Table of Contents

Traditional asset classes such as government bonds or equities are repeatedly causing headaches for investors due to interest rate risks, volatile markets and an uncertain economic situation. The search is on for alternatives that promise high returns at acceptable risk. The idea of diversification with uncorrelated assets such as Bitcoin, gold or unlisted investments is also coming more into focus. These can be used to reduce portfolio risks while maintaining the same return expectations.

The market for private equity and infrastructure investments has established itself as a potential game changer in this regard – and it is booming. This is also because it benefits from long-term trends such as digitalisation, dilapidated and green infrastructure, and succession planning in medium-sized companies. The 3i Group (ISIN: GB00B1YW4409), with a history spanning over 75 years, is a potential winner of these developments.

With a diversified portfolio of high-growth private equity investments and stable infrastructure investments, the company combines the prospect of high returns with a certain resilience to market fluctuations. Business is booming, as the figures of the investment company show. In recent years, sales have grown at an average double-digit rate, with EBITDA growing even faster. The share price has also reflected these developments, with an impressive increase of over 1,000 per cent in the last decade.

Source: Performance of the 3i Group stock

But despite the strong price increase, 3i Group shares are not necessarily expensive. For example, the P/E ratio is only in the single digits. Furthermore, the company regularly pays attractive dividends that are on the rise. These developments are also due to the good performance of one of 3i Group's core investments, Action. The Dutch discounter is on a strong expansion course and is increasingly taking market share from the established industry leaders Lidl and Aldi. This is likely to continue in the medium term. But what are the key aspects of 3i Group's shares?

The following 3i Group stock analysis takes a closer look at the success of the investment company, how it is positioned financially, which valuation ratios speak for or against the share and what role the specific business model as an investment company plays in this. Is it a buy?

Company profile – British investment company

3i Group is an international investment company based in London that operates in the areas of private equity, infrastructure and selected strategic investments (Scadlines).

Source: 3i Group Investor Relations

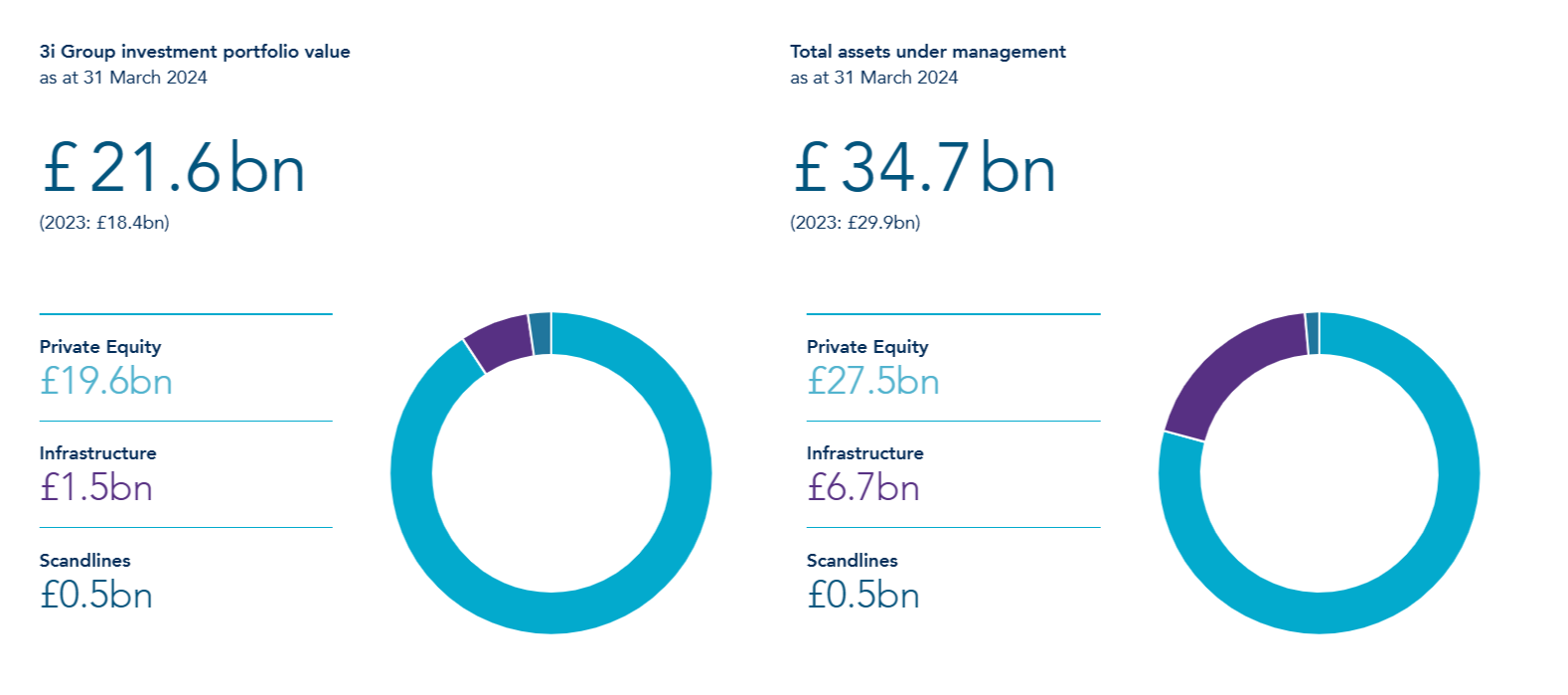

In the private equity sector, the 3i Group focuses on investments in medium-sized companies with high growth potential, particularly in Europe and North America. The private equity company primarily acquires majority stakes in established companies in sectors such as consumer goods, business services, healthcare and technology. By providing capital, strategic expertise and global networks, the 3i Group helps to increase the value of each of these portfolio companies. The company generates profits mainly through the appreciation of its shareholdings and their subsequent sale, as well as through ongoing dividends and management fees.

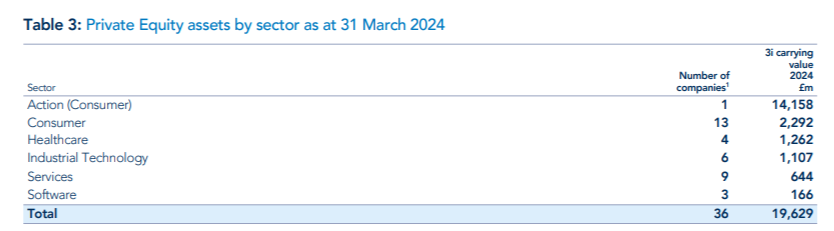

The discount retailer Action plays a special role in the private equity portfolio. At 72 per cent, it accounts for the majority of the segment's assets of 19.6 billion British pounds at the end of the 2024 financial year (quarter ending 31 March). The 3i Group recently held a simple majority of 57.9 per cent in the Dutch retailer. Action's growth is impressive in several respects: since 2005, the Dutch company's revenue has increased by 24 per cent annually, and its operating EBITDA by as much as 28 per cent. At around 10 per cent, like-for-like sales are twice as high as those of its competitors. The same applies to growth. So they are doing a lot better than the competition. With over 2,500 stores in Europe, the company is now the market leader in non-food retail. By 2026, 1,300 new stores are to be added – a store growth of over 50 per cent in just two years.

Source: 3i Group Annual Report 2024

Another important investment is Royal Sanders, a manufacturer of private label products and contract manufacturer in the personal care sector. The company benefits from a buy-and-build strategy that has been further strengthened by targeted acquisitions such as the integration of Lenhart. The portfolio also includes the European Bakery Group, which was formed from the merger of Dutch Bakery and Coolback, a German manufacturer of frozen bakery products. This platform is also being expanded, including through the acquisition of the British manufacturer Panelto. Other investments include ten23 health, a service provider in the field of biologics, and Luqom, an online lighting specialist. Smaller investments such as YDEON, an online retailer of garden houses and saunas, and Digital Barriers, a provider of video technology solutions, are also part of the portfolio.

Source: 3i Group Annual Report 2024

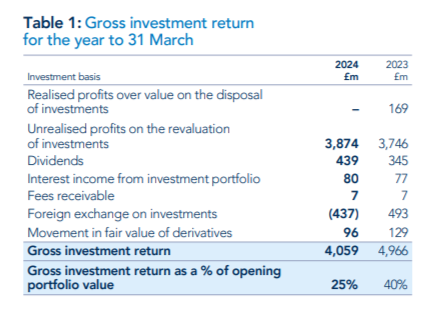

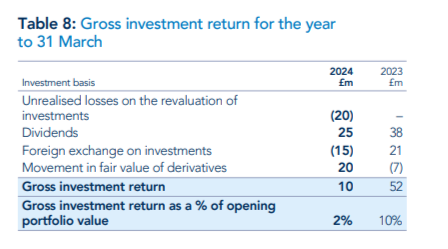

In total, a gross investment return of 4 billion British pounds or 25 per cent on the capital employed was achieved in the 2000 financial year. A large part of this return is due to unrealised gains on investments.

In the Infrastructure division, the 3i Group invests in critical infrastructure projects that offer stable and long-term returns. The main areas of investment include energy, transport, utilities and telecommunications – all critical areas of the economy. At the end of the 2024 financial year, the division had assets under management of £6.7 billion and generated a gross investment return of £99 million or 7 per cent.

Source: 3i Group Annual Report 2024

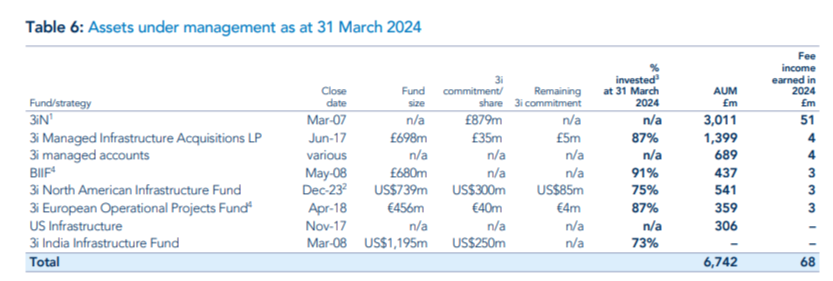

3i manages, among other things, the listed fund 3i Infrastructure plc (3iN), which invests in listed and private infrastructure projects. The aim of these investments is to generate a continuous and reliable return for investors while improving the quality and efficiency of the infrastructure projects. 3iN's major holdings include TCR, ESVAGT and Infinis.

TCR is a leading ground equipment rental company for airports and represents 16 per cent of the portfolio. The company is benefiting from the growth and recovery of the global aviation industry. ESVAGT, which makes up 14 per cent of the portfolio, specialises in offshore wind services, including safety and emergency response services for offshore installations. Infinis, which contributes 11 per cent, is a major producer of renewable energy that specialises in energy generation from landfill gas. The portfolio comprised a total of 12 assets at the end of the 2024 financial year.

At the end of the financial year, the 3i Group itself held 29 per cent of 3iN, worth 879 million British pounds. At 38 million British pounds, the investment also achieved the highest growth in value in the segment. Dividends of 31 million British pounds were received from this investment.

In addition, 3i has a stake in Scandlines, one of the leading ferry companies in the Baltic Sea. It is considered a long-term strategic investment and provides stable cash flows by operating ferry services between Germany and Denmark. Scandlines is an example of 3i's strategy of investing in high-quality, established companies that can achieve high returns through efficiency improvements and targeted innovation. However, the latest gross investment return of 2 per cent was not convincing. However, it can be explained by currency fluctuations.

Source: 3i Group Annual Report 2024

At the end of the 2024 financial year, the ferry business was valued at £519 million using a discounted cash flow model. This is a few million less than in the previous year (554 million British pounds), which is mainly due to currency effects. Nevertheless, a gross investment return of 10 million British pounds and an ongoing dividend payment of 25 million British pounds were achieved.

Competition

In the private equity and infrastructure sectors, the 3i Group has several major competitors that follow similar business models. These include Carlyle Group, Blackstone, KKR (Kohlberg Kravis Roberts) and TPG, all of which invest in private equity and alternative investments worldwide. These companies compete fiercely for investments in high-growth companies and also pursue long-term capital strategies to achieve high returns. In the infrastructure sector, 3i competes in particular with firms such as Brookfield Asset Management, Australia's Macquarie Group and IFM Investors, which make substantial investments in infrastructure projects, such as in the energy, transport and renewable energy sectors. In addition, there are specialised competitors such as Oakley Capital and Lexington Partners, which operate in the area of private equity funds and venture capital and have a strong presence in niche markets.

The competitive landscape is therefore characterised by a mix of global and regional players competing for investment opportunities and capital. Despite the competition, 3i's strong brand, diversified portfolio approach and successful track record with investments such as Action enable it to hold its own. The players mentioned above are just a small number of competitors. They differ in some respects in their investment approaches, but they have similar target markets, which makes them strong rivals of the 3i Group – especially because it is a volume market. Here, smaller companies can quickly rise to the top through networks.

Critical success factors

The references and network of a private equity company are therefore also crucial. A private equity firm's reputation has a significant influence on the willingness of target companies to be acquired, as a good reputation creates trust and attractiveness in bidding processes. Companies prefer investors who have a proven track record of value creation and maintain a fair partnership, which leads to better takeover opportunities. A negative reputation, on the other hand, deters potential target companies, increases transaction costs and makes it more difficult to access high-quality deals.

Influential individuals and networks play an equally crucial role in the private equity industry, as they facilitate access to exclusive deals, capital and strategic partnerships. Individuals with extensive experience and a good reputation, such as successful founders, experienced managers or well-known investors, can instil confidence in target companies and speed up the negotiation process. At the same time, strong networks in the industry, with consulting firms and other investors provide access to market information and enable co-investments or exit strategies that increase profitability or allow for rapid scaling. An established network and prominent personalities thus strengthen the position of a private equity firm in a highly competitive environment.

Market

The future of the private equity and infrastructure sector tends to look good. It is determined by various factors that bring both challenges and opportunities. At its core, the industry is benefiting from several long-term trends that will enable further growth. One important growth driver is the increasing focus on sustainable and climate-friendly investments. Infrastructure projects focusing on renewable energies, climate protection and decarbonisation are strongly encouraged by regulatory incentives such as the Inflation Reduction Act in the US and similar programmes such as the Green Deal in Europe. This creates new opportunities for investors, particularly in areas such as energy infrastructure and digitalisation. Technological change also plays a key role. Private equity firms are increasingly relying on artificial intelligence and automation to make investments more efficient and create added value for their portfolios. This includes optimising operations and accelerating growth in target companies. Despite these opportunities, the industry also faces challenges such as rising interest rates, geopolitical uncertainties and increasing regulatory pressure. Long-term prejudices such as those against private equity firms must also be combated. These could have a short-term impact on the availability of financing and transaction activity.

The last 3i Group quarterly figures as of September 2024

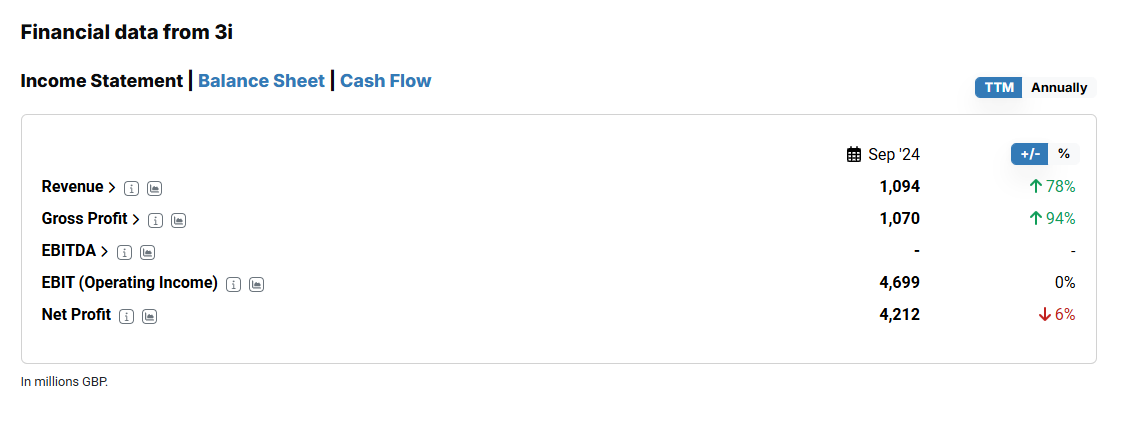

The last quarterly figures as of 30 September 2024 relate to the half-yearly figures for 2025, with a financial year ending on 31 March 2025. And these were extremely encouraging. It was initially noted that portfolio assets increased by 13.3 per cent to 22.9 billion British pounds. At the same time, net debt fell from 1.2 billion to 805 million British pounds. Liquidity also rose from 955 million to almost 1.3 billion British pounds.

Over the last twelve months, revenues increased by 78% to just over one billion British pounds. Operating income remained at the previous year's level of 4.7 billion British pounds.

Source: Financial data from 3i Group, StocksGuide

Now to the individual segments: in the first half of 2024, the private equity segment continued to perform well, with a gross investment return of 2.1 billion pounds, up 11 percent on the previous year. 94 percent of investments increased their earnings in the last twelve months.

The non-food discounter Action also continued to perform well. It increased its EBITDA by 26 per cent to 1.3 billion euros in the current year. The like-for-like sales trend is also convincing, at an impressive 9.8 per cent in the current year. There are no signs of a slowdown in momentum. The Dutch are taking more and more market share from the established discounters Lidl and Aldi. And that is likely to remain the case in the medium term.

Last but not least, the infrastructure segment also showed at least solid development. At the end of the quarter, a return on investment of 43 million was reported, which corresponds to a gross return of 3 per cent. In particular, the rise in the share price of the listed 3i Infrastructure plc fund, in which the company has a significant stake, contributed significantly to this performance. The value of this fund rose by 4 per cent in the current year.

3i Group stock forecast 2024

The 3i Group did not provide a specific forecast for 2025. However, the management board sees good momentum for its own investments and exit opportunities. It is therefore quite possible that some high-quality investments will be sold and book gains realised over the next twelve months. But on the acquisition side, too, management sees numerous interesting opportunities to replenish the investment pipeline.

Source: 3i Group Sales and margin forecast through 2027

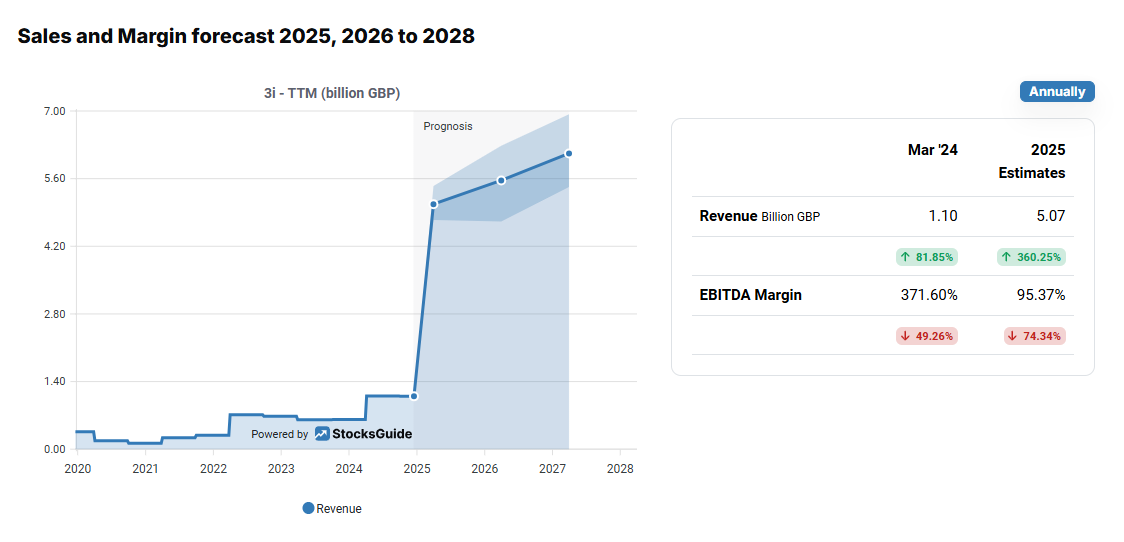

Looking at analyst opinions, they are optimistic about the future. For example, sales are expected to increase from 1.1 billion British pounds in 2024 to 6.1 billion pounds in 2027. The rapidly expanding discounter Action is not the only factor behind this. Based on the solid financial position of the 3i Group, analysts also expect increased acquisition activity.

Source: Earnings per share and P/E ratio developments for the 3i Group

The analysts also see further growth in earnings per share. For 2025, 5.06 British pounds per share are forecast – 27 percent more than in 2024. For 2027, the analysts consider earnings per share of almost six British pounds to be possible. This means that the P/E ratio should remain in single digits.

Important key metrics for 3i Group stock from the Levermann analysis

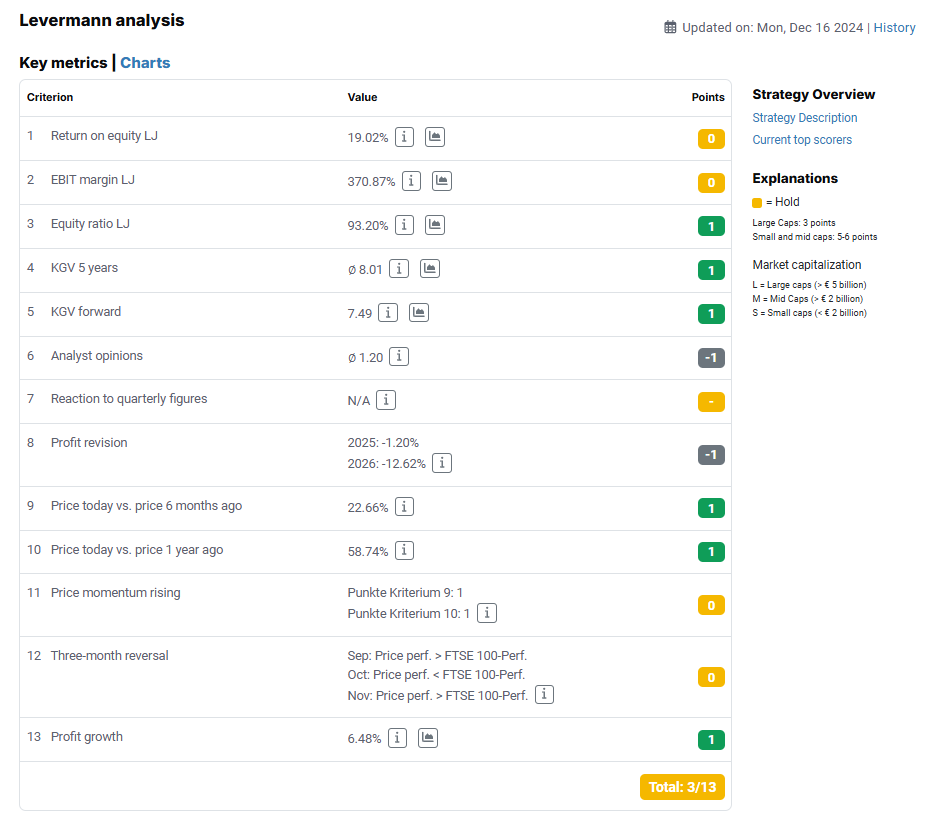

The Levermann analysis of 3i Group shows a solid trend with a total of 7 out of 13 possible points. According to the strategy criteria, the stock is a buy.

Source: Levermann score of 3i Group stock

The high equity ratio of 93 per cent is particularly positive and indicates financial stability. But the expected profit growth of 18.2 per cent also stands out from a fundamental perspective. Both categories were awarded one point each in the Levermann analysis.

On the valuation side, there were also two points. The 5-year P/E ratio, which takes into account the profits of the last three years and the expected two years, is only 7.8. Even on the basis of pure expectations (P/E ratio forward: 7.4), the 3i Group easily received full marks in the Levermann analysis.

From a technical perspective, the share price performance over the last six and twelve months was convincing, with a gain of 29 and 64 per cent respectively. The reaction to the quarterly figures on the day of publication was also clearly positive, with an outperformance of 3.5 per cent. The earnings revisions for 2025 support the optimistic outlook.

Despite these strengths, there are also neutral or negative criteria, such as the analysts' opinions with an average rating of 1.2 or the three-month reversal, which shows no clear trend. Overall, however, 3i Group is positioned as an attractive investment with a good valuation, solid financing and growth prospects.

Valuation of the 3i Group stock

At first glance, the valuation of the 3i Group appears very attractive with a clear single-digit P/E ratio. However, it is distorted by some peculiarities of the business model and the figures reported on the balance sheet. As an investment company, 3i invests in a variety of companies, primarily in the private equity and infrastructure sectors. 3i earns money from dividends, interest, fees and, above all, from increases in the value of the investments it holds. This means that a large proportion of profits are based on revaluations or revaluations of the investments held, which can lead to strong fluctuations in results. These accounting profits are not always liquid and depend on market developments and future divestment opportunities. A change in the discount rate or, as in the case of Scandlines, currency effects, can lead to significant changes in value. The expected price-earnings ratio of 7.4 should therefore be treated with caution, as it relates to unrealised operating accounting profits.

Source: Valuation ratios of the 3i Group stock

This becomes particularly clear when looking at the free cash flow, which amounted to just 367 million British pounds in the last twelve months. At over 100, the enterprise value to free cash flow (EV/FCF) ratio is extremely high. For investors, this means that while the substance and performance of the investments may be attractive, short-term liquidity and profitability have to be traded.

The NAV, which indicates the value of the balance sheet assets per share and plays an important role on the financial market as net asset value, was 2.261 pence at the end of the second quarter (30 September 2020). However, the share is currently trading at 3.708 pence, almost 64 per cent above this value. Now it is important to consider why this is so. On the one hand, the portfolio could have increased in value, which is entirely realistic given the rapid expansion of the discounter Action. But 64% in a single quarter? It is possible that investors are trading a little future fantasy here.

However, the high equity ratio of 93 per cent underlines the stability of the business model and the low dependence on outside capital. The same applies to the low gearing of 4 percent in the last financial report. Gearing refers to the ratio of debt to equity in a company's capital structure and indicates the extent to which a company is financed by debt. The low level of debt at the 3i Group could indicate that there is still potential for expanding the private equity business.

Conclusion on the 3i Group stock

The 3i Group presents itself as an interesting investment in the area of alternative investments, particularly in the rapidly growing market for private equity and infrastructure. The British company benefits from long-term trends and is financially stable, as evidenced by the high equity ratio of 93 per cent and the low gearing of 4 per cent. The impressive share price performance and the favourable valuation according to classic criteria such as the price-earnings ratio also speak in favour of the share. Over the last ten years, the holding company's share price has increased tenfold. At the same time, the price-earnings ratio remains in the low single digits. However, this is somewhat misleading. A significant portion of the reported profits are attributable to revaluations or revaluations that cannot be immediately liquidated and depend on the respective market development. The very high EV/FCF ratio of over 100 speaks a different language here. The fact that the share price is already more than 60 per cent above the most recently reported NAV could also be an indicator of risk.

Nevertheless, investors appreciate the stock, as the momentum shows. The growth potential is large and, above all, sustainable – thanks to Action. In addition, the solid financial position could enable further deals, which means a higher volume. Finally, the 3i Group is active in a growth market. Direct investments have proven to be a solid addition to large portfolios. This is also likely to be the case in the future. For investors with a long-term horizon who want to benefit from the dynamics of the private equity market and are willing to accept certain fluctuations due to the dependence on valuation adjustments, the 3i Group could therefore be a strategic asset. Above all, however, the 3i Group is a bet on the development of the non-food discounter Action. This discounter accounts for the majority of the investment and is expanding rapidly. If the expansion gains momentum and if Lidl and Aldi lose further market share to the Dutch company, the 3i Group is likely to benefit greatly from this.

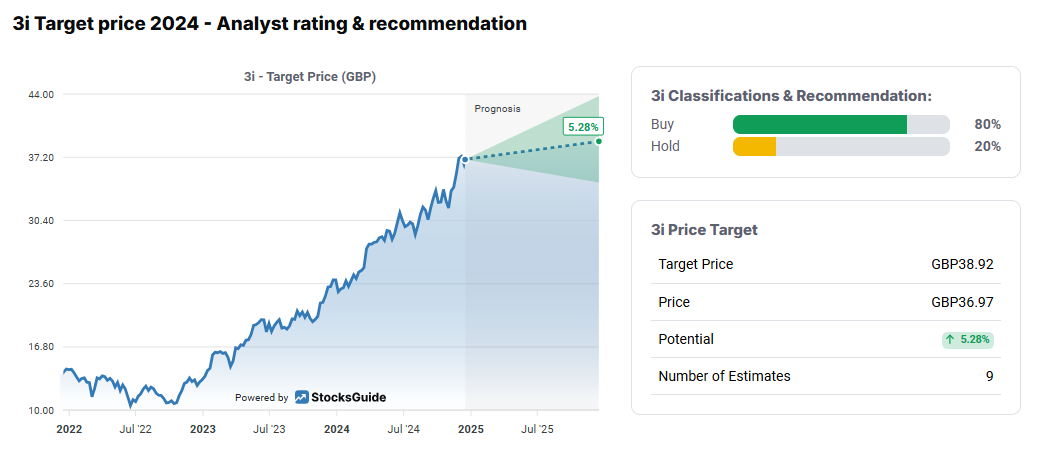

Source: Analysts' opinions on the 3i Group stock

Most analysts also agree that this could be the case, with the majority – 80 per cent, to be precise – recommending the share as a buy. The remaining analysts see the share as a hold. The average price target is 38.60 British pounds, 3.5 per cent above the last price.