There are companies that are underestimated at first glance. In my opinion, Talanx (ISIN: DE000TLX1005) is one of them. The Hanover-based insurance group, operating under the HDI brand, is majority-owned by the insurance association HDI Haftpflichtverband der Deutschen Industrie V.a.G. and remains an insider tip for many retail investors, even though it is the third-largest German insurer after Allianz and Munich Re. Its majority-owned subsidiary, Hannover Re, is better known. But anyone familiar with the figures from recent years quickly understands the growing interest among investors: Talanx delivers record results year after year, continuously increases its dividend, and regularly exceeds its own forecasts. Given the ongoing megatrends, this could continue for several more years. The group’s equity story is fundamentally based on three pillars: diversification, cost leadership, and structural growth in an industry with tailwinds. Megatrends in particular play right into Talanx’s hands. For instance, climate change is increasing demand for natural disaster coverage—in both the primary and reinsurance sectors. The increasing digitalization of the economy is creating new risks in the area of cyber insurance—a growth market that Talanx is actively addressing. And the insurance industry has also skillfully leveraged the inflation of recent years to adjust premiums. Not least, higher interest rates open up better opportunities for insurers to reinvest capital reserves. This is a structural profit driver that has been in effect since 2022 and should continue to be effective beyond 2026.

Source: Stock price

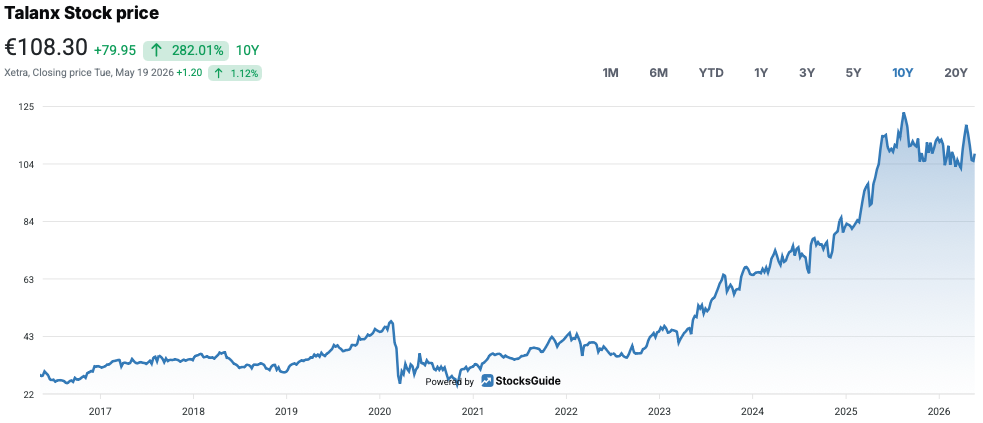

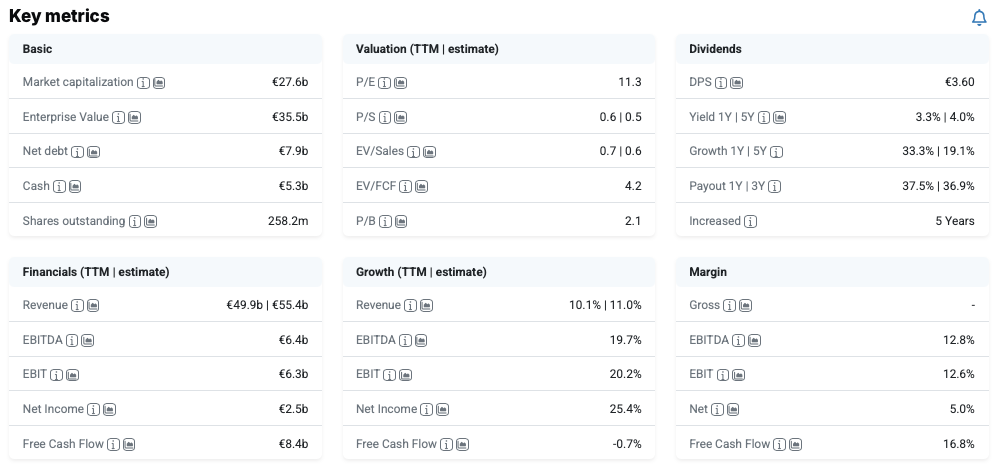

This positive trend is also reflected on the stock market. Over the past 20 years, Talanx shares have risen by an impressive 470 percent. At the beginning of May 2026, they were trading at around 108 euros. But it hasn’t always been an upward trend. The recent weakness, in particular, gives cause for concern. The trigger for the weakness was global market turbulence surrounding interest rate expectations and geopolitical uncertainties in the spring of 2025. The subsequent recovery, however, was driven by record-breaking half-year results and an upward revision of the annual forecast. Since its annual high, however, the stock has fallen back by about 8 percent—a move that investors might view as a buying opportunity. This is supported, at least, by the attractive valuation with a P/E ratio of 11. The initial yield stands at 3.4 percent, and the stock is a top performer in the dividend analysis. Yet analysts are divided. The following Talanx stock analysis will examine why they are skeptical.

Company Profile – Germany’s third-largest insurer with international ambitions

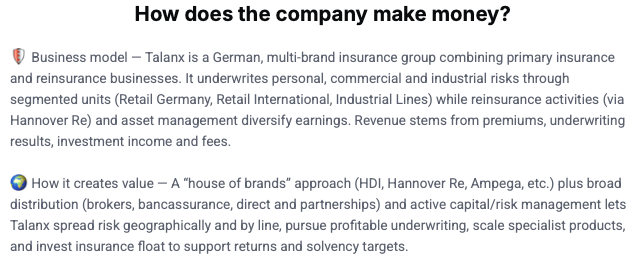

Talanx is not a traditional primary insurer. The group sees itself as a multi-brand provider that combines primary and reinsurance under one roof. It is precisely this combination that constitutes a significant competitive advantage.

Source: How does the company make money

The Talanx Group holds approximately 50.2 percent of the shares in the publicly traded Hannover Re. This makes Talanx one of the few insurance groups worldwide that operates profitably in the areas of retail business, the large-corporate industrial segment, and reinsurance. However, with a market capitalization of approximately €33 billion, it lags far behind Allianz.

The group’s investment volume (assets under management) most recently stood at around €144 billion. With insurance premiums of €48.9 billion and an EBIT of €5.3 billion in fiscal year 2025, Talanx is nonetheless one of Europe’s leading insurers. Talanx operates its insurance business in over 150 countries with a focus on B2B insurance.

Reinsurance is the backbone of the group

The largest segment is property and casualty reinsurance (P/C Reinsurance). This segment accounts for 40 percent of revenue. Operationally, it is managed by Hannover Re, which is also publicly traded. The second-largest segment, accounting for 20 percent, is Retail, followed by Life/Health Reinsurance and Corporate & Specialty, each with a 16 percent share of revenue.

Germany is the largest market

Geographically, 14 percent of insurance premiums are generated in Germany. However, the highest premium income by country is generated in the U.S., at 26 percent. In third place is the rest of Europe with 13 percent, followed by Latin America with 12 percent and the Asia/Australia region with 11 percent.

Economic Moat

Since Talanx operates in a volume market, differentiation through specific unique selling propositions is crucial, and the Group possesses several competitive advantages that make it difficult for competitors to imitate. A major barrier to entry is the high credit rating requirements in the industrial insurance business, as large clients mandate credit ratings that can be met almost exclusively by established groups. Additionally, the decentralized organizational structure, featuring strong local brands such as HDI, Warta, and HDI Seguros, fosters a level of customer proximity and brand loyalty that centralized competitors can hardly replicate. Another unique selling point is the stake in Hannover Re, which provides unique internal reinsurance access. This market position is rounded out by high efficiency, as the company rates itself as a cost leader in 93 percent of its units. This brings us to the opportunities and risks.

Source: What are the key opportunities and risks?

Opportunities

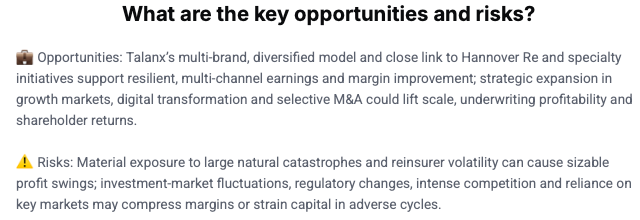

A key growth driver is the structural premium growth in the global insurance market. Rising asset values, increasing regulation, and greater risk awareness are driving both private and commercial customers to seek more insurance coverage. In the commercial insurance segment in particular, Talanx can benefit from risk-adequate pricing, as margins in this environment remain quite stable and are even on the rise. Growth is particularly dynamic in Latin America. Through the integration of the companies acquired from Liberty Mutual, Talanx gains access to high-growth markets such as Brazil and Mexico. These regions are growing structurally faster than Europe, meaning that the international retail business can become a key earnings driver in the medium term. Another market with strong growth potential is cyber insurance. Through HDI Global, the Group is well-positioned in this area, as existing industrial clients can be targeted directly (upselling or cross-selling). Given the increasing digitalization and the growing threat landscape, double-digit market growth is realistic here in the long term. The interest rate environment also plays into Talanx’s hands. Higher interest rates improve investment income, as premium reserves can be reinvested at better terms. This strengthens profitability, regardless of the insurance business itself. However, risks remain with each individual point.

Risks

The single greatest risk for an insurer is, of course, the risk of major claims. Natural disasters, pandemics, or industrial accidents can quickly exceed planned claims budgets and thus significantly weigh on earnings. This volatility is inherent in the insurance business and difficult to fully control. Added to this are currency risks stemming from the strong international presence. Fluctuations in currencies such as the Brazilian real or the Mexican peso can quickly offset operational successes when consolidated in euros. Regulatory interventions also pose a risk. Changes to regulations such as Solvency II or national price regulations can increase capital requirements or directly limit margins. While we previously viewed higher interest rates as an opportunity, the capital markets unfortunately also represent an extremely significant risk. Severe crashes or crises on the stock market can influence results more strongly than the operating business itself. Finally, the ownership structure is another structural factor to keep in mind, as the majority of Talanx shares are held by HDI V.a.G. The relatively low free float makes the stock illiquid and deters institutional investors. This puts downward pressure on the valuation in the long term and somewhat hampers price momentum.

Talanx’s latest quarterly figures from May 2026

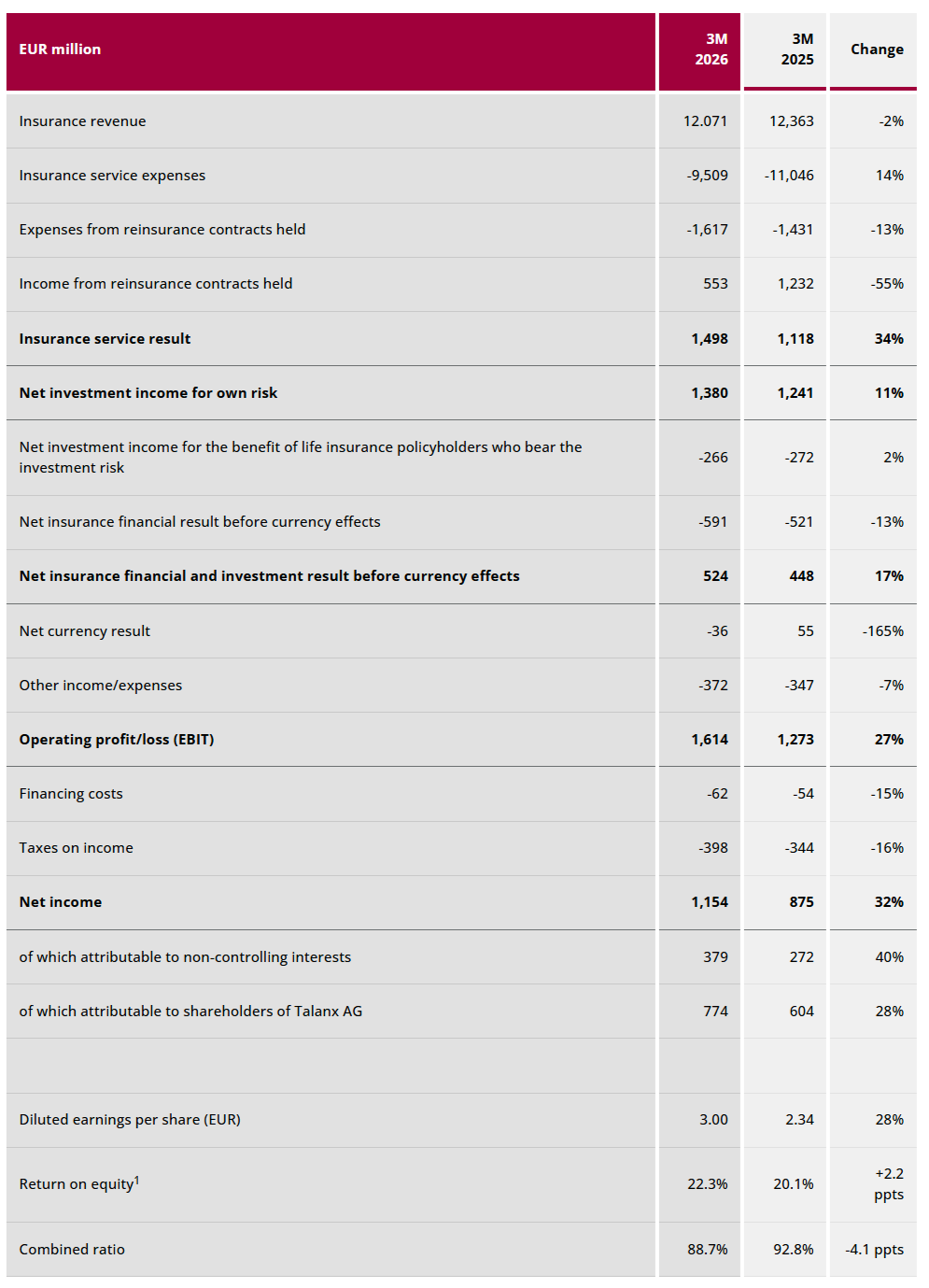

Talanx’s quarterly figures for the first quarter of 2026 show an exceptionally strong start to the year. Although insurance revenue fell by 2 percent to 12.1 billion euros, consolidated net income rose by a further 28 percent compared to the same quarter of the previous year, reaching a record 774 million euros.

Source: Financial data Talanx

It is noteworthy that this growth is based on a broad operational foundation, with nearly all business segments contributing to higher earnings. At the same time, the Group was able to further increase its profitability. Operating profit (EBIT) rose by 27 percent to 1.6 billion euros (margin: 13 percent), while the return on equity increased to 22 percent. The combined ratio also improved to just under 89 percent, indicating a currently highly profitable insurance business. A key reason for this positive development was the significantly lower burden from major losses compared to the previous year. While high losses from the wildfires in California still weighed on earnings in the first quarter of 2025, major losses in 2026 were well below the budgeted amount. The Group also retains a safety buffer of approximately 400 million euros within the major loss budget after the first quarter, which increases the likelihood of achieving the reaffirmed annual targets.

Reinsurance performed particularly strongly, once again serving as the Group’s most important earnings driver. The segment’s profit contribution rose by 50 percent to 359 million euros. The business benefited primarily from lower natural catastrophe losses and continued attractive market prices. The combined ratio in property and casualty reinsurance improved significantly to 83.6 percent. The international retail business also continued on its growth trajectory. Talanx was able to significantly increase premium income and profits, particularly in Poland, Brazil, Mexico, and Turkey. This development once again confirms the strategic importance of international expansion, particularly in higher-growth markets outside Western Europe. The Retail International segment is increasingly becoming a key revenue pillar for the Group. In the German retail business, however, revenues declined slightly. This is attributable, among other things, to the expiration of the cooperation with TARGOBANK. Nevertheless, profits were also significantly increased here, as improvements in the existing business and efficiency measures more than offset the negative impacts. Furthermore, the Group’s capital base remains exceptionally robust. The Solvency II ratio stood at 249 percent at the end of March 2026, signaling substantial financial reserves. In addition, the Hanover-based Group strengthened its loss reserves, making it more resilient to future major losses.

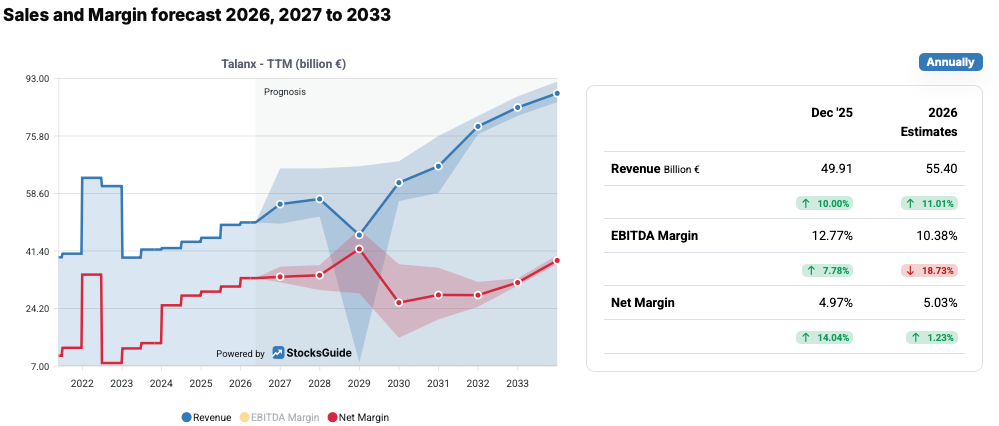

Talanx Stock Forecast 2026

For the full year 2026, Talanx is sticking to its forecast of consolidated earnings of around 2.7 billion euros. This would initially represent an increase of around 9 percent compared to the already record-high prior-year result of 2.5 billion euros. This would mean that Talanx would achieve the profit target originally set for 2027 as early as this year, underscoring the Group’s operational strength and positive sentiment. However, the guidance is subject to three caveats: As with all insurers, major claims must not exceed the budget allocated for them. Furthermore, the capital markets must not experience significant turbulence, and there must be no major currency fluctuations. A return on equity of 19 percent is forecast for the end of the year.

Source: Sales and Margin forecast

Analysts consider the Talanx Group’s forecasts to be conservative. They project revenue of €55.4 billion and net income of €2.8 billion for 2026. According to analysts, revenue is expected to grow in the mid-single digits over the medium term. Earnings per share could even see significant double-digit growth in some cases.

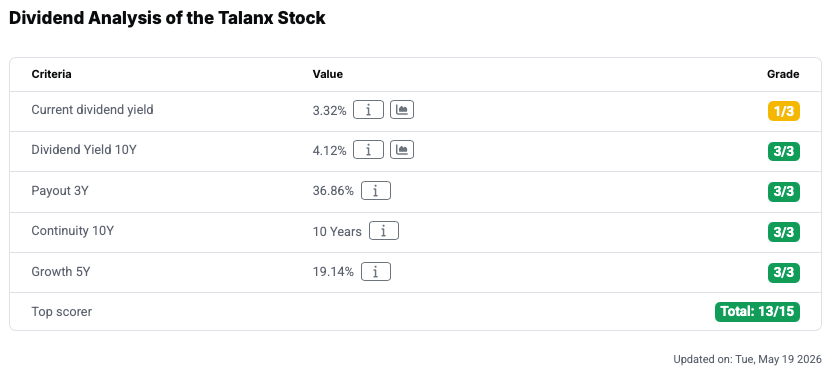

Key metrics for the Talanx stock from the dividend analysis

With 13 out of a possible 15 points, the Talanx stock clearly belongs in the category of top dividend performers. This initially points to a solid and shareholder-friendly dividend policy. However, there are weaknesses here as well.

Source: Dividend Analysis

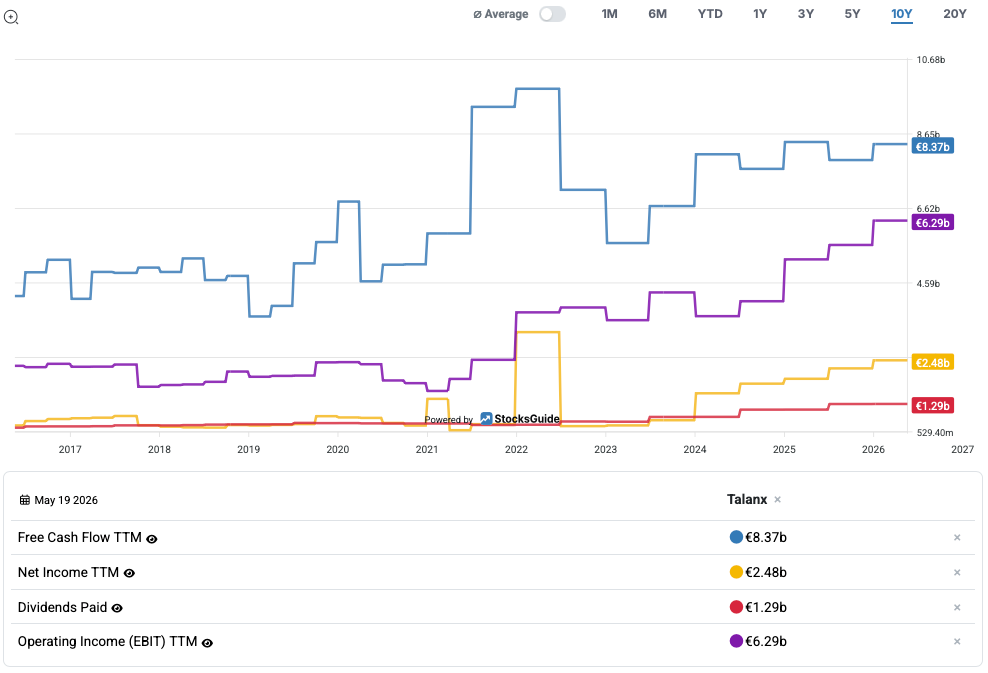

The current dividend yield of 3.4 percent is decent, but not exceptionally high. There are reasons why it is also below the 10-year average of 4.1 percent. The stock price has risen sharply recently, while the dividend has not kept pace in relative terms. For new investors, this is a somewhat neutral to slightly negative factor. The payout ratio of around 37 percent, on the other hand, is very impressive. It falls within a conservative range, which is typical for solid insurers. Above all, it should be viewed positively, as free cash flows are significantly higher.

Source: StocksGuide Charts

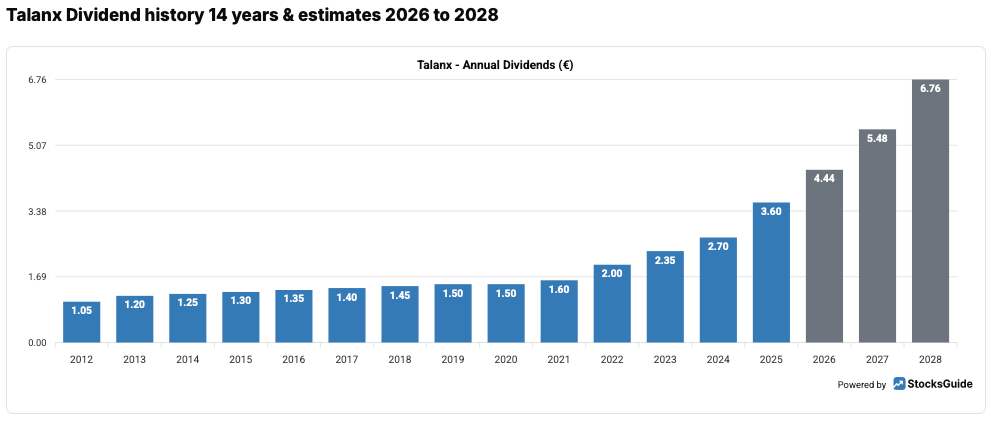

This means that the dividend is well covered by profits while simultaneously leaving room for growth, reserves, and periods of crisis. A true indicator of quality is the consistency of dividend payments over a ten-year period. Continuous dividend payments for a decade – including periods of crisis such as pandemics or natural disasters – demonstrate a robust business model and disciplined management.

Source: Dividend history

Particularly noteworthy is the dividend growth of over 19 percent in the last five years. This above-average dividend growth demonstrates that Talanx not only pays a stable dividend but also significantly shares its profit growth with its shareholders. Here, they easily outpace inflation. Looking ahead, dividend growth could gain even more momentum. The dividend for 2028 is already estimated at €6.76, representing an increase of 87 percent compared to fiscal year 2025.

Valuation of the Talanx

Based on profit estimates for 2026, the Talanx share appears moderately valued with a price-to-earnings ratio of around 11. Compared to the European insurance sector, which typically trades at P/E ratios of 11 to 15, Talanx is at the lower end of the range – even though the company achieves an above-average return on equity and records stronger profit growth than most of its competitors.

Source: Key metrics

One explanation for the favorable valuation is the low free float of around 23 percent. This deters large institutional investors and tends to keep the share price down. Furthermore, the legal form of a mutual insurance association is less common internationally. On the other hand, the majority shareholder structure via HDI V.a.G. ensures stability, eliminates takeover risks, and promotes a long-term planning horizon.

Source: StocksGuide Charts

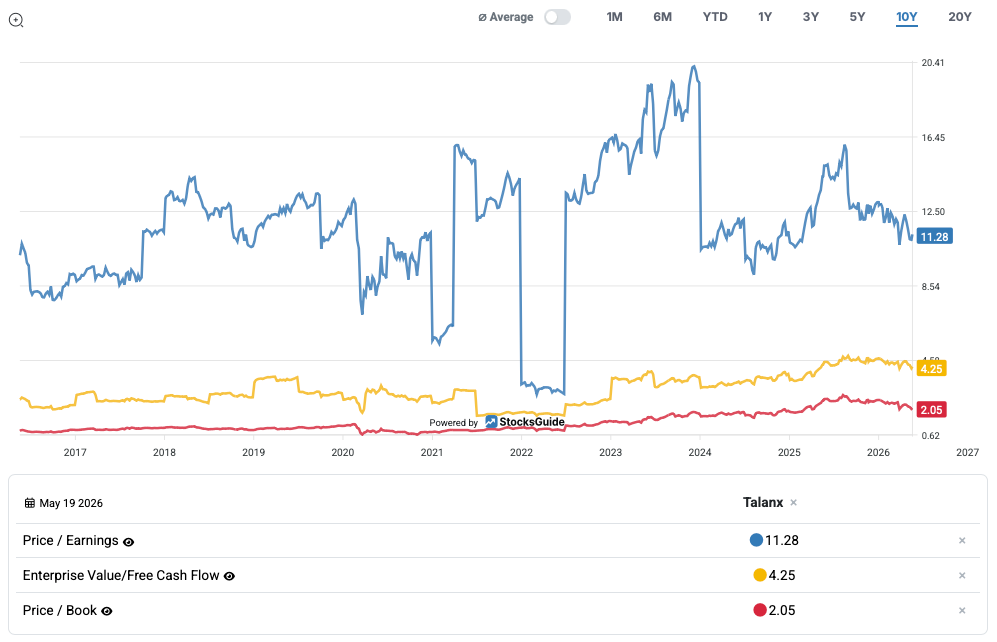

Looking at the historical development of the P/E ratio and EV/FCF, the P/E ratio is almost in line with the average of the last ten years. However, the current free cash flow value is 40 percent higher, and the price-to-book ratio is even 57 percent higher. Therefore, Talanx is not a classic value stock with low fundamentals in a historical context, but rather a quality growth stock that impresses with its market positioning, growth, and consistent exceeding of its own targets.

Conclusion on Talanx stock

The equity story of Talanx stock is simple and compelling: a diversified business model encompassing primary, industrial, and reinsurance; structural growth in emerging markets; a consistent strategy for achieving cost leadership; and a dividend policy that reliably shares earnings growth with shareholders. The fact that Talanx appears poised to achieve its own medium-term targets for 2027 as early as 2026 demonstrates operational strength. And further profitable growth should be expected in the medium term as well. The result for the first quarter of 2026, at €774 million, was around 15 percent above the analyst consensus. This signals that the upward momentum is continuing. The valuation discount compared to its European insurance peers, coupled with above-average profit growth, could therefore offer an attractive risk-reward profile. Of course, significant risks such as major losses from natural disasters, currency fluctuations, or limited trading liquidity due to the small free float are not considered in this calculation. The same applies to potentially more intense competition in the future. Nevertheless, Talanx shares could be appealing to income-oriented investors with a long-term horizon who value strong fundamentals and solid dividend growth.

Source: Target price

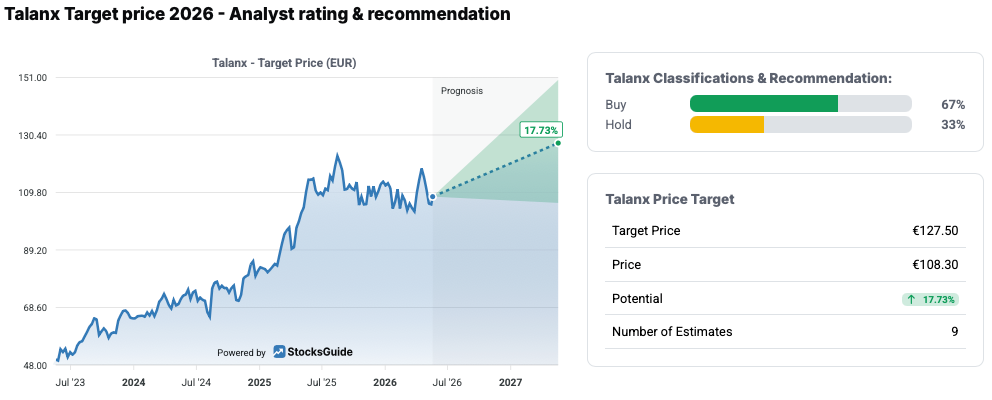

Analysts see an average price target of €127.50. This corresponds to a potential price increase of 20.9 percent within one year. 67 percent of analysts recommend buying, while a third advise holding. Those who still consider the stock too expensive can set an alert in aktien.guide. A marker at the historical average dividend yield of 4.2 percent seems plausible.

The author and/or persons or companies associated with StocksGuide own or may own shares of Talanx. This article represents an expression of opinion and does not constitute investment advice. Please note the legal information.