Table of Contents

- Company profile - Premium chocolate manufacturer

- The latest Lindt quarterly figures for December 2024

- Lindt stock forecast for 2025

- Evaluation of Lindt stock

Chocolate is always a good choice. It symbolizes reward, love, and comfort. Almost everyone enjoys it, and its high fat and sugar content makes it somewhat addictive. Lindt & Sprüngli (ISIN: CH0010570759) operates in this market, primarily in the premium chocolate segment. The Swiss company benefits from its strong brand, high pricing power, and proven business model with a global presence. Shareholders have also benefited from above-average returns for many years.

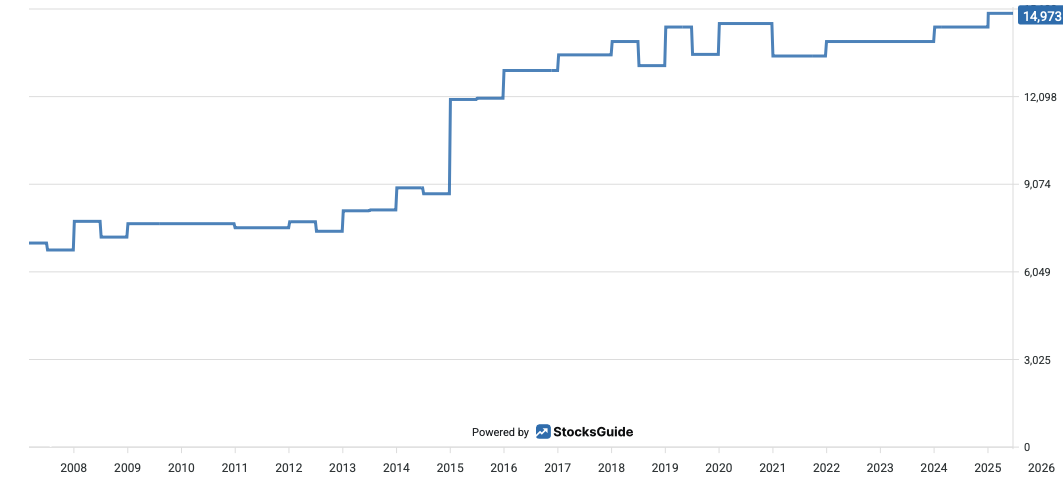

Source: Lindt stock price

However, there are also challenges: increasingly fierce competition and high inflation are contributing to consumer restraint. Added to this are high raw material prices, on which Lindt is heavily dependent. Despite the challenging economic environment, the company has achieved relatively good organic growth rates in recent years, expanded its market share, and steadily improved its profitability. This puts it in a better position than its competitors.

The stock is also particularly attractive due to its defensive orientation, as chocolate consumption remains relatively stable even in weaker economic phases, which gives the stock a certain degree of crisis resistance. The clear strategic focus on further international growth, coupled with innovative products and successful direct sales through its own stores, currently makes Lindt & Sprüngli a potentially exciting investment in the consumer goods sector – were it not for its high valuation. Could the stock still be a buy? The following Lindt stock analysis reveals more.

Company profile - Premium chocolate manufacturer

Lindt & Sprüngli's business model is based on the manufacture and worldwide distribution of premium chocolate products. The Swiss company focuses on complete control of the entire value chain – from the selection of cocoa beans to production and sales. In economics, this is referred to as vertical integration. It enables the company to maintain the highest quality standards and ensure the uniqueness of its products. Another key component of the business model is the strong brand positioning. Lindt is internationally synonymous with luxury, craftsmanship, and tradition in chocolate manufacturing. This is precisely what sets it apart from its competitors, who often focus on mass markets. The Lindt brand is built and maintained through extensive marketing, emotional advertising campaigns, and iconic products such as the Gold Bunny at Easter.

In addition to traditional retail distribution, Lindt operates a growing network of its own boutiques and flagship stores. There were exactly 568 of these at the end of 2024. These outlets enable direct customer loyalty, offer an exclusive brand experience, and help to collect valuable data on consumer behavior.

Source: Lindt development of employees since 2007

However, the chocolate empire is also pursuing a strategy of internationalization and expansion, particularly in high-growth markets such as Asia and North America. Seasonal products and gift items also play an important role in annual business and contribute significantly to sales. Let's take a closer look at these unique characteristics of the chocolate market.

Market and competition

The chocolate market, especially the premium segment, has a few special features. One key thing is how strongly people feel about the product. Chocolate is not only perceived as a foodstuff, but also as a luxury item and a symbol of reward, love, or comfort. This creates a high level of brand loyalty, especially for established brands with a strong image, as is the case with Lindt. However, there is also a strong seasonal factor. Sales are highly concentrated in certain times of the year, particularly around Easter and Christmas. The explanation is that demand for gift items and high-quality packaging rises sharply during these periods. However, this means that marketing and logistics have to be managed in a cyclical manner. In addition, there is increasing premiumization of the market. More and more consumers are willing to spend more money on high-quality, sustainable, and fairly produced chocolate. This is exactly what a supplier like Lindt, which is strongly positioned in these segments, benefits from. Sustainability and transparency in the supply chain are also becoming increasingly important. Consumers today are increasingly interested in the social and environmental conditions under which cocoa is grown and processed. The market is also highly fragmented internationally, with major differences in taste, consumption habits, and purchasing power. While per capita consumption is high in Europe, there is still significant growth potential in many Asian markets. However, this requires cultural and logistical adjustments, as chocolate melts more quickly in hot regions and people have different eating habits.

In terms of sales, there is a clear European focus. Around half of sales are generated in Europe, with North America accounting for just under 40 percent. The rest of the world accounts for 13 percent of sales. However, the latter area recorded the strongest growth of 10 percent in fiscal year 2024. The European region grew at a similar rate of 9.5 percent. In North America, however, organic growth was only 5 percent. Let's move on to the competition.

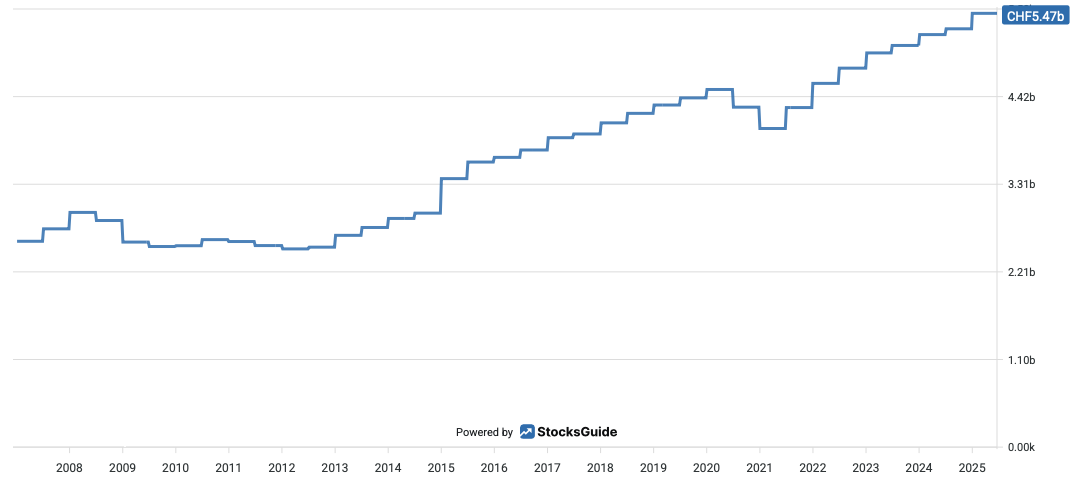

Source: Revenue TTM development since 2007

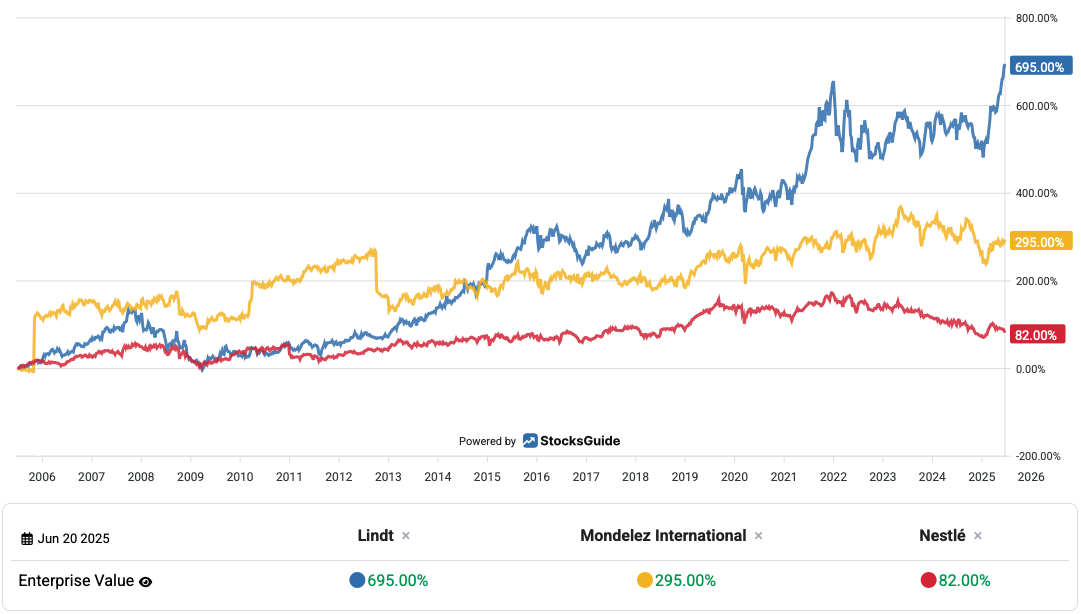

Lindt & Sprüngli's biggest competitors in the global chocolate market are primarily large, internationally active companies with broad brand portfolios and a strong market presence. They differ in their strategic orientation – for example, mass market vs. premium segment – but are increasingly overlapping as many suppliers are moving into the premium segment. The most significant competitors include Mondelez, Mars, Nestlé and Ferrero. Mondelez International owns well-known brands such as Milka, Toblerone and Côte d'Or. Unlike Lindt, Mondelez is more active in the mass market, but is increasingly trying to develop premium products. Mars owns brands such as Mars, Snickers, M&M's and Dove (known as Galaxy in Europe). The Americans are particularly strong in the impulse consumption products and convenience segments. Although the focus is less on premium quality, their market presence is significant, as demonstrated by sales in the double-digit billion range. The situation is similar at Nestlé, the world's largest food company. With brands such as KitKat, Smarties and Cailler, Nestlé also has a broad international presence. In some markets, such as Switzerland, Nestlé also competes directly with Lindt in the premium segment. Ferrero from Italy should not be forgotten. The company is known for brands such as Ferrero Rocher, Raffaello, Mon Chéri, and Kinder. Its surprise eggs have cult status. Ferrero combines mass appeal with a certain premium image, especially for seasonal and gift products. The Ferrero Rocher brand can be seen as a direct competitor to Lindt chocolates simply because of its shape. Looking at slightly smaller competitors in the premium segment, we come across the name Godiva. Originally, this was a Belgian chocolatier. However, the company is now owned by the Turkish group Yildiz Holding. Similar to Lindt, it focuses on elegant packaging, gifts, and an international network of stores.

Source: Enterprise value development of Lindt vs. Mondelez vs. Nestlé over the last 20 years

In addition to these global corporations, there are numerous other regional suppliers and luxury brands such as Neuhaus, Leonidas, Valrhona, and Läderach, which are strong competitors in certain markets or in the high-end segment. However, none of them can match Lindt in terms of sales.

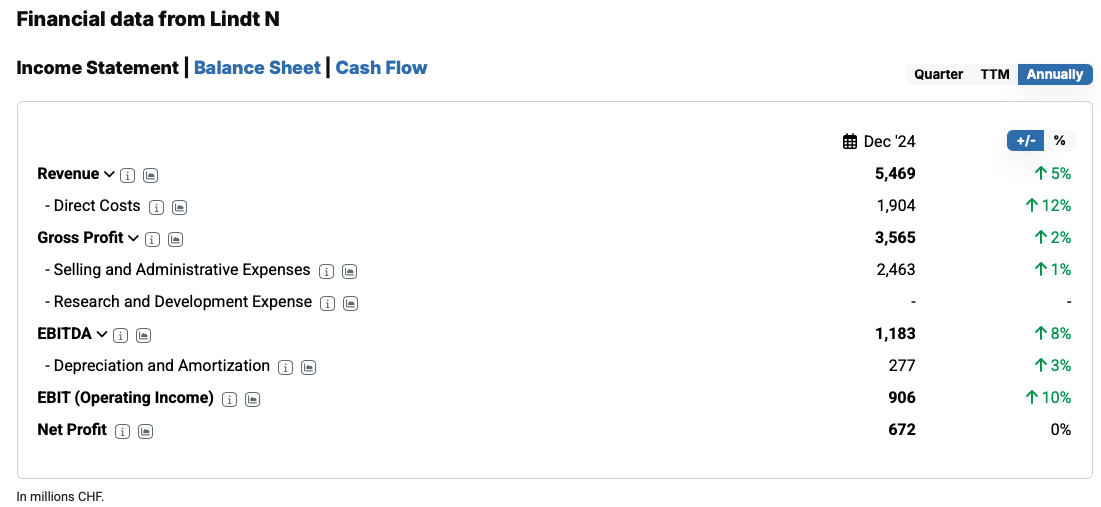

The latest Lindt quarterly figures for December 2024

Despite a challenging economic environment, Lindt & Sprüngli achieved strong organic growth of 7.8 percent in 2024. This growth was driven primarily by positive sales volume and product mix developments, as well as price adjustments to offset sharp increases in cocoa prices. All three regions – Europe, North America and the rest of the world – contributed to growth, with Europe standing out in particular with organic sales growth of 9.5 percent. Sales rose by 5 percent to 5.5 billion Swiss francs, while operating profit increased by 10 percent to 906 million Swiss francs.

Source: Financial data from Lindt & Sprüngli

Despite high raw material prices and subdued consumer sentiment, Lindt managed to gain global market share in both sales and volume. The Global Retail division was particularly successful. The 568 company-owned stores and 21 online shops recorded sales growth of 16.7 percent. This development underscores the increasing importance of direct sales for the brand. The company also secured further market share in the US and Canada. Double-digit growth was achieved in Asia and Latin America, particularly in countries such as Brazil, Japan, and China. Strong momentum also came from established products such as Lindor and Excellence, which were in high demand worldwide. The range was expanded with new flavors and limited editions such as the successful Lindt Dubai Chocolade.

Lindt stock forecast for 2025

Looking ahead to 2025, Lindt & Sprüngli is initially confident about the coming year and the years ahead. Specifically, the Swiss company expects organic growth of 7 to 9 percent for the 2025 fiscal year. This would allow the company to continue the strong growth of the previous year. This expectation is based, among other things, on further necessary price adjustments due to persistently high raw material costs, particularly for cocoa.

Lindt & Sprüngli also expects further improvements in profitability. The operating profit margin is expected to increase by 20 to 40 basis points in 2025, after a margin of at least 16 percent has already been targeted for 2024. Lindt & Sprüngli is sticking to its medium-term targets for the period after 2025. The chocolate manufacturer continues to aim for organic sales growth of between 6 and 8 percent per year, accompanied by a continuous improvement in the operating profit margin in line with the current year.

Source: Sales and Margin forecast

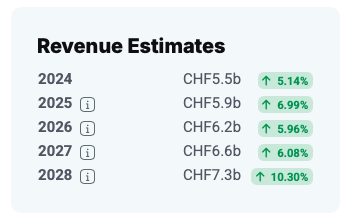

Analysts are similarly optimistic. Sales forecasts for the coming years show continued growth momentum. Sales of around 5.9 billion Swiss francs are expected for 2025, representing organic growth of 7.4 percent compared to the previous year.

Source: Revenue Estimates by analysts

This would allow Lindt to continue the positive trend from 2024, when sales of 5.5 billion Swiss francs were already achieved. Growth is expected to remain at a solid level in the following years. Sales of 6.2 billion Swiss francs are forecast for 2026, corresponding to an increase of 6.2 percent. In 2027, sales are expected to rise to 6.6 billion Swiss francs, representing an increase of 6.2 percent. The forecast for 2028 is particularly strong: with expected sales of 7.3 billion Swiss francs, growth of 9.6 percent is predicted, which would represent the highest increase within the five-year period.

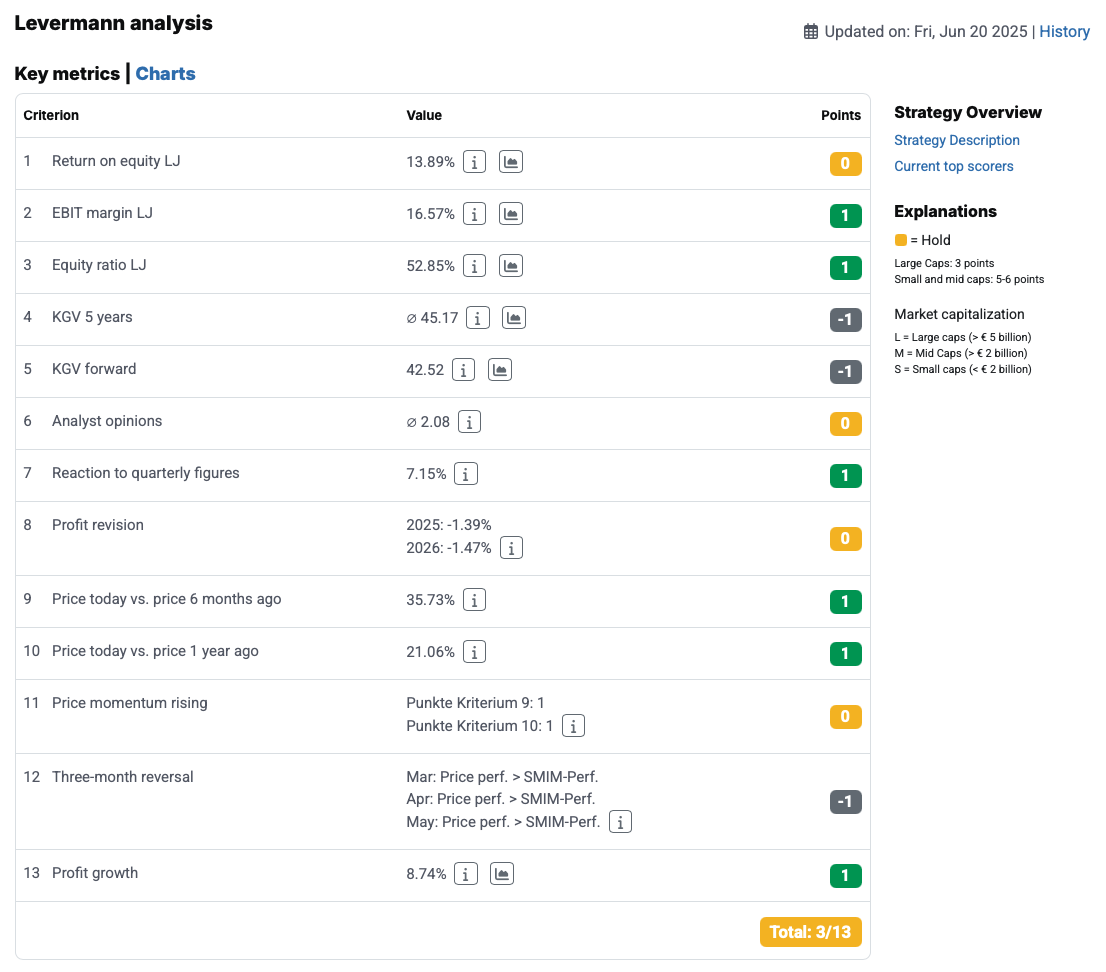

Key figures for Lindt tock from the Levermann analysis

The Levermann analysis, which offers a systematic approach to stock valuation, paints a mixed picture for Lindt & Sprüngli stock. The score of three points does not yet indicate a clear trend toward buying, which may be due primarily to the high valuation. Nevertheless, there are a number of factors that speak in favor of the stock.

Source: Levermann analysis

The EBIT margin is certainly a positive factor: at 16.6 percent, Lindt & Sprüngli achieved a very solid figure, which earned it one point in the analysis. The equity ratio of 52.9 percent is also very solid and received a positive rating. Lindt stock earned further points for their reaction to the quarterly figures. On the day of publication, the excess return was positive at 8.3 percent. Two further points were also scored for stock price performance. The stock price rose significantly over both six months (36 percent) and twelve months (21 percent).

However, due to weak price momentum, the chocolate manufacturer's stock did not receive any points in the Levermann analysis, partly because the short-term moving averages have not yet been significantly broken.

The three-month reversal even results in a minus point, as the relative strength compared to the SMIM (Swiss Market Index Mid) is considered too strong – a classic counterpoint in the Levermann model. The forward P/E ratio of 43 is also unconvincing, indicating a high current valuation in relation to expected earnings – this results in a minus point.

The same applies to the 5-year P/E ratio of 45, which takes into account the earnings of the last three years and those of the next two years and calculates an average value. Analyst opinions also fail to earn any points, as they tend to be neutral. Finally, the picture looks better for earnings growth, which is solid at 8.7 percent and earns one point.

Evaluation of Lindt stock

As we have already seen, many things look good at Lindt. That is at least a good basis for a solid investment. However, as is so often the case, when you evaluate the company, you realize that the price is too high. Unfortunately, this is also true for Lindt.

Source: Key metrics

The expected P/E ratio is extremely high at over 40, and the enterprise value to free cash flow multiple is still expensive at 37. Even for a quality stock with a deep moat, that's not chicken feed. And there's little to be gained in terms of dividends either. The dividend yield is just over one percent. Even the extremely solid dividend history and the annual dividend in kind (a box containing four to five kilograms of Lindt chocolate) are of little help here. The same applies to the solid sales growth. Nevertheless, long-term investors have historically been rewarded for their patience. Over the past ten years, the stock price has risen by 123 percent. Looking back over 20 years, the stock price has almost septupled.

The competitive situation is therefore likely to be decisive for further development, as is the strength of the brand. Will Swiss chocolate from Lindt continue to be a global phenomenon? Can the markets in Asia and Latin America be successfully tapped? These are precisely the questions investors must ask themselves. In the medium term, at least, there are many indications that the trends will continue, which bodes well for the stock.

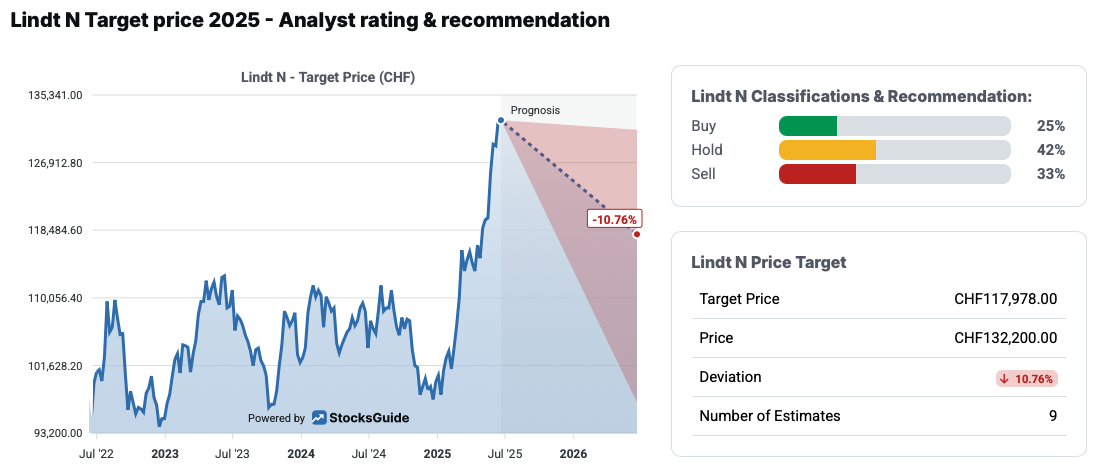

Conclusion on Lindt stock

Lindt & Sprüngli is a solid, fast-growing company with a strong brand, global presence, and clear strategic focus. Despite challenging conditions, such as high raw material prices and subdued consumer sentiment, the chocolate empire is demonstrating impressive resilience and consistently pursuing its growth course. Continuous market share gains, successful expansion in direct sales and promising sales forecasts underscore the long-term potential of the stock. However, the valuation is extremely high.

Source: Lindt target price

The mood among analysts is also subdued. They paint a mixed picture regarding the potential of Lindt & Sprüngli stock. Twelve analysts have issued price targets for 2026, with the average price target at almost 118,000 Swiss francs. This figure is around 10 percent below the current stock price. Even the highest target price of 131,000 Swiss francs is still slightly below this. There is also no consensus among analysts: only three recommend buying the stock, while five advise a neutral stance and four recommend selling.

The author and/or persons or companies associated with the StocksGuide own or may own stocks in Lindt.

This post represents an expression of opinion and not investment advice. Please note the legal information.