The global cybersecurity market is poised for a decade of growth. Cyberattacks are increasing exponentially in both frequency and complexity, AI-powered threats are emerging in real time, and companies worldwide are realizing that traditional network perimeter security is no longer sufficient in a cloud-first world. This is precisely the vacuum that Zscaler (ISIN: US98980G1022) is filling. Since its founding in 2007, the company has played a key role in shaping the concept of “Zero Trust” and has made it the foundation of its entire platform strategy. The Zero Trust Exchange model assumes that no user, device, or application is inherently trustworthy—every data stream is individually verified. The equity story can be boiled down to a clear core: The company aims to replace enterprises’ outdated firewall and VPN infrastructures with a fully cloud-based security architecture. Two megatrends will support growth for years to come: the increasing use of artificial intelligence in corporate environments, which creates new attack vectors while simultaneously requiring new security solutions; and the growing regulatory requirements for data sovereignty and cloud compliance, particularly in Europe. The stock itself has been on a rollercoaster ride over the past twelve months. From a high of over $330 in the fall of 2025, the price fell to below $147 by the end of February 2026—a decline of more than 55 percent. Viewed over the entire year, however, the stock is down only 25 percent.

Source: Stock price

The high volatility was driven by a disappointing forecast for the first quarter of fiscal year 2026, as well as general market turbulence in the software sector triggered by interest rate concerns and the so-called “SaaSpocalypse”—that is, fears of structural margin erosion among SaaS companies due to AI competitors. Following strong quarterly results in late February 2026, the stock price eventually rebounded by more than ten percent. In our Zscaler stock analysis today, we examine whether current prices present a buying opportunity and whether a turnaround in the stock is possible.

Company Profile – Pioneer and Market Leader in Zero-Trust Architecture

Zscaler was founded in 2007 in San José, California, and went public on the Nasdaq stock exchange in 2018. The company operates a cloud-native, multi-tenant Security-as-a-Service platform known as the “Zero Trust Exchange.” At its core, Zscaler provides security functions that were traditionally delivered by hardware appliances and on-premises software—but entirely as a cloud service. This eliminates the need to route data packets through a corporate network.

Zscaler is also a classic disruptor with its business model. The market potential is enormous. Zscaler itself estimates it at up to $100 billion. Given the current annual revenue of around $2.7 billion, there is still a lot of room for growth. Revenue growth of over 20 percent also shows that the market is far from saturated. However, competition is intensifying, as evidenced by the steadily declining revenue growth rates. Recently, however, there has been some relief in this area, as the following chapters will demonstrate. But now to the definition of the business model.

The Core Business: Subscription-Based Security Platform

Zscaler’s business model is based almost exclusively on subscriptions (SaaS). Customers therefore pay annual license fees for access to the platform. Pricing is typically per user or per device. In recent quarters, however, Zscaler has begun to expand the model to include usage-based components. These already account for more than 25 percent of the value of new annual contracts. This step enables the company to scale with growing data volumes without alienating customers. This could be particularly exciting for the future, because in a world where more and more AI agents are taking over the work, there would be increasing pressure on revenue growth.

Main Products and Segments

Zscaler’s platform comprises three main strategic solutions:

- Zscaler Internet Access

- Zscaler Private Access

- Zscaler Digital Experience

Source: StocksGuide AI

Zscaler Internet Access

Zscaler Internet Access (ZIA) is the flagship product that replaces traditional secure web gateways, cloud access security brokers, and data loss prevention solutions. ZIA protects users when accessing the public internet and SaaS applications. It remains the biggest revenue driver.

Zscaler Private Access

Zscaler Private Access (ZPA), on the other hand, is an alternative to traditional VPN solutions. It enables users to securely access internal corporate applications without exposing them directly to the internet. Government agencies and large corporations in particular rely on ZPA: 14 U.S. federal agencies at the cabinet level already use Zscaler products.

Zscaler Digital Experience

Zscaler Digital Experience (ZDX) is the newest major segment and measures and optimizes the user experience when using applications. It is aimed at IT administrators who want to track performance issues end-to-end.

In addition, there are newer solutions in the field of AI security: With the “AI Security Suite,” launched in January 2026 and including “AI Asset Discovery,” “Shadow AI Detection,” and “AI Protect,” Zscaler is responding to the growing demand for control over AI applications in the enterprise environment. These solutions could help maintain a high net retention rate in the future as well.

Revenue by Region – Americas Dominate

Looking at the revenue breakdown by region, approximately 51 percent of revenue in fiscal year 2025 came from the Americas, 30 percent from the Europe, Middle East, and Africa (EMEA) region, and 16 percent from the Asia-Pacific region. EMEA is a strategic focus, particularly in light of the new data sovereignty features that Zscaler expanded in March 2026 to meet European regulatory requirements. The market still offers considerable potential, but it also has its unique characteristics. The geographic expansion primarily demonstrates the ambition to grow into a global corporation. The foundations are in place; now they just need to be expanded. However, this is not always easy, as the market has some key peculiarities.

Zscaler’s Cybersecurity Market

Within this broad market, the company operates primarily in the field of cloud-based security. This segment has grown significantly in recent years as more and more companies have migrated their applications and data to the cloud. Unlike traditional security providers, which rely on local hardware such as firewalls, Zscaler takes a fully cloud-native approach. This means that security functions are no longer installed within the corporate network itself but are provided via a globally distributed cloud infrastructure. This allows users to securely access applications and data regardless of their location. A key market segment in which Zscaler operates is the so-called zero-trust model. This security concept is based on the assumption that no user or device is automatically trusted—even if it is located within the corporate network. Instead, every access attempt is continuously verified. Zscaler is among the pioneers in this field and is also one of the leading providers delivering this architecture on a large scale as a cloud service. Furthermore, Zscaler is a key player in the Secure Access Service Edge (SASE) sector. This is a relatively new market that combines network security and network functions into a unified cloud platform. The goal is to provide companies with a flexible, scalable, and centrally manageable security solution that meets the requirements of modern, cloud-based IT environments.

Opportunities and Risks of Zscaler Stock

In these markets, Zscaler faces both opportunities and significant risks that are closely linked to technological developments and the competitive landscape.

Source: StocksGuide AI

The ongoing shift of IT infrastructure to the cloud represents one of the greatest opportunities. More and more companies are replacing traditional, on-premises systems with cloud-based applications. This automatically increases the demand for new security solutions. Since Zscaler has relied on a cloud-native model from the very beginning, it is well-positioned to benefit from this structural shift. The trend toward remote and hybrid work further reinforces this development, as secure access from anywhere is required. Another key growth driver is the rising awareness of cyber risks. Attacks are becoming more frequent and complex, forcing companies to modernize their security strategies. AI is accelerating this development even further. In this context, the zero-trust model is gaining increasing importance. New market segments such as SASE also offer additional growth potential, as many companies are currently fundamentally rebuilding their network and security architecture. Artificial intelligence itself can also be counted among the opportunities. AI presents a dual opportunity for Zscaler: On the one hand, threats from AI-powered attacks are rising, which increases the need for advanced defense solutions. On the other hand, Zscaler can use AI itself to improve detection rates and monetize new products like AI Protect. AI can also increase the efficiency of the business model—achieving more with fewer staff.

At the same time, however, there are also risks. One lies in the technological dynamics of the market. Security requirements and attack methods are constantly evolving, so Zscaler must continuously invest in innovation. Should the company fail to keep pace with new technologies or quickly patch security vulnerabilities, this could lead to a loss of customer trust or trigger legal risks. Furthermore, the business model relies heavily on recurring cloud revenue. While this enables stable income, it also comes with high expectations for continuous growth. A slowdown in demand or reduced customer budgets due to economic uncertainties could quickly have a negative impact on business performance. Another risk lies in competition. Competition in the cybersecurity market is intense due to low barriers to entry and includes both established IT conglomerates and specialized providers. On the positive side, Zscaler has specialized in growth areas of the IT security market. However, developments here are also dynamic. Large companies today have significant resources and existing customer relationships. This allows them to aggressively expand their own cloud-based security solutions. AI-driven coding, in particular, is making it increasingly affordable to produce software products. Ultimately, this could lead to increased price pressure or slow down Zscaler’s growth.

Competition

Zscaler competes with traditional network security providers as well as with new, cloud-native specialists. Furthermore, the lines between network and security solutions are increasingly blurring, which further intensifies competitive pressure.

Source: StocksGuide AI

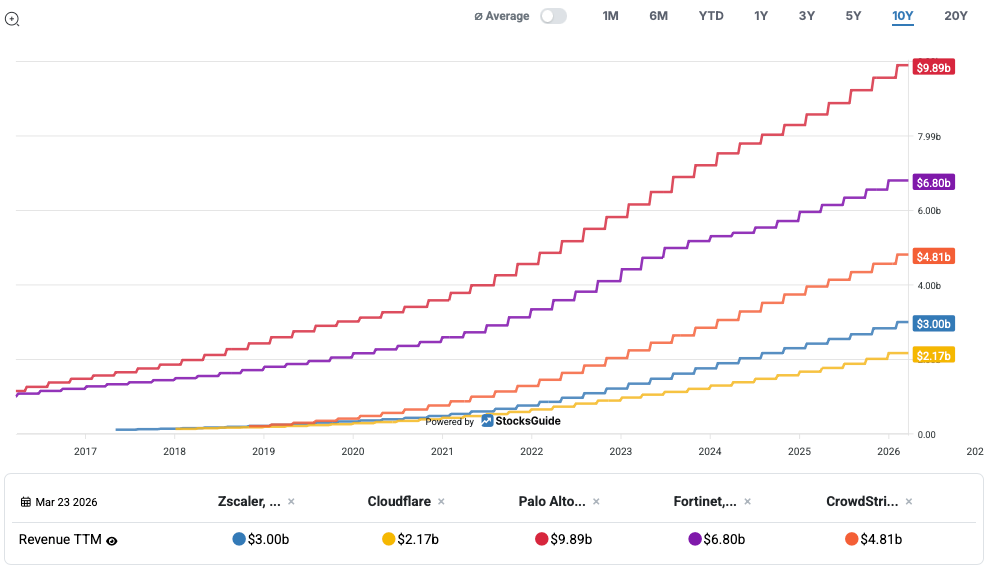

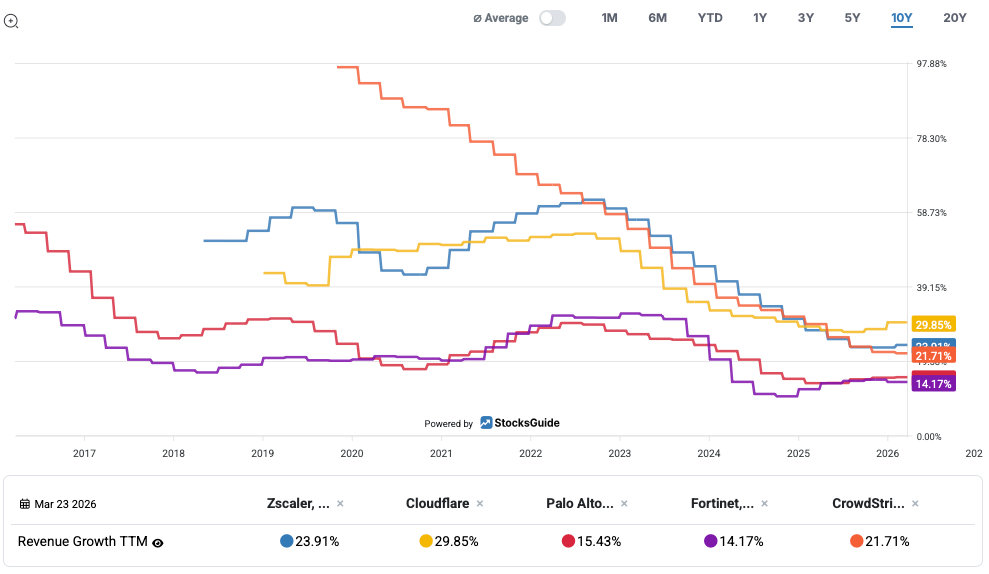

Key competitors include large, established technology companies such as Palo Alto Networks, Cisco, and Fortinet. These companies have built a strong historical presence in the field of network security and are investing heavily in expanding their cloud and SASE offerings. Their main advantages lie in their size, their global customer base, and their ability to offer integrated, end-to-end solutions. In addition, there are specialized cloud security providers such as Cloudflare and Netskope, which have relied on cloud-native architectures from the very beginning. These competitors are also highly innovative and focus on specific areas such as web security, data control, or zero-trust access. A look at the major players shows just how well the market is performing. They are all experiencing strong growth. Zscaler is one of the smaller players in the market.

Source: StocksGuide Charts

However, their growth is steadily slowing, which could indicate market saturation. Nevertheless, the growth remains impressive. All of them are consistently reporting double-digit revenue growth rates.

Source: Revenue Growth

Major cloud platforms such as Microsoft and Amazon are also a competitive factor. These providers are increasingly integrating security features directly into their cloud ecosystems. This allows them to cover parts of the value chain themselves, putting pressure on external specialist providers like Zscaler—especially when customers heavily align their IT with a single platform.

Despite this intense competition, Zscaler has several differentiating factors. These include, above all, its consistently cloud-native architecture and early focus on the zero-trust model. Nevertheless, the market remains highly competitive. In the long term, it will be crucial whether Zscaler can maintain its technological leadership while keeping pace with the scaling and integrated offerings of major competitors. Looking at its moats, things might not look so bad after all.

Moat and Competitive Advantages

Although Zscaler faces competition, it possesses several structural competitive advantages. Its moat—that is, its sustainable competitive advantages—stems primarily from its architecture, its business model, and its market positioning. A key difference lies in the technical foundation. While many competitors, such as Cisco or Palo Alto Networks, come from the world of hardware firewalls and have subsequently expanded their solutions into the cloud, Zscaler was developed from the outset as a fully cloud-native platform. This means that all customer traffic is routed through and inspected on Zscaler’s global cloud infrastructure, rather than via local devices on the corporate network. Due to its long-term development and globally distributed infrastructure, this architecture is difficult to replicate. Another part of the moat is the network effect driven by data. Since Zscaler analyzes enormous amounts of traffic daily, it can detect threats faster and continuously improve its protection mechanisms. The more customers use the platform, the better it becomes—an effect that makes it difficult for new competitors to enter the market. Added to this is the structural advantage provided by the zero-trust model. Here, Zscaler replaces traditional network architectures rather than merely supplementing them. Many competitors, on the other hand, attempt to adapt existing systems incrementally, which often leads to more complex and less efficient solutions. The business model itself also contributes to the moat. Zscaler sells its solutions as subscription-based cloud services that are deeply integrated into customers’ IT infrastructure. Switching to another provider therefore involves significant effort, leading to high switching costs and strengthening customer loyalty.

Zscaler’s Latest Quarterly Results from January 2026

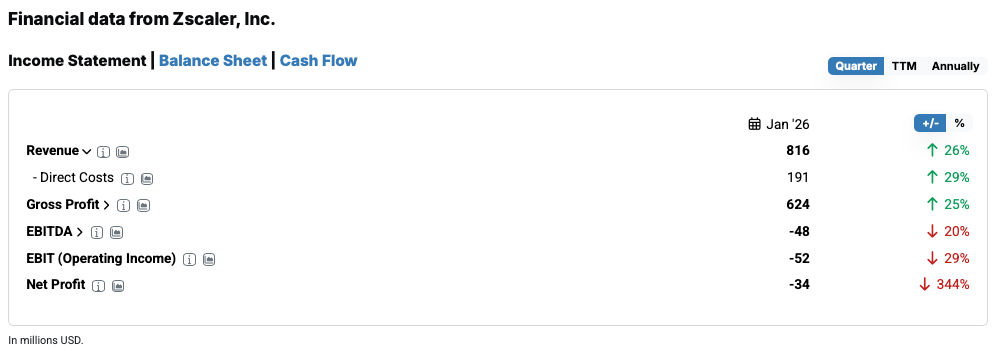

On February 26, 2026, Zscaler reported its results for the second quarter of fiscal year 2026—which ended on January 31, 2026—and significantly exceeded market expectations in nearly every category.

Source: Financial data

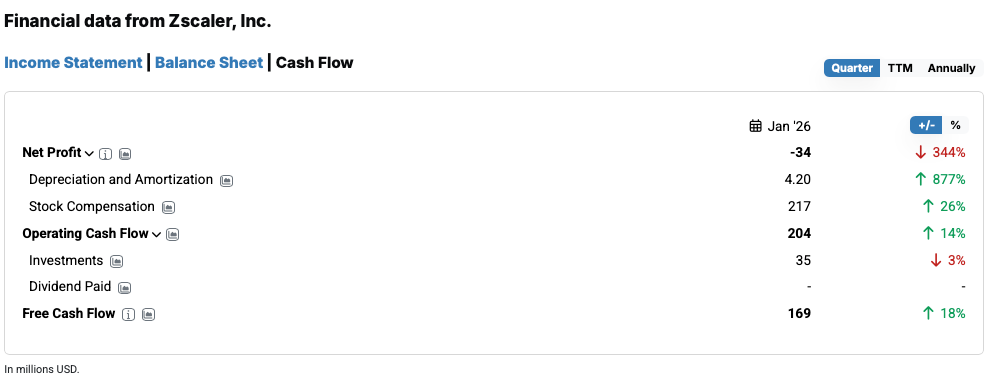

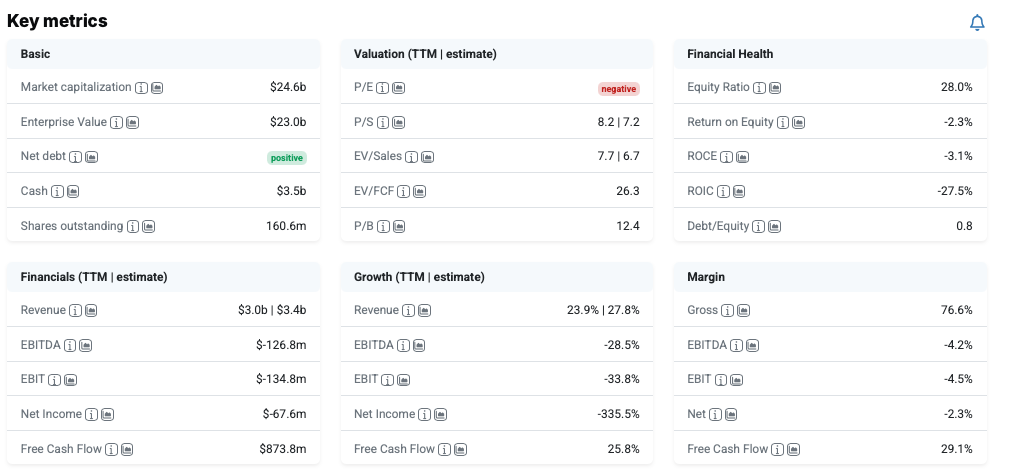

Revenue increased by 26 percent to $816 million. However, EBITDA fell sharply by 20 percent to $-48 million. This was due to increased research expenses and higher marketing costs. The focus therefore remains on organic growth, although acquisitions are now also being made. With a net loss of $34 million, the company remains on the threshold of sustainable profitability. However, based on free cash flow, this threshold has already been reached for some time. In the second quarter of 2026, free cash flow stood at $169 million, representing an increase of 18 percent. The main reason for the discrepancy with net income remains the high level of stock-based compensation.

Source: Financial data

It is clear, then, that Zscaler continues to benefit significantly from the key megatrends in the cybersecurity market, particularly in the areas of cloud, zero trust, and, increasingly, artificial intelligence. It is also notable that this growth is not driven by individual products alone, but is broadly supported across multiple strategic pillars. Management places particular emphasis on the areas of AI Security, Zero Trust Everywhere, and Data Security. Zscaler is thus increasingly positioning itself as a platform rather than merely a provider of individual solutions. This is precisely a decisive factor in the competitive landscape, as customers are increasingly demanding integrated security solutions.

Another key aspect in the second quarter is the role of artificial intelligence as a growth driver. Here, Zscaler is seeking to position itself early on as a security platform for the “AI era.” The increasing use of AI in enterprises creates new attack surfaces while simultaneously increasing the complexity of IT security. The fact that Zscaler is making targeted investments in areas such as AI governance, protection of AI applications, and even security for autonomous agents further underscores that the company aims to actively shape the next major technological shift rather than merely react to it. Strategically, it is also clear that Zscaler remains committed to expansion. Acquisitions such as those of Red Canary and SquareX, as well as partnerships with major cloud ecosystems, ultimately demonstrate that the company is strategically acquiring capabilities and expanding its platform offerings. At the same time, the global infrastructure is being expanded—which is essential to meet rising international demand and comply with regulatory requirements.

Zscaler Stock Forecast 2026

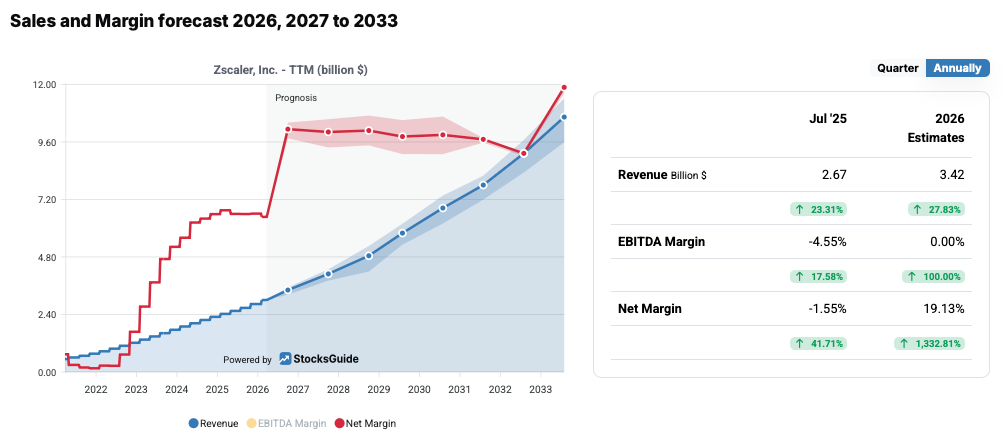

Zscaler’s forecast paints a very solid and confident picture for the coming quarters. For the third quarter, for example, strong growth is still expected, albeit with a slight normalization compared to the previously even higher rates. Revenue is expected to be around $834 million to $836 million, representing growth of approximately 23 percent. At the same time, profitability is shown to be increasing disproportionately. Non-GAAP operating income is expected to grow by around 28 to 29 percent, and adjusted earnings per share will also rise to about $1.

An even more interesting perspective is the outlook for the full year 2026, as the direction becomes clearer here. Expected annual revenue is around $3.3 billion, which still represents growth of approximately 24 percent. The key metric for SaaS companies, Annual Recurring Revenue (ARR), has also been revised upward and is expected to be around $3.7 billion. The trend in profitability is particularly strong. Adjusted operating income is expected to grow by about 28 to 29 percent for the full year 2026, and adjusted earnings per share are now expected to be just under $4 per share.

Source: Sales and Margin forecast

Analysts share a similar view of these developments. They unanimously expect significant double-digit growth that will only slow down gradually. The net margin, on the other hand, is expected to rise significantly and reach over 30 percent in the 2030s.

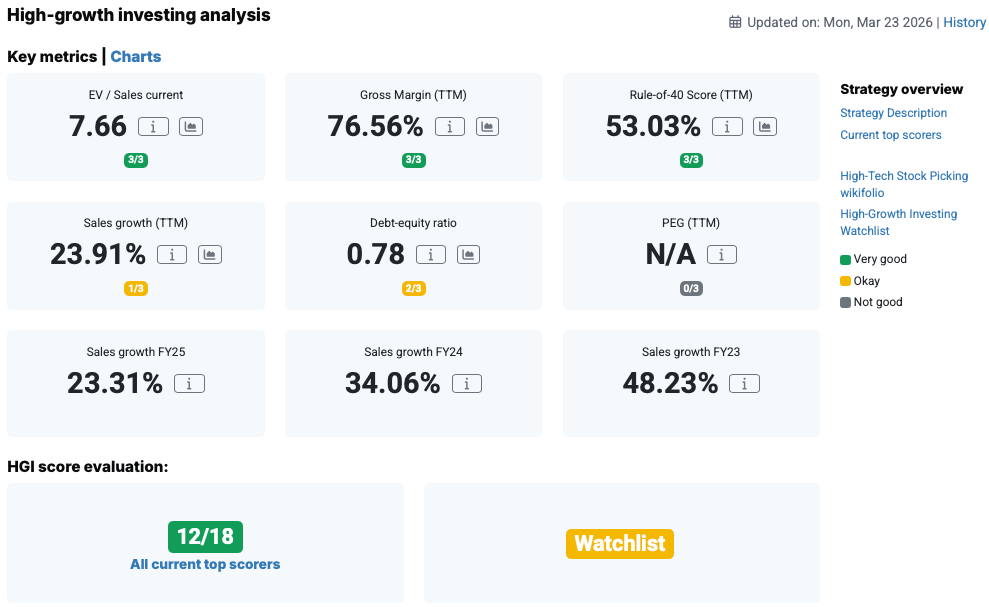

Key metrics for Zscaler stock from the HGI analysis

The High-Growth-Investing analysis paints an overall solid, if no longer entirely flawless, picture of Zscaler as a more mature growth company. Overall, it achieves an HGI score of 12 points. While this is good, it is not top-tier.

Source: HGI Analysis

The quality of the business model is particularly noteworthy. With a gross margin of around 77 percent, Zscaler ranks among the most efficient SaaS companies. The Rule of 40 score of over 50 percent is also very good and signals a healthy balance between growth and free cash flow profitability. This is an important indicator that the company is not only growing but also does not necessarily face increased financing needs in the long term. Shareholders are nevertheless facing dilution, which is also due to the high level of equity-based compensation.

The valuation is also solid in the current market environment. An EV/sales ratio of about 7.6 is not excessive for a growing cybersecurity company, especially when considering the trend in profitability. Unfortunately, the PEG ratio, which compares the valuation to growth, cannot be calculated due to losses and declining earnings metrics. However, based on adjusted figures, an additional point could ideally be gained here as well.

On the other hand, a clear weakness is also apparent: the slowing pace of growth. While Zscaler achieved growth rates of over 40 percent a few years ago, current growth stands at only around 24 percent. In the HGI classification system, this leads to a lower rating in this category. The company is thus in a transition phase from hyper-strong growth to a more mature growth phase, which is likely to impact its valuation.

Zscaler Stock Valuation

The valuation of Zscaler is arguably the most contentious issue surrounding the stock. While the picture has improved after the price decline of over 55 percent since its multi-year high in 2025, the valuation remains challenging.

Source: Key metrics

The forward P/E ratio remains negative. On a non-GAAP basis, it stands at approximately 39, calculated based on the expected adjusted EPS for 2026 of around four US dollars. The valuation is better explained by the revenue multiple. The expected price-to-sales ratio (PSR) is around 7.2, and the EV/Sales ratio is slightly below 7. However, based on free cash flow, investors only have to pay a multiple of around 26. To put this in perspective: During boom times, Zscaler traded at an EV/Sales multiple of 30 to 40 and a free cash flow multiple of over 300 – the current valuation is therefore historically cheap.

Source: StocksGuide Charts

This development can also be explained by a steady decline in growth rates. While the company recorded revenue growth of over 60 percent five years ago, it now stands at just over 20 percent. This slowdown generally justifies a lower valuation than in the past. However, the dynamics and direction of growth are also crucial. And it is precisely here that a stabilization of the growth rate at a high level has become apparent in recent quarters, which is a positive sign. The high quality of the business model must also be considered in the valuation. The gross margin of over 76 percent demonstrates that Zscaler has a highly scalable SaaS model. Even more important, however, is the fact that the company is already generating strong cash flows. This sets Zscaler apart from many other growth companies that are not yet profitable at the cash flow level. Investors are therefore more willing to accept a moderate valuation premium, provided the growth and outlook are promising. Another key factor is the market position. Zscaler operates in structurally growing areas such as Zero Trust and cloud security, and is considered a technological leader in these fields. This position also justifies a premium. At the same time, however, several factors limit its upside potential. In addition to slowing growth, the intense competition from large providers like Microsoft and Palo Alto Networks is a particular drawback. This competition increases uncertainty about how strong and for how long Zscaler can maintain its growth rates.

Conclusion on Zscaler Stock

Zscaler is a structurally strong company that benefits from a clear megatrend: Zero Trust, AI security, and cloud migration. These trends will support demand for Zscaler's platform for the foreseeable future. The results for the second quarter of fiscal year 2026 also demonstrate the company's operational performance. Revenue growth of 26 percent, stable margins, strong free cash flow, and a record customer base were all reported. The revenue slowdown has thus been halted, at least for now. Looking ahead, growth is expected to slow only slightly. However, risks remain. GAAP losses, the ambitious forward multiple, and intense competition from Palo Alto Networks and CrowdStrike are significant factors. Furthermore, it remains to be seen whether AI will become a key growth driver or a major threat.

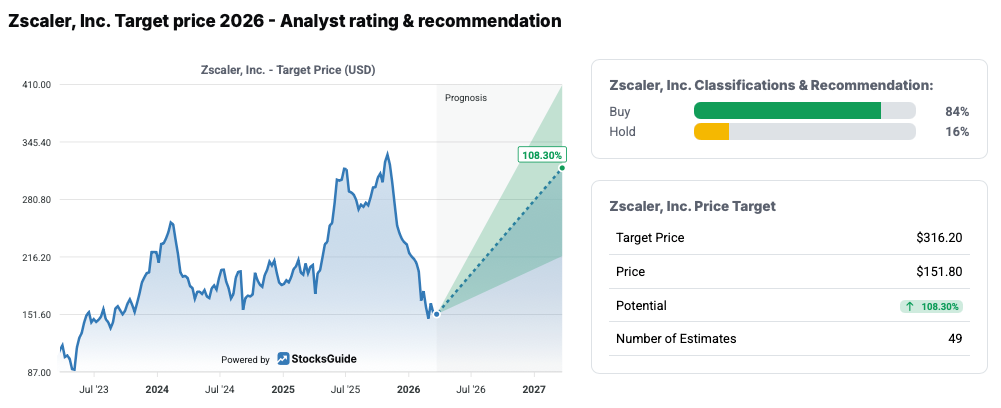

Source: Target price

The consensus among analysts is "Buy," with a median price target of $316.20 – a figure significantly above the current level. A return to the previous highs could therefore be possible if the growth rate accelerates again and the outlook improves accordingly. Otherwise, the share price could remain weak, especially since high expectations are still priced in. Those looking for a larger discount or risk buffer on Zscaler stock can set an alert on aktien.guide to revisit the stock. I find an alert level near the previous lows from 2023, around $90, particularly interesting.

The author and/or persons or companies associated with StocksGuide own or may own shares of Zscaler. This article represents an expression of opinion and does not constitute investment advice. Please note the legal information.