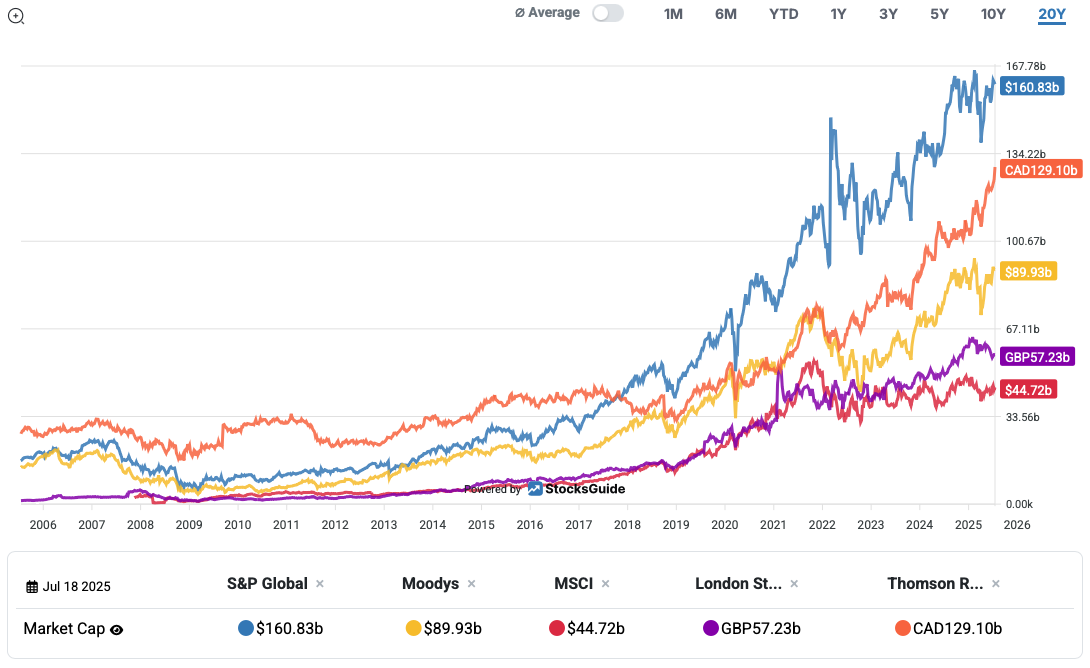

In terms of market capitalization, S&P Global is the clear leader. However, in terms of performance, the London Stock Exchange and MSCI are ahead.

Source: Development of S&P Global's peer group over 20 years

Competition is therefore limited. This can be explained by the deep moats that protect against competition. A dominant position in credit ratings, indices, and financial data, which are deeply integrated into regulatory processes and financial products, is difficult to replicate and break down. However, the market in which S&P Global operates has a number of special features that significantly influence the company's business model and long-term competitiveness.

A key feature is the high barrier to entry mentioned above, which is created by regulatory requirements, strong brand positioning, large amounts of data, and deep integration into customer processes. Over the years, S&P Global has developed into an oligopolist in many areas, particularly in the rating business, where the company is one of the “Big Three” alongside Moody's and Fitch. These positions are extremely difficult to challenge, as they are based on decades of reputation, regulatory acceptance, and extensive historical data.

The market is also characterized by a strong trend toward digitalization and data refinement. Raw data alone has only limited value. What is in demand is structured, linked, and contextualized information that can be embedded in decision-making processes. Here, S&P Global benefits from its ability to integrate data from different sources and convert it into practical analyses, benchmarks, or risk models. As companies increasingly seek solutions that not only provide data but also support the interpretation and decision-making process—for example, through AI-supported analyses, visualizations, or interfaces to internal systems—S&P Global has an advantage.

Another aspect is the high level of regulation and institutional anchoring of many services. Ratings, for example, are anchored in numerous laws and regulatory frameworks, such as Basel III, Solvency II, and US SEC regulations. Benchmark indices such as the S&P 500 and price references in commodity trading also have regulatory or contractually documented relevance. It is precisely this institutional integration that ensures a high degree of stability and creates dependencies on the customer side. In addition, the market is characterized by increasing demand for ESG (environmental, social, governance) data and sustainability-related analyses. Investors, regulatory authorities, and companies have long been calling for transparent and standardized ESG information in order to assess risks and meet regulatory requirements. S&P Global invested in this market at an early stage and can now provide comprehensive ESG ratings, databases, and reporting solutions.

However, the most important argument is that there is a high level of customer loyalty and low price sensitivity, as the products and services are deeply integrated into critical business processes. Switching providers therefore involves high costs and is in some cases unthinkable. At the same time, many customers are willing to pay a premium for high-quality, reliable, and regularly updated information, precisely because they themselves earn a great deal from this valuable data.

Acquisitions by S&P Global

Although S&P Global has delivered solid operational growth, it has also made several strategically significant acquisitions in recent years that have expanded and strengthened its business in the long term. By far the most important transaction was the acquisition of IHS Markit, which was completed in early 2022. With a volume of around US$44 billion, it was the largest acquisition in the company's history. It gave S&P Global access to new business areas, particularly in the fields of commodity data, automotive and engineering solutions, and supply chain analytics. It also created a much broader data and analytics platform. In addition to this major acquisition, the company made a number of smaller acquisitions. A recent example is the acquisition of ORBCOMM's Automatic Identification System (AIS) business, which strengthened the company's expertise in supply chain and maritime data. The acquisitions demonstrate the company's clear strategy: targeted growth through complementary technologies, deeper data expertise, and a stronger market presence in high-growth segments.

The latest S&P Global quarterly figures for March 2025

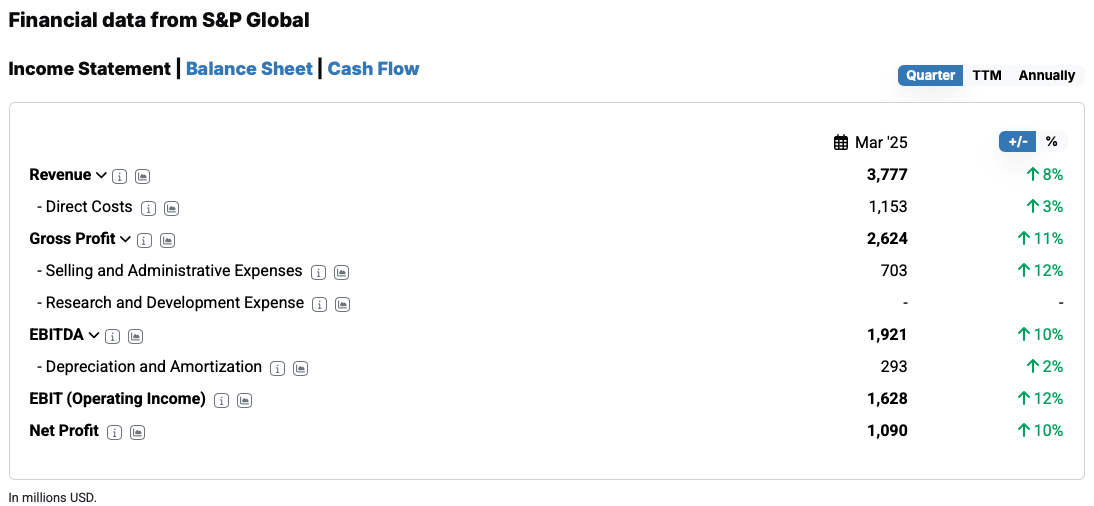

In the first quarter of 2025, S&P Global reported significant revenue and profit growth. Revenue rose by 8% year-on-year to US$3.777 billion. GAAP net income increased disproportionately by 10% to US$1.090 billion, while diluted GAAP earnings per share rose by 12% to US$3.54. On an adjusted basis, net income rose by only 7% to US$1.344 billion and adjusted diluted earnings per share by 9% to US$4.37. The increase in earnings was driven in particular by strong growth in the Ratings and Indices segments, both on a GAAP and adjusted basis.

Source: Financial data from S&P Global

In addition to its financial results, the company announced a strategically significant change with the spin-off of its Mobility division into an independent, publicly traded company. The aim of this measure is to sharpen the company's focus, simplify its operating structure, and maximize the growth potential of both units. The remaining four business segments remain central to S&P Global's long-term strategy. The spin-off is expected to be tax-free for shareholders and to be completed within the next 12 to 18 months. The new Mobility company will operate independently and pursue a targeted growth strategy in the automotive sector. In addition, the planned sale of the 50% stake in the joint venture OSTTRA was announced earlier. OSTTRA is a provider of post-trade solutions for global financial markets, formed in 2021 through the merger of the post-trade activities of CME Group with the MarkitServ business of IHS. The latter was acquired by S&P Global in 2022. The two owners expect the transaction to generate total proceeds of US$3.1 billion, which will be distributed to the two partners in accordance with their shareholdings.

S&P Global stock forecast for 2025

The outlook for 2025 as a whole is based on solid data. For example, growth of between 4 and 6 percent is expected, with an operating margin of between 42.3 and 43.5 percent. Adjusted for extraordinary effects, it is even 6 percentage points higher. At the end of the year, EPS in accordance with GAAP is expected to be between 14.60 and 15.10. Adjusted, it could even be a few US dollars more. The company's own estimates are between 16.75 and 17.25 US dollars per share.

Overall, however, the annual forecast for 2025 paints a slightly weaker picture than the previous plan. Operating cash flow after deducting investments and distributions to minority shareholders is now expected to be between US$5.4 billion and US$5.6 billion, which is below the previous expectation of around US$5.9 billion. Adjusted free cash flow is also slightly below the previous forecast of around US$6.0 billion at US$5.6 to US$5.8 billion. The reduction is primarily due to changes in assumptions regarding tax payments, net income, and working capital. The forecast for revenue growth was also adjusted downward by one percentage point, reflecting slightly lower expectations in the Ratings and Indices segments. At the same time, however, the company is raising its forecast for GAAP operating profit, primarily due to the expected gain from the sale of the OSTTRA joint venture. By contrast, the adjusted EPS forecast was given a wider range.

This reflects uncertainties in rating revenues as well as timing fluctuations in expenses and strategic investments over the course of the year. There is positive news for dividend investors: For the full year 2025, S&P Global plans to return approximately 85% of adjusted free cash flow to shareholders in the form of dividends and stock repurchases.

Management has approved a quarterly dividend of US$0.96, and it intends to carry out additional accelerated stock buybacks totaling US$650 million in the near future.

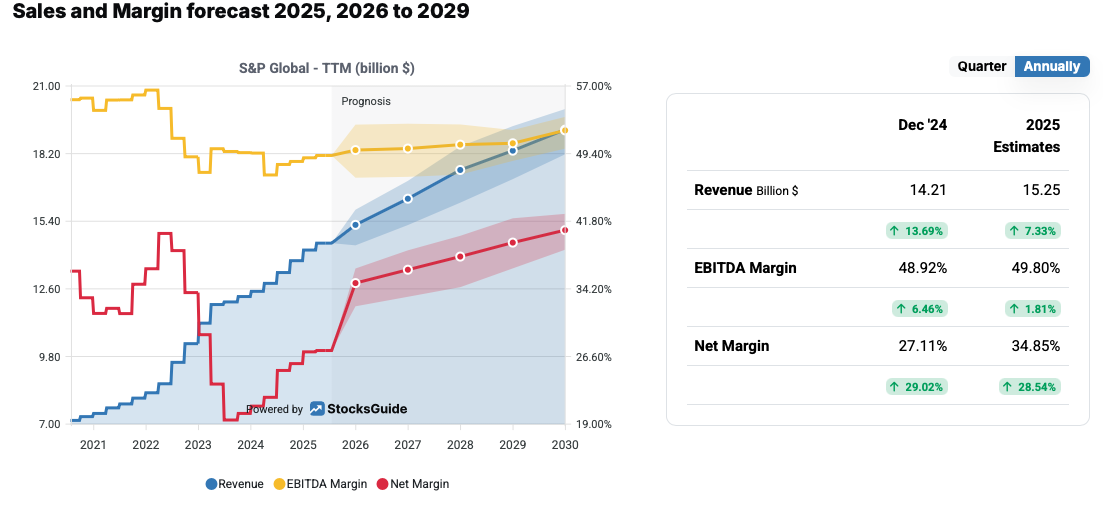

Source: Analyst forecasts for S&P Global's revenue

Analysts' revenue forecasts for S&P Global point to continued but moderately flattening growth in the coming years. For 2025, for example, revenue of around US$15.2 billion is expected, representing an increase of just over 7% on the previous year. In the years that follow, growth is expected to continue at a similar level, with the pace slowing slightly from 2028 onwards. Net margins could improve steadily until 2030.

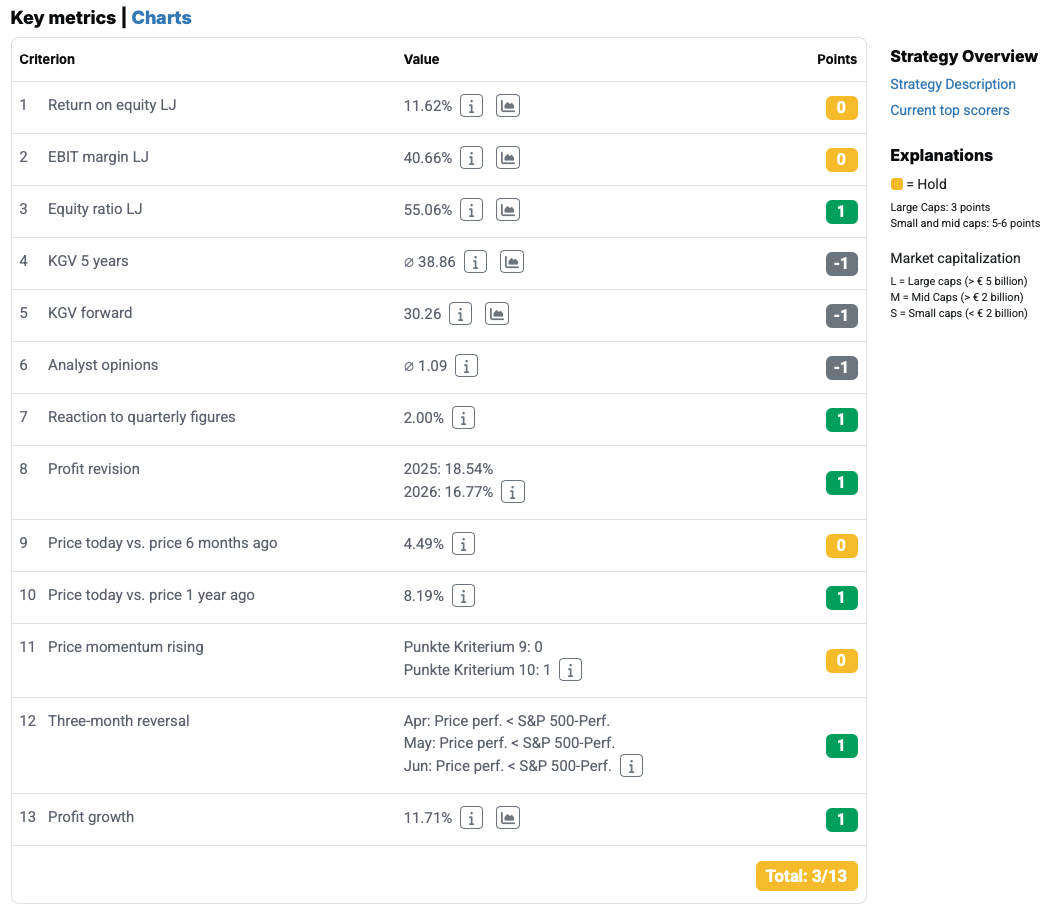

Key figures for S&P Global stock from the Levermann analysis

The Levermann analysis for S&P Global stock paints a balanced picture with a slightly positive trend. The financial services provider's shares score points with a strong equity ratio of over 55 percent. The positive stock price performance over the last six and twelve months and the good market reaction to the latest quarterly figures also speak in favor of the stock. In addition, analysts' significant upward revisions to earnings are providing tailwinds. The same applies to earnings growth, which is at a respectable level of just under 12 percent. With 3 out of a possible 13 points, a solid basis has been achieved. The stock is regularly top scorer in the Levermann strategy.

Source: S&P Global Levermann analysis

But there are also negative aspects: both the average P/E ratio for the last five years and the expected P/E ratio are at a high level. The very optimistic analyst estimates also lead to point deductions, as they are interpreted as a contraindicator in the analysis. And even though operating profitability, measured in terms of return on equity and EBIT margin, is high, it does not exceed the required thresholds in the Levermann analysis.

The technical indicators paint a generally positive picture. Only the long-term price performance received full marks. The stock also failed to score points for price momentum. Fortunately, no points were deducted here either. On the other hand, the three-month reversal is positive again. In each of the last three months, the stock outperformed the S&P 500 benchmark index.

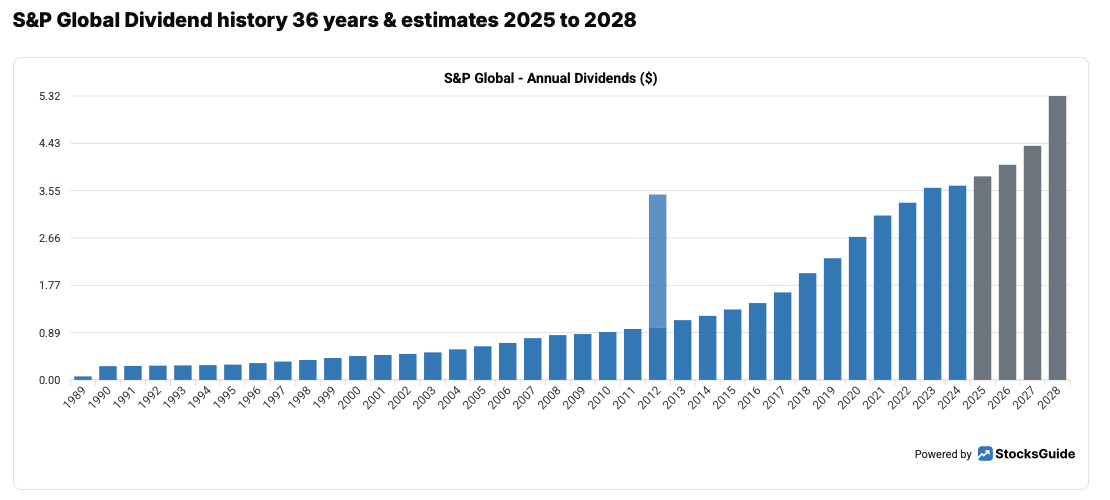

Source: S&P Global Dividend

Unfortunately, the stock is not a top performer in terms of dividend strategy, but there are some arguments in favor of the stock with regard to distributions. S&P Global's dividend is less impressive in terms of its size than in terms of its quality and reliability. With a current dividend yield of just 0.7 percent, the distribution yield is well below the market average. It is also rather low in a historical comparison of the last ten years, at 0.9 percent. However, the strong dividend growth is noteworthy. Over the last five years, the payout has risen by an average of just under 10 percent per year – clear evidence of the company's sustainable earnings power and the management's willingness to share the company's success with shareholders.

Valuation of S&P Global stock

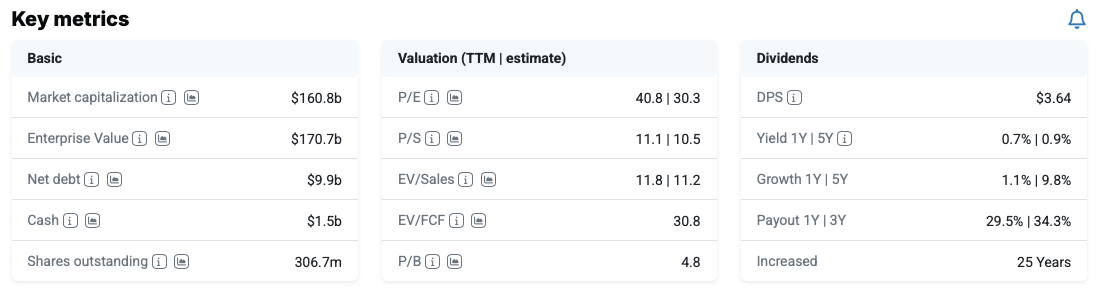

The valuation of S&P Global stock can definitely be described as ambitious. The expected P/E ratio of over 30 and the double-digit revenue multiple show that investors will have to pay a quality premium for this dividend aristocrat.

Source: S&P Global key metrics

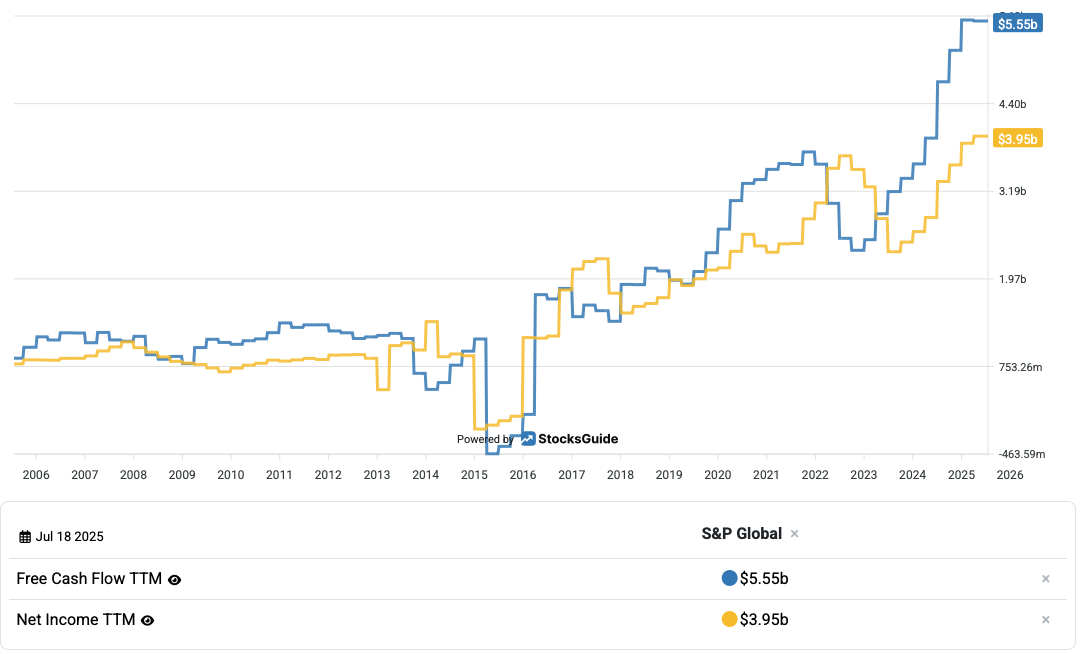

But there is plenty of quality here. For example, the company achieves an EBIT margin of over 40 percent. Free cash flows are also booming, recently reaching a record high of US$5.6 billion on a trailing month basis. Incidentally, this figure is regularly higher than net profit. S&P Global therefore generates more money than it reports as profit.

Source: Development of free cash flow and net income at S&P Global

The high valuation is also reflected in the dividend. A yield of well below one percent—both in the short and long term—does not exactly point to a high-yield investment.

Source: dividend analysis

However, this must be put into perspective, as the payout ratio is low. At the same time, dividends are rising steadily at a rapid pace. Growth over the last five years has been almost double-digit. Dividends have risen without exception for 38 years.

However, the dividend score just missed out on top spot, mainly due to the high valuation and low dividend yield. Looking back, however, the stock has always been highly valued.

Conclusion on S&P Global stock

S&P Global is an exceptionally well-positioned company with a clearly structured, largely recurring business model that is deeply embedded in the infrastructure of global financial and commodity markets. The company's products are indispensable for many market participants, whether for assessing credit risks, designing financial products, evaluating macroeconomic developments or meeting regulatory requirements.

Despite short-term weaknesses in individual segments such as ratings, the long-term growth outlook remains intact, supported by structural trends such as rising demand for reliable financial and sustainability data, the expansion of passive investment strategies, and the increasing digitalization and automation of decision-making processes. But that's not all: with disciplined capital allocation, high cash flows, and targeted strategic measures such as the upcoming spin-off of the Mobility business, management is demonstrating that it consistently prioritizes value enhancement. From a fundamental perspective, the stock therefore remains a potentially attractive investment for long-term investors who value stability, pricing power, and sustainable growth.

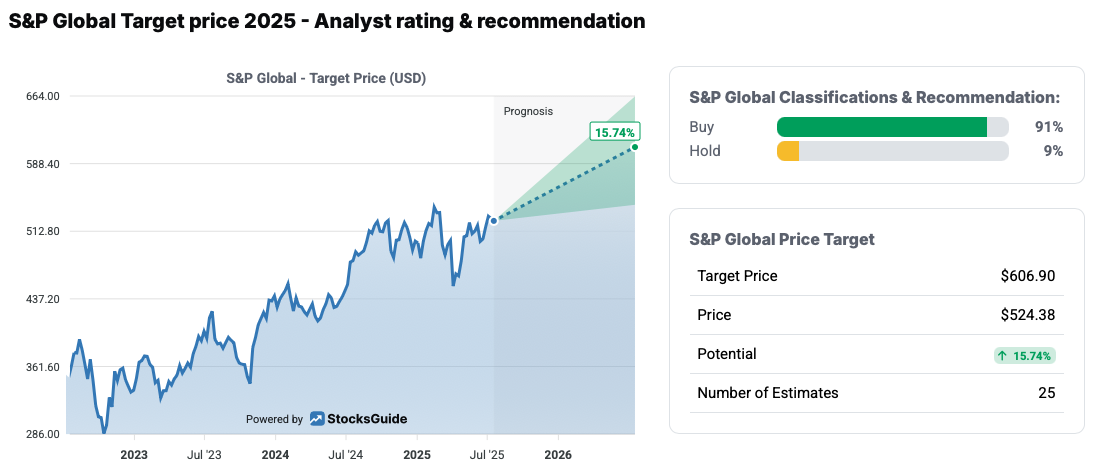

Source: S&P Global target price

Analysts are also euphoric, as their ratings for the stock show. Almost all (91 percent) see the stock as a buy, with only three and nine percent recommending it as a hold. Despite its high valuation, the growth, which is largely predictable, appears to be convincing. The stock is expected to rise by almost 16 percent over the next year.

The author and/or persons or companies associated with StocksGuide own or may own shares of S&P Global. This article represents an expression of opinion and does not constitute investment advice. Please note the legal information.